Environmental, social, and governance (ESG) issues aren’t new, but the amount of attention being devoted to the topic has increased significantly, compelling companies to adjust accordingly. Not only must companies work to fulfill reporting requirements (and plan for future requirements), but it’s critical that they ensure their strategies, processes, and operations remain relevant in this rapidly changing environment.

The regulatory field, in particular, is evolving quickly regarding sustainability. Governments and regulators are increasingly requiring companies to report externally in a broader manner in which multiple stakeholders’ perspectives and the long-term value-creation capabilities of the companies play a central role. This has led to a global growth in institutions, standards, and requirements focusing on how companies should report about ESG issues.

It can be rather confusing for companies to tackle ESG issues internally while at the same time keeping track of the alphabet soup of organizations and frameworks that need attention. (See Table 1 for an overview of just a handful of the abbreviations in sustainable business management.) It’s an ever-growing challenge, but the increased interest in sustainability and ESG-related reporting also provides companies an opportunity to reassess their value-creating capabilities for a variety of stakeholders. Through sustainable business management, companies can look to integrate sustainability and ESG efforts into their strategies and processes to create greater value in both the short and long term.

WHY SUSTAINABLE BUSINESS MANAGEMENT?

The idea for a certification that would attest to the qualifications and proficiency of management accountants originated in the mid-1940s, more than two decades after the National Association of Cost Accountants (NACA, as IMA was originally known) was founded in 1919. It took another 20 years for the association and its then-president, Joseph L. Brumit, to appoint a Long-Range Objectives Committee to consider the matter.

Because much of the sustainability conversation initially revolved around addressing demands about transparency and concerns of multiple stakeholder—beyond those with a financial interest of some kind—many of the rules, regulations, institutions, guidelines, and frameworks are focused on external reporting and disclosure. Yet that isn’t the end of the conversation.

Sustainability efforts also serve as a means of stimulating organizations to think about what drives their business and where and how value can be created in the long run. Through the means of ESG reporting, a company’s financial information is linked with ESG strategy and risk information. For the business, this means that ESG factors are no longer considered separately but form a core element of financial analysis and decision making.

It’s imperative that this business perspective isn’t overlooked as the integrated approach is a key element in order to get to the external reporting information that’s required in the first place. But while the external reporting pressure increases, there’s a growing risk that sustainability becomes more of a compliance exercise instead of an integrated approach toward a long-term viable business strategy.

In sustainable business management, however, the reporting component is simply a description of what a company has done and achieved over the year. The manner in which those accomplishments are achieved is what distinguishes a sustainable business. By positively impacting the environment and/or society as a whole, sustainable companies are able to create value for themselves as well as for external parties. This requires companies to take a broader, more holistic view of the business and its impact. Sustainable business management thus encompasses and affects the whole organization, from strategy to risk management to marketing to internal controls and so on.

There’s no singular model for sustainable business management. The variety and differences across companies, industries, geographies, cultures, and other factors preclude that. The key to sustainable business management is that companies make decisions with the holistic perspective in mind. This means having a vision and strategy that ensure value creation in the short and long term for the company itself and for others. To do so requires gathering the right information, having the right processes in place, and hiring the right people to make strategic business decisions.

MAKING THE TRANSITION

Switching to sustainable business management can be a challenge. Even when the external reporting aspect is well covered, the overarching aspect of sustainable business management—how it encompasses the whole of an organization—can function as a barrier. The key is to use an integrated perspective and understand the power of connectivity.

This can be accomplished by embracing integrated reporting—not only the reporting aspect, but specifically the focus on integrated thinking. Many tools are already available for companies to start with its implementation. For example, following the main elements of a traditional performance management system can provide you with some important ingredients to a sustainable business:

The strategic plan. This is the starting point for sustainable business management. The strategy shows where the company is heading and how it aims to get there. A sustainable strategy should align with the financial and operating objectives, showing how the company will use its (scarce) resources and to what extent sustainable decision making contributes to the strategic goals of the company. Thus, management doesn’t need to formulate a separate sustainability strategy; rather, it can embed sustainability into the company’s strategic planning and then effectively communicate and implement the plan. The end result is that sustainability becomes an integral part of the organization.

Integrated financial analysis. While integrating ESG issues into the strategy is a start, it’s far from sufficient. Sustainable thinking needs to be integrated into decision making and analysis. A translation is needed between the strategic objectives and the business of the organization. For this, a deep understanding of the organization’s business model, resource usage, and impacts is important. It requires the organization to take a holistic view on long-term risk management and the impact of ESG factors to understand how it can affect day-to-day operations and include this in the financial analyses.

Performance management. Performance information is essential for sustainable business management, so ESG information needs to be included in the performance management systems. Based on a thorough understanding of how objectives, risks, resources, and operations are interwoven, identify useful and operational ESG-related key performance indicators (KPIs) that can be cascaded throughout the organization metrics.

There are myriad ESG-related KPIs from which to choose, but selecting the right ones involves ensuring they’re measurable, reliable, and related to the value drivers of the company. For a suitable performance management system, this calls for a broad mindset that looks beyond established silos. It also requires a vast governance and internal control system safeguarding the quality and reliability of the information, both financial as well as ESG.

Reporting. One of the biggest obstacles to implementing a sustainable business is when management lacks a sense of urgency on the topic. To resolve this, management reporting on both ESG and financial information is key. With proper performance measurement and reporting procedures in place—ones that generate complete, useful, and actionable information—it’s possible to show the urgency of these ESG drivers to top management. Only then will good sustainable decision making be possible.

Although integrated thinking can take many forms in companies, starting with these four components—strategy, analysis, performance management, and reporting systems—is essential to moving sustainability beyond being a mere compliance exercise. Companies that implement sustainable business management recognize that their ability to grow, create value, and serve consumers is inseparable from sustainability commitments. Finance and accounting teams play a critical role by steering the business strategy accordingly and ensuring it’s supported by business operational processes.

When sustainable business management standards developed in the field align with the goals and needs of a company and its stakeholders, everyone benefits. Companies that understand that see ESG information not as a disclosure risk, but rather as a way of including a long-term, risk-aware vision in their day-to-day operations and decisions.

NINE PRINCIPLES OF SUSTAINABLE BUSINESS MANAGEMENT

In order to support the development of sustainable business management and to stress what the finance function needs in these efforts, IMA® (Institute of Management Accountants) launched the Sustainable Business Management Global Task Force in September 2021. In addition to advocating for sustainable business management on behalf of the management accounting profession as well as accountants and finance professionals in business, the task force looks to educate IMA members and the business community on the role that accounting and finance professionals play in respect to sustainable business information and management.

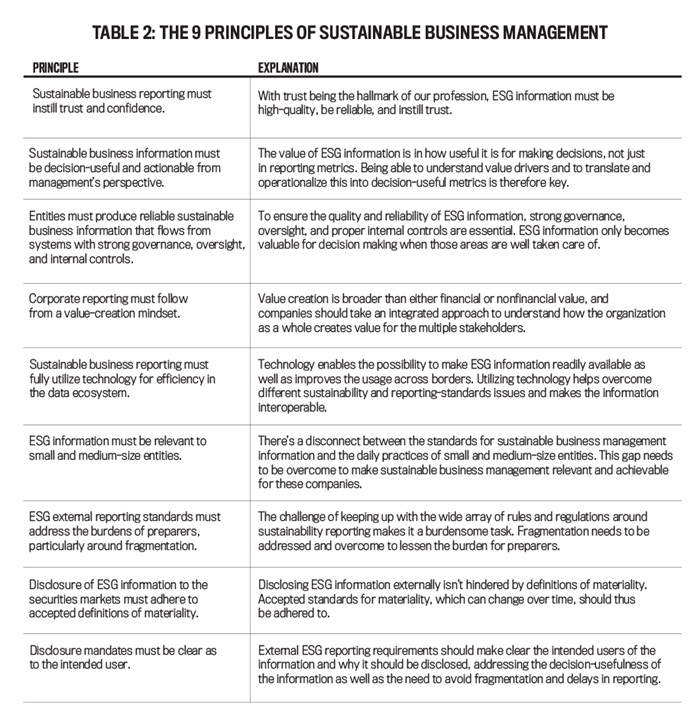

In November 2021, the task force issued a statement of position that addresses nine principles IMA believes should be taken into account by the profession while advancing the field of sustainable business management:

- Sustainable business reporting must instill trust and confidence.

- Sustainable business information must be decision-useful and actionable from management’s perspective.

- Entities must produce reliable sustainable business information that flows from systems with strong governance, oversight, and internal controls.

- Corporate reporting must follow from a value-creation mindset.

- Sustainable business reporting must fully utilize technology for efficiency in the data ecosystem.

- ESG information must be relevant to small and medium-size entities.

- ESG external reporting standards must address the burdens of preparers, particularly around fragmentation.

- Disclosure of ESG information to the securities markets must adhere to accepted definitions of materiality.

- Disclosure mandates must be clear as to the intended user.

The nine principles are structured in such a manner that the list starts from an internal perspective (the core of sustainable business management) and gradually moves toward a more external perspective (how to align with the external reporting requirements). See Table 2 for a brief overview of why each principle is relevant.

These principles are fundamental to building a successful and sustainable accounting ecosystem. An important characteristic is that they’re adaptable to a changing environment. As the reporting landscape seems to change in an ever-increasing pace, so should the management accounting profession be adaptable.

OPPORTUNITIES FOR MANAGEMENT ACCOUNTANTS

Sustainable business management is no longer a “nice to have.” It’s essential for a business to survive in the long term. And it should be seen not as a hurdle but as an opportunity to recognize the real value drivers of the organization and to incorporate those drivers into the company’s strategy, analysis, performance management, and reporting. Thus, sustainable business management provides a massive opportunity for management accountants and finance professionals to take the lead.

As the IMA Management Accounting Competency Framework states, management accountants are able to connect many different domains within the organization—all of which play a key role in achieving sustainable business management. The capacity of management accountants to navigate the domains of strategy, planning, and performance; reporting and control; technology and analytics, business acumen and operations; leadership; and professional ethics and values puts them in the right position to play a leading role in achieving sustainable businesses. They can work with different streams of information and deal with conflicting demands and interests. They can help management to understand and present ESG information, ensuring that it isn’t kept in its own silo but becomes an integrated part of the organization’s operations.

Figure 1 includes a few key ways that accounting and finance professionals can bring sustainable business management to their organization. Whether it’s balancing the different interests of multiple stakeholder groups, aligning financial and nonfinancial goals, breaking down silos to have the right information available, or navigating complex data to provide relevant information for decision making, accounting and finance professionals are well positioned to weave sustainability into the fibers of the organization.

The opportunities are ample, from including ESG factors in pricing decisions to adjusting the decision-making process in such a way that ESG factors are made relevant for the whole supply chain to ensuring that long-term environmental risks are at the core of strategic decision making. Rarely has the profession been in the position to play such a key role in a whirlwind of changes to society. Sustainability is the future of finance, and finance is the future of sustainability. These are challenging but exciting times to be a finance and accounting leader.

Six Pitfalls to Avoid in Sustainable Business Management

1. Reinventing the wheel

A lot has been done in sustainable business management already. Make sure to use this knowledge. Best practices are provided by multiple standards providers while institutions like the United Nations Sustainable Development Group, the GRI, and the SASB give relevant indicators of what might be useful to measure. You don’t need to figure it all out yourself.

2. Doing it all at once

There’s no clear recipe for becoming a sustainable business, but it’s certain that it takes time. Know where your company can make a difference—a key area in which the organization can perform well—and try to focus on that first. That’s where most of the value can be created.

3. Assuming one size fits all

There isn’t just one right way to become a sustainable business. Each company needs to take its own journey. Learn from best practices, but stick to what’s important and works for your company.

4. Staying siloed

Sustainability efforts can’t be done without collaboration between teams. One important factor to a successful implementation is that information is shared throughout the company and that silos between departments are broken down.

5. Waiting to get started

Sustainable business management is gaining momentum, but waiting for regulatory frameworks or requirements that exactly fit your company’s situation will make you lag behind. Start adjusting to this new reality now, or the organization might simply be too late to keep up with competitors.

6. Forgetting why you’re doing this

Sustainable business management is an opportunity. Understand and keep in mind the long-term value of the effort—how it provides a deeper understanding of the business and helps improve decisions on a day-to-day basis. The time of greenwashing is over. It’s time to make a real difference.

April 2022