Under the traditional business model, employees were often considered an expense. The cost of salaries, benefits, hiring, and firing received much more attention than the critical contributions that employees made to the company. Now, as companies better recognize the role that employees play in business success, things like employee output, knowledge, creativity, and problem solving are valued more highly and are seen as critical revenue-producing or profit-contributing assets.

This growing appreciation has led to increased focus on human capital management strategies in order to maintain, protect, and expand employee resources. There are three major steps you can take to align HR efforts more closely with the company’s financial systems: (1) realign company strategy to incorporate improved human capital development and management, (2) develop a dynamic recruitment program that aligns with company strategy, and (3) develop new measures of success and improved employee retention systems. The end result most likely will lead to increased profitability and greater business success.

STRATEGY REALIGNMENT

When forming a new company, discussions often focus on vision, profitability, and strategy. These conversations typically result in a clear definition of the problem the business is attempting to solve. In these early stages, it’s also common to draft plans to target potential customers. But goals for supply, demand, and sales are only part of a successful strategy.

A more comprehensive business plan also needs to include several considerations traditionally thought of as HR issues: hiring strategies, employee development and retention programs, and efforts to ensure the right people are placed on the right teams with strategic, aligned management. It’s also important to define what success looks like in both financial and human terms.

To improve human capital management systems, begin by incorporating the role of employees into the business strategy. For example, the finance team can help look at historical numbers to create written goals for the leaders of each department. A company should define the role of support staff for the sales team to illustrate precisely how their day-to-day work effectively supports the company’s goal of increasing sales.

Darren Root, CEO of Rootworks LLC, suggests starting by defining the ideal workday for employees and managers alike. For most business owners, the ideal day provides them with clarity on priorities, enabling them to focus their energy and thoughts on what they do best. This allows their activities to be tied more directly to the company’s strategic goals for the most part. And, remember, to retain employees, the workday should end at a reasonable hour.

CLIENT RELATIONSHIPS

The alignment of people with strategy also extends to the interactions between the business and external clients.

When developing effective advertising campaigns, marketing executives often begin by defining their audience. Apply this same type of exercise when developing or updating business plans. In this case, the goal is to determine the traits of an ideal client.

The personalities of clients are important. Good relationships often occur when companies align themselves with organizations that share similar visions, cultures, and values. Locating partners based on these traits can be as important as economic factors. If, as part of the sales process, leaders come across people they like, that same appreciation and respect will likely carry over in serving the client. If a company’s employees are considered a critical asset, it should be important to locate clients with a similar mind-set.

DYNAMIC RECRUITMENT

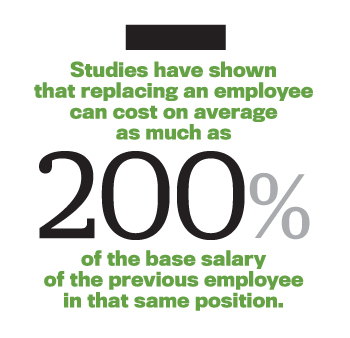

Developing a more people-focused business strategy makes it that much easier to recruit the right individuals to implement that strategy. And the importance of having the right people in place can’t be overstated. While people are a company’s greatest asset, job turnover is its biggest expense (see “Employee Turnover: Financial Impact and Human Impact”). Studies have shown that replacing an employee can cost on average as much as 200% of the base salary of the previous employee in that same position.

The costs are high because hiring and retaining talent involves several components. It begins with the costs associated with attracting the right candidates. Then there are costs associated with training and developing employees after they’re hired. Performance management is critical in all businesses, but assessment and improvement efforts also cost money. Employee engagement helps companies retain top talent, and it’s an expense that must be considered when replacing personnel. Finally, there are the costs associated with developing employees so they can advance and grow while remaining with the company.

Beyond financial losses, job turnover can be costly in other significant ways. It often leads to lower morale, which can reduce the overall quality of work and diminish innovation from all employees. Productivity losses are also a common result because most businesses, particularly smaller ones, rely on company-specific knowledge gained over an extended period of time. And customer satisfaction and retention also can be affected by employee turnover. All of these factors are particularly relevant to small businesses. Because most companies are based on relationships with people, the failure of many small businesses can often be traced back to employee turnover.Simply offering the most money isn’t enough to attract and retain top talent. A dynamic recruiting strategy considers several elements, including maintaining a positive work environment, identifying the driving motivations for employees and prospects, and defining the core values and personality traits needed for success within a position.

When Insperity collaborated to implement these strategies at GrowthForce, turnover was reduced and resulted in an average employee tenure of at least five years, which led directly to building strong recurring profits. While it’s unrealistic to assume all employees will stay with a company for a long period, an average employment of five to seven years is a sign that an employer has a sound recruitment strategy and great company culture.

CULTURE AND EMPLOYEE DEVELOPMENT

Before beginning the search for the right employees, a company should have a formal training program in place. Policies and procedures must be created, and coaching leaders should be identified and trained.

The goal for all companies should be to create a safe environment for people to work and thrive in. Seek to hire leaders who understand life’s challenges and who will work with employees and be flexible when needed, as long as the work is getting done.

A good work environment also features a culture that removes the fear of making mistakes. At the same time, of course, it’s also important to manage quality. One effective strategy for creating this balance is to have a position within the organization that interacts with staff on a daily basis to ensure quality and uniformity of work.

IDENTIFY EMPLOYEE MOTIVATIONS

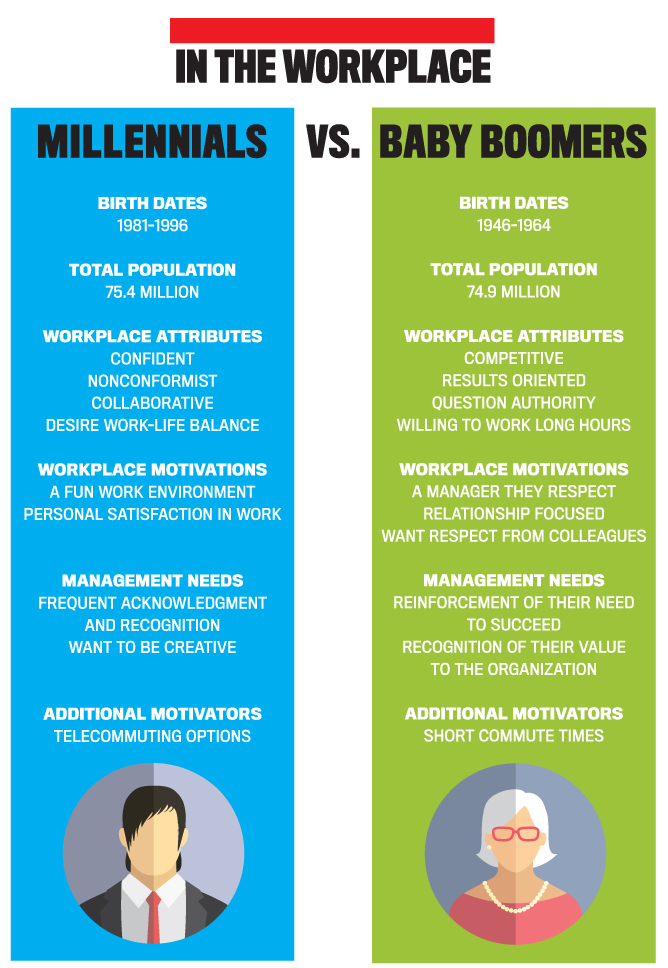

Once the training program is established and the right culture is in place, it’s time to begin the search for candidates. At least four generations of workers currently are in the workforce, including Millennials and Baby Boomers, so a company must find out what its prospective employees value. With such a wide range of workers, this can vary considerably. Are they pursuing a career or simply looking for a job? Do they want to have fun at work? Are they interested in having a company invest in their technology skills?

Baby Boomers often want to work for managers they respect. They are also often attracted to great benefits and prefer to work close to home. In comparison, Millennials are frequently in search of a workplace that offers flexible hours in a fun environment or the flexibility to work at home on occasion (see “In the Workplace: Millennials vs. Baby Boomers”).

While their motivations may vary widely, most people want to work for a company that cares about them. Going back to the importance of culture, employees don’t join a company to live in fear of an angry e-mail or phone call from a manager or a valued client. People join companies and quit bosses. With that in mind, a company’s goal should be to create a unique culture and meaning within the organization. The company must provide clear reasons that would make people want to work for it.

A good start is to define the motivations of prospective employees and list the financial and nonfinancial benefits of working for the company. This can be of great assistance down the road. For instance, it will be easier for interviewers to generate more meaningful interview questions that help identify the right candidate for the job. Interviews should begin by asking questions centered on the candidate’s values and mind-set before progressing into skill sets and experience. This will identify those candidates most likely to be in alignment with the client acquisition and retention strategy at the core of the company’s business plan.

DEFINE CORE VALUES AND PERSONALITY TRAITS

In addition to understanding the motivations of prospective employees, it’s often a good idea to proactively consider skills and personality traits when listing the criteria for ideal hires. This not only helps ensure that the right people are hired for the right job, but envisioning the ideal candidates also helps determine where to look to find the perfect match.

Candidates who enjoy solving problems often become top performers. In an accounting department, managers might look for people who are accountable, enjoy working as part of a team, and are passionate about gaining more knowledge. Knowledge-seeking workers gain considerable job satisfaction when their ideas or contributions to a strategy lead to direct revenue or profit improvement. And if the decision comes down to a candidate with a higher skill level vs. one who is a better cultural fit, it’s almost always better to hire the person who best fits the culture. Hire employees for attitude. Train them for skills. Skills and problem solving can be taught, but it’s difficult to change an individual’s attitude.

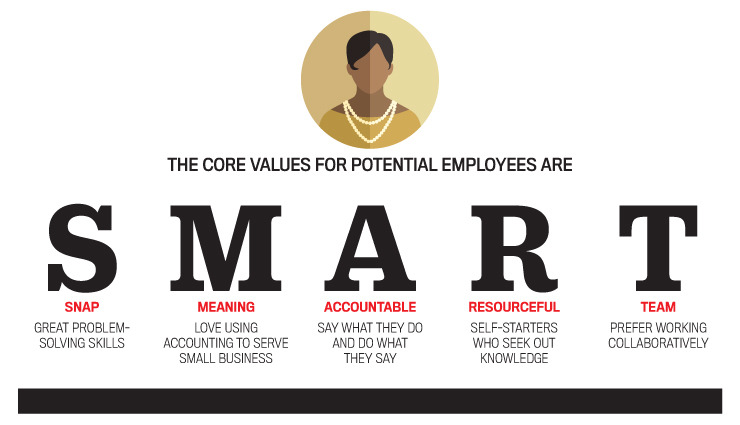

As a trusted business advisor and HR company, Insperity helped GrowthForce develop the core values for potential employees, which were defined as being SMART:

S – Snap (great problem-solving skills)

M – Meaning (love using accounting to serve small business)

A – Accountable (say what they do and do what they say)

R – Resourceful (self-starters who seek out knowledge)

T – Team (prefer working collaboratively)

When interviewing potential candidates for an accounting position based on SMART characteristics, use behavioral interview questions to identify individuals who can cite specific examples or explain how they solved an internal company or client problem. These individuals tend to speak passionately about their work or overall profession and often provide concise responses that include real-life examples without being prompted by interviewers. SMART individuals refer to team efforts and often use the word “we” instead of “I.” They are quick to point out collaborative work with other team members in achieving goals. Hiring managers should look for the candidate who can connect the dots from idea to strategy to profits and who becomes more enthusiastic about a role that gives him or her that opportunity.

Also remember the generational differences. When recruiting team members from either Generation X or Y, place an emphasis on seeking candidates who hope to work with inspirational people as well as candidates who are interested in achieving work-life balance. When targeting Baby Boomers, keep in mind that they are interested in comprehensive health insurance coverage and retirement plans. They also are frequently described as being interested in working with managers they respect.

IMPROVED EMPLOYEE RETENTION

One popular format for tracking success is a company scorecard or dashboard report (see “Dashboard Design” in this month’s issue). While traditional dashboards focus solely on financial matters, an increased alignment between HR and accounting allows for the inclusion of both financial and people-based metrics in tracking overall company health. Whenever possible, look for ways to measure and report the connection between employee productivity and progress toward company goals. For example, an expanded scorecard might track sales figures and service indicators as well as employee performance and retention.

EMPLOYEE RECOGNITION

It is often said that the best salespeople are motivated by both money and recognition. Tracking and identifying exemplary sales efforts are easy. Workers in other departments crave the same recognition, but their contributions often can be much harder to measure and are rarely communicated. When it comes to employee retention and preventing the negative human and financial impacts of turnover, employee recognition is one of a company’s most crucial tools. But no two employees are the same. As a result, when recognizing employees, a company should know what those employees value the most: time or money. If the answer is time, one popular perk is flex-time Fridays.

When it comes to recognition, incentive compensation must be tied to results, not activity. Also, there should be a line of sight between employees’ activities and the results they are measured on. Incentive pay must correlate to the key drivers of the business and the recently updated business plan.

Developing incentive pay measures for service employees is a much more difficult task. Having access to accurate job costing data is essential. Time-driven activity-based costing (TDABC) helps to automatically allocate labor costs to the clients or projects the employees are working on. This provides a view of real profitability by client, project, and employee.

Businesses need concrete ways to measure both customer and employee satisfaction. They should closely track unplanned employee turnover and recognize that planned turnover should be expected and is natural. Planned turnover can be easily identified and managed when managers have regular, honest discussions with employees about their career goals.

Incentive plans should be structured with three levels. The first level is a baseline goal, below which nobody gets a bonus. Next is a budget goal. This level is a target incentive compensation goal the company can afford and is in line with its competitors. The final level involves stretch goals. These can be determined by identifying additional key business drivers, which are then tied to an incremental goal.

DEVELOP BRAND AMBASSADORS

Once the right people are in the right seats, they need to be empowered and motivated. How does a business get employees to adopt the same brand of pride as the company’s owners?

Everyone in the company must be able to identify precisely how his or her job is tied to the company’s strategic goals, such as revenues, profit, and customer satisfaction goals. Each person should also have individual goals that help achieve the larger company goals. Manager incentive pay should be closely tied to department and company goals. Individual incentive goals should be closely tied to individual goals. Finally, incentive pay should be given out quarterly instead of annually so that the positive impacts are realized year-round. This also helps normalize company cash flow and expenses.

Taking the time to refine your company’s strategy and to recognize employees as an important revenue- or profit-producing asset can help your business grow and remain competitive. More importantly, doing so can help better meet the needs of your employees, clients, and, ultimately, shareholders.

June 2016