2023 STUDENT CASE COMPETITION

The Student Case Competition is sponsored annually by IMA® to provide an opportunity for students to interpret, analyze, evaluate, synthesize, and communicate a solution to a management accounting problem.About a month ago, Thomas Foxwell, president and CEO of Kunapipi Gardens, a 738-room resort hotel, met with CFO Prisha Patel to discuss the company’s performance. Foxwell has been CEO of Kunapipi Gardens for the past four years after the prior CEO was fired after the company’s earnings before interest, taxes, depreciation, and amortization (EBITDA) had fallen nearly 50%. During his tenure, Foxwell hasn’t seen much growth in revenues, but EBITDA has increased 29%. The board of directors has been placing increased pressure on Foxwell to get back to the record revenues and EBITDA of a decade ago. As Foxwell and Patel looked over the reports together in one of the hotel’s restaurants, Foxwell summarized the situation:

We started out as a midsize hotel in Lake Tahoe, steadily expanding to where we are today. The problem I have is that our annual income statements are an outgrowth of what we used more than 40 years ago. Back then, we were a 180-room hotel. Over the years, we added two new buildings for hotel rooms, added an event center 20 years ago, and, more recently, added a golf course and spa. Our income statement treats the organization as a hotel with multiple departments, but I think of us as a multidivisional company. Each line of business should be evaluated on its own merits. Can you put together a new income statement that better reflects the performance of our various divisions?

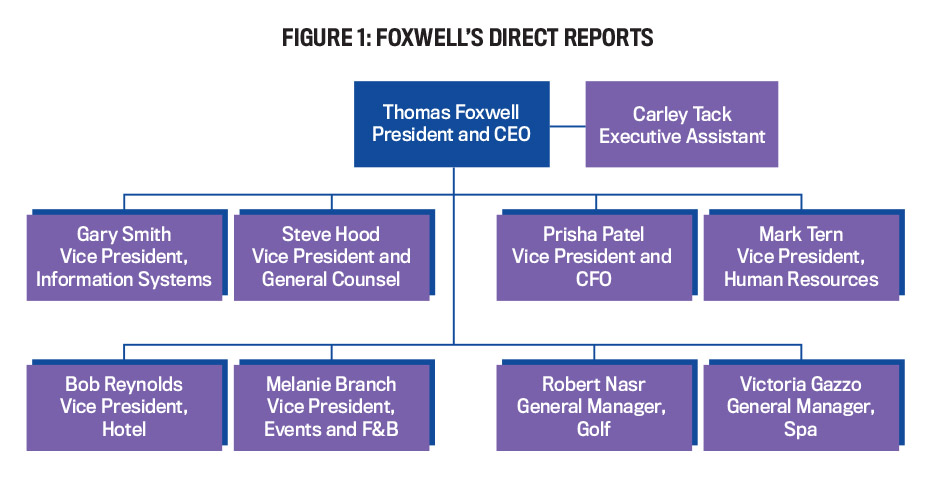

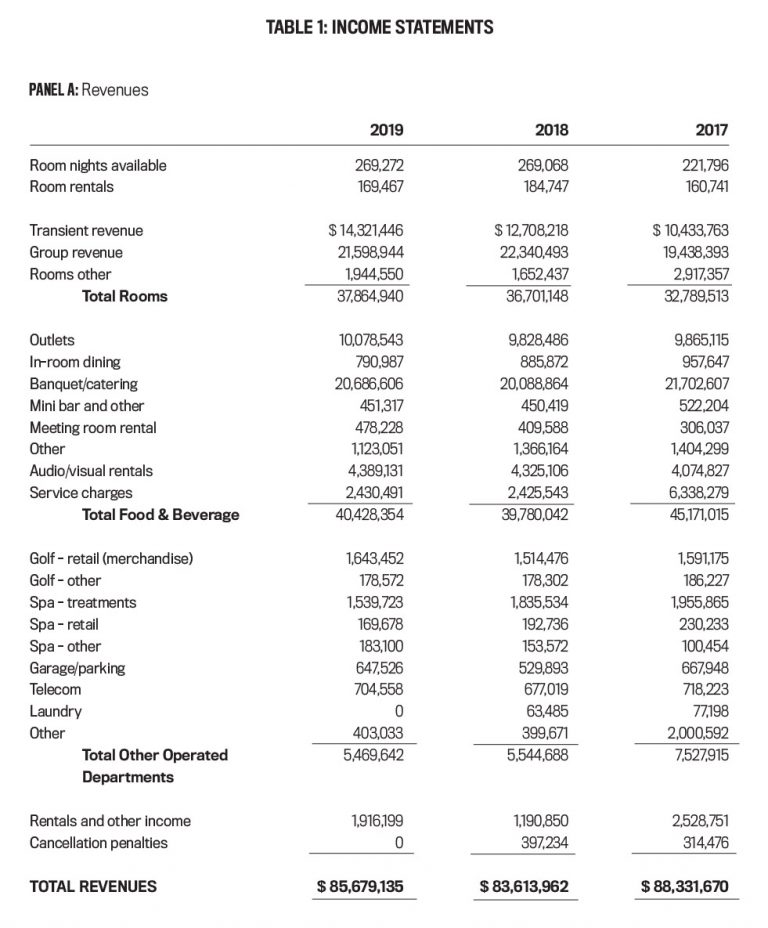

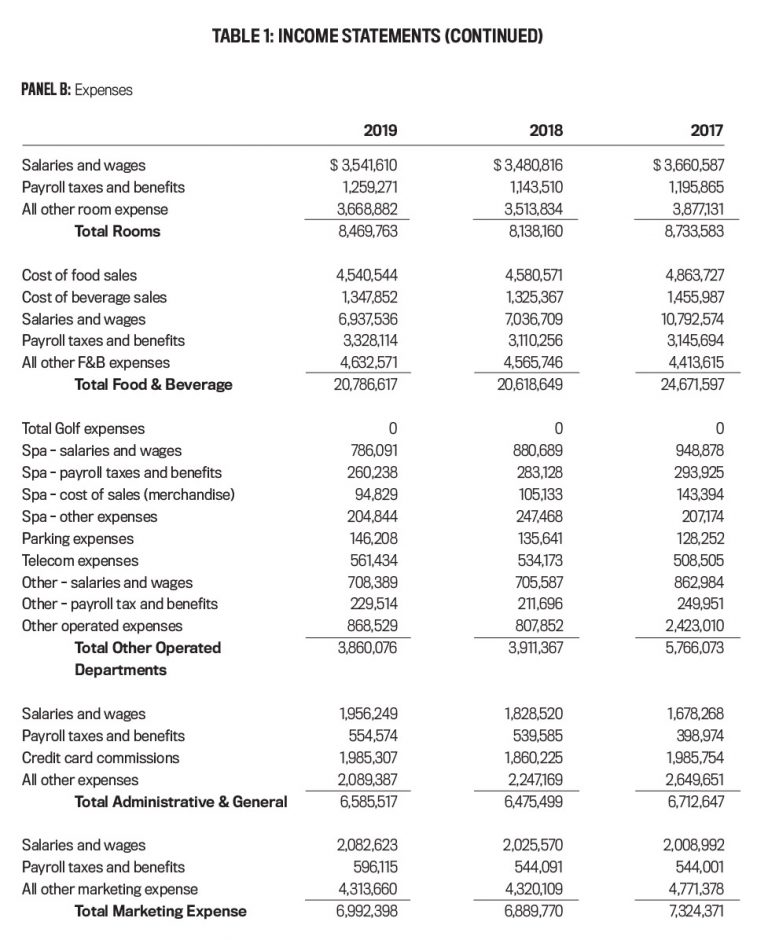

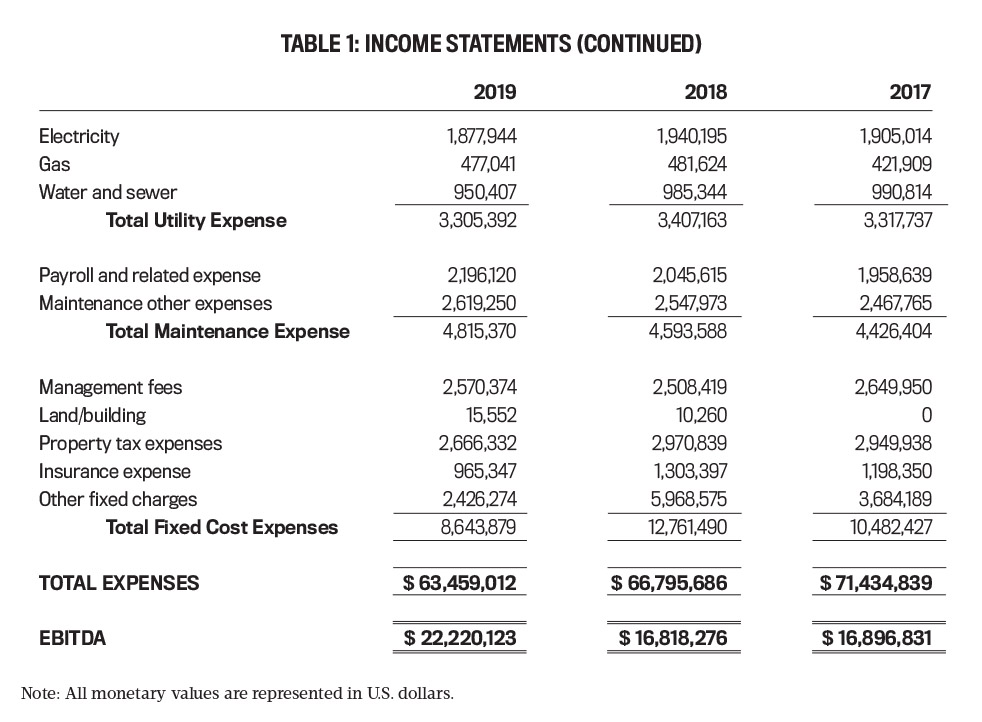

Foxwell felt he needed to better understand how the different managers were performing. With eight senior managers reporting to him at the moment, Foxwell can be thought of as an investment center manager (see Figure 1). The managers of the different company divisions—Hotel, Events and Food & Beverage, Golf and Spa—are treated as profit-center managers, while his other direct reports are cost-center managers. The accounting department has followed the industry practice of preparing income statements in accordance with the Uniform System of Accounts for the Lodging Industry (USALI). (See Table 1 for income statements from the past three years.)COMPANY BACKGROUND

Kunapipi Gardens was developed in the 1970s when Nevada’s Reno-Tahoe area established itself as a four-season resort destination. Since then, Reno has grown into a large city (population greater than 260,000) with multiple high-end resorts, golf courses, spas, a thriving business center, and numerous high-end retail areas. The Reno-Sparks metro area is one of the 150 largest in the United States. Just to the west, in California, the Tahoe Basin area has a population of 50,000 that balloons to 300,000 on peak days. With its widely acclaimed international airport, the Reno-Tahoe area’s resorts host golf tournaments, business meetings, and group events in addition to normal business travel and tourism.

For many years, hotels were simply buildings for accommodating transient guests. Full-service hotels provided food and beverage (F&B) outlets to feed guests and some event space for group meetings, social functions, etc. While managers followed the performance of their F&B outlets, the event space received little attention. Responsibility for the execution of events was usually assigned to the F&B manager because banquets and snacks are often a major part of business meetings, proms, wedding receptions, and conferences, among others. Throughout the 1980s, many full-service hotels viewed their event space as an adjunct to their principal line of business (providing rooms for travelers). Similar to casinos in the 1960s, where the hotel was seen as an adjunct to their gaming business (to keep gamblers at the hotel, rooms were “comped,” or provided free), hotels typically focused on maximizing hotel room occupancy (i.e., rooms rented divided by rooms available, a measure of capacity utilization) while ignoring event space utilization. Prior to the pandemic, hotel occupancy rates averaged 80% while 30% of event space was utilized.

For many years, hotel companies focused on revenue per available room (RevPAR) as a key performance measure. As the name implies, this measure represents room revenue divided by the rooms available, and it captures the impact of pricing (i.e., average daily room rate, or ADR) and occupancy. It’s a leading metric noted in two established hospitality accounting textbooks, Hospitality Industry Managerial Accounting by Raymond S. Schmidgall (2006) and Accounting Essentials for Hospitality Managers by Chris Guilding (2009). Both textbooks cover multiple performance measures in the context of financial statement analysis, with the emphasis being on rooms and F&B operations. They place RevPAR front and center in their coverage, followed by occupancy, average food service check (i.e., food revenue divided by the number of guest checks), food-cost percentage, and seat turnover. No mention is made of events, despite the significant growth in weddings, business banquets, etc., that occurred in the two decades prior to these textbooks being published. During the 1970s, an accountant started a business based on gathering three measures from hotels: room revenue, rooms rented, and rooms available. From these three metrics, one can compute daily occupancy, ADR, and RevPAR. Hotels submitted daily reports on postcards, mailing them to the accountant’s benchmarking firm. Recording this data, the firm sold anonymized, weekly, and/or monthly reports to participants. By providing this confidential data, hotels were able to benchmark their property to competitors (as a group, not individually, since individual hotel data was confidential). Today, the accountant’s firm is a global hospitality benchmarking firm that has more than 80% of U.S. hotels submitting their data, accounting for more than 95% of all hotel rooms. Yet despite a growth in event spaces, not a single report has performance data on hotel event space; the only data available comes from income statements in the USALI format, which has a departmental focus with events lumped into various departments, but primarily into the F&B department. Hotel sales departments usually handle both rooms and events. Years ago, hotel salespeople would negotiate away event fees in order to book hotel room nights. This was done because hotel sales staff performance was based on room nights booked, not overall revenue. A large group with thousands of room nights, such as a national meeting of automobile dealers, would be told that morning and afternoon breaks would be provided free of charge if attendees booked a specified number of rooms. Meeting space would be provided free of charge if a higher level of room bookings was achieved and the same with audio/visual equipment rentals. Hotels like Kunapipi did this because they viewed themselves as a hotel, and management’s goal was to maximize RevPAR through higher occupancy and higher ADR. According to Foxwell, this perspective is flawed. For example, many airlines began to think of themselves as providers of travel services. This led to Air France owning Le Méridien (now part of Marriott), Swissair owning Swissôtel, and United purchasing Westin, among several examples. United even went further by purchasing Hertz Rent-a-Car and changing the corporate name to Allegis. While these alliances didn’t last, one thing the airlines didn’t do was give away hotel rooms or car rentals simply to get travelers into airline seats. It’s safe to assume that most people would view such an idea as crazy—which, following Foxwell’s thinking, makes one wonder why hotels would think differently. Is this perspective the product of an organization’s accounting that doesn’t match its strategy and organizational form? Foxwell thought so. But serving the events market (corporate meetings, sales meetings, weddings, professional conferences, etc.) shifted the company’s customer base. Many of Kunapipi’s new customers expected better facilities with bundled services (i.e., direct billing, bidding on the event, and meeting space along with hotel rooms and banquets). Foxwell believed a new incentive compensation plan, along with a new reporting format, might be needed to get the performance being sought by the board of directors.

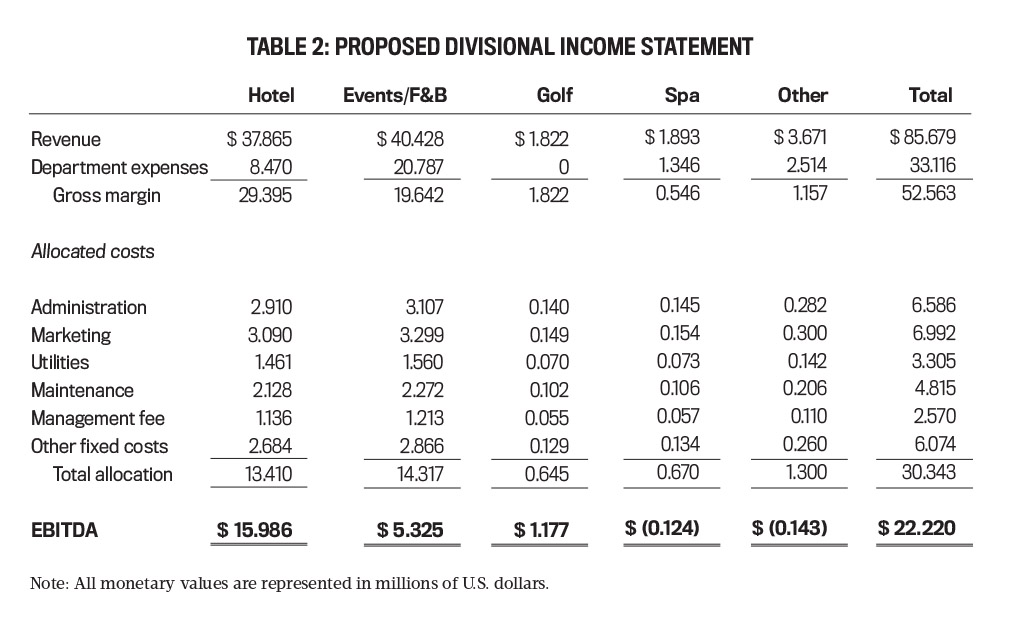

THE COMPLAINT

Late last week, Patel distributed her proposed divisional income statement (see Table 2). This statement summarized and reorganized what was on the current statement. She listed five separate areas of responsibility: Hotel, Events, Golf, Spa, and Other. The first four were the profit centers, but the last category was a collection of items that Patel was unsure about. She felt that she’d need more input from Foxwell and the other members of the senior executive team to refine the new income statement. In the monthly executive team meeting, Melanie Branch, VP of Events and F&B, expressed some concerns over the new format:I think this new approach is a good idea, but it needs some improvements. I don’t think this statement accurately reflects my contribution to the organization. Last year I booked more than 40 major events, with an average attendance of 300 persons, staying an average of five nights. These numbers suggest that my work brought in more than 60,000 room nights. The marketing, sales, negotiations, and successful executions have made us a leader in the events business in the Reno-Tahoe area. Bob [Reynolds, VP of Hotel] gets all of the credit for those room rentals, but—and I hate to say this—he hasn’t done anything to capture that incremental business. Now if you look at Bob’s business, he rented about 169,000 rooms last year. If he didn’t have the customers I brought, his revenues would have dropped more than $13.4 million. But since his marginal costs are low, most of that would have fallen to his bottom line. His gross margin and EBITDA would have dropped about $10 million.

Foxwell recognized right away that Branch had a valid point. She should be recognized and awarded for doing a good job—for working hard and making the right decisions. It was clear that the proposed income statement wasn’t quite there yet. Having taken a management accounting course, Foxwell was aware of transfer pricing. While the examples he’d seen were all in a manufacturing setting, he wondered why the Hotel department couldn’t sell rooms to the Events and F&B department. But was he wrong? Foxwell asked Patel to evaluate the idea further and come to the executive leadership team’s meeting the next month with a revised income statement that would incorporate a transfer price that the two managers (Branch and Reynolds) could agree upon. Foxwell also thought that a revised divisional income statement like the one proposed by Patel might require a new incentive compensation scheme for Kunapipi’s senior leadership. Under the current arrangement, the executives receive a bonus based on EBITDA. The idea is to align the interest of the executives with that of Kunapipi’s owners. But Foxwell wondered whether a decentralized organization should have a compensation plan where divisional VPs have their bonus based on divisional performance rather than corporate performance. If so, he wondered whether this might adversely impact organizational loyalty and increase fighting among the company’s senior leadership. Perhaps a blended approach would work best. Foxwell thought that he and his team needed to consider the compensation plan carefully before any changes were made. Two other concerns had also arisen. Recently, the executive leadership team had thought about closing the golf course and spa. The land around the hotel is valuable, and the board of directors asked Foxwell to look into selling the land to a local developer who would turn it into a shopping center. A study found that most golf patrons were attending events. Apparently, the golf course was a major selling point for events, and Branch feared that her department’s events business would drop 20% to 40% if the golf course were to close. For this reason, the board decided to keep the golf course. But Foxwell wondered if Robert Nasr, general manager of the golf course, should remain as a profit center reporting to him. The rationale behind closing the spa was due to its performance. Last year, the division lost more than $100,000. Neither Reynolds nor Branch felt that closing the spa would have an impact on the performance of their profit centers. Foxwell, Patel, Reynolds, Branch, and Kunapipi’s other employees hold unique perspectives and interests, although they all share the common goal of ensuring the achievement of its mission over the long term. You’ll need to observe the rights and interests of all parties in assessing Kunapipi’s possible avenues forward.ASSIGNMENT QUESTIONS

- Critically analyze the strategic position of Kunapipi Gardens.

- What are the pros and cons of the current system (income statement) described in Table 1?

- To what extent does the system in Table 2 solve these issues or create new problems?

- Based on your analysis so far, please suggest an “ideal” performance measurement system. Feel free to make appropriate and reasonable assumptions and to discuss alternative designs.

August 2022