One of the recent examples of this call is the 2018 letter to Standard & Poor’s 500 CEOs from Larry Fink, CEO of BlackRock (the world’s largest asset owner), who made a compelling case for achieving long-term value creation through corporate purpose. He said, “Society is demanding that companies, both public and private, serve a social purpose. To prosper over time, every company must not only deliver financial performance, but also show how it makes a positive contribution to society.” A few months earlier, Apple CEO Tim Cook used similar language about the role of business in society.

One way for business organizations to address this challenge is to define their purpose and align it with a sustainable, value-creating strategy that can make a positive contribution to society.

How can management accountants help? What’s the role of management accounting and reporting practices? Through which mechanisms can CFOs and the finance organization make sure that the promise of sustainable business strategy and inclusive business models has positive impacts on stakeholders in practice?

HOW TO EMBED PURPOSE

Although the benefits of purpose on corporate performance are starting to be recognized by both business leaders and academics, very little evidence exists about how purpose can be effectively and practically embedded into decision making and strategy execution. We suggest that if performance management and measurement systems are well-designed, management accountants can use them as a powerful and positive tool for aligning purpose with sustainable, value-creating strategy and business models. By leading in the design and implementation of comprehensive performance management and measurement systems, management accountants and the whole finance organization can play a vital role in helping their organization embed purpose into action as a business path for achieving positive social impact and sustainable business performance.

Research at the Center for Strategy, Execution and Valuation at DePaul University focuses on the following definition of the purpose of a company, which is useful in guiding management and board actions: “An effective statement of corporate purpose should answer the two-part question: Why does the company deserve the commitment and support of its stakeholders, and what unchanging principles will guide management’s actions?” (See “The Purpose of the Firm, Valuation, and the Management of Intangibles,” Journal of Applied Corporate Finance, Spring 2017.)

Building on a series of case examples—Unilever, Barilla, and EasyJet—we suggest that by aligning corporate purpose to sustainable, value-creating strategy, companies will be ready to move from “business as usual” to what we call “Business2030.” Business2030 is a reference to Sustainable Development Goals (SDGs), which can provide a clear signal that a business takes seriously its broader societal role as a positive force rather than saying that recognition of the SDGs is a definition of a purposeful company per se. In doing so, we emphasize the role of Integrated Thinking in enabling a comprehensive set of relationships and performances to be positioned at the core of an organization’s business model and strategy. We also explore the main challenges and opportunities for management accountants as well as for CFOs and finance professionals in general.

THE NEED FOR INTEGRATED THINKING

Since September 2015, when 193 heads of state and government meeting at the United Nations General Assembly agreed on 17 Sustainable Development Goals (see Figure 1), it became clear that public opinion and policy makers expect business organizations to recognize the value of the United Nations’ Agenda 2030. The SDGs define global priorities and aspirations for 2030 and rely on the critical role of business organizations in delivering on the promise of sustainable and inclusive development (see “Sustainable Development Goals: Integrating Sustainability Initiatives with Long-Term Value Creation,” Strategic Finance, September 2017).

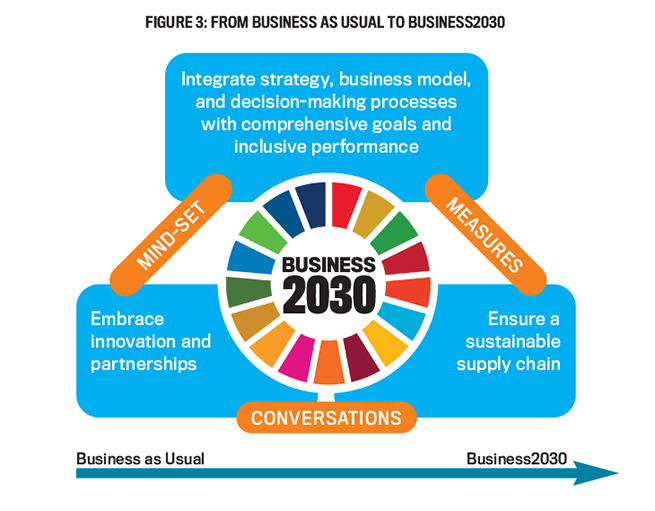

Making SDGs happen will be a great opportunity and challenge in the years ahead. Large, medium, and small companies can move from business as usual to Business2030, a new way of doing business that’s aligned with long-term commitment and responsible actions toward multiple and diverse stakeholders. Business2030 entails attention to integrating comprehensive stakeholder relationships within strategy, business models, and decision-making processes; an openness to innovation and partnerships; and attention toward ensuring sustainable supply chains.

As business organizations become familiar with SDGs, they have the opportunity to learn to understand, measure, and communicate the comprehensive relationships that make up their business model. Ultimately, they can learn to plan, act, and report in an integrated way. Recently popularized by the International Integrated Reporting Council (IIRC), the term Integrated Thinking refers to the conditions and processes that are conducive to an inclusive process of decision making, management, and reporting based on the connectivity and interdependencies among a range of factors that affect organizations’ ability to create value over time. The Framework developed by the IIRC (http://bit.ly/2DCvJno) suggests that the fundamental concepts of Integrated Thinking (and Reporting) are represented by the multiple capitals—or stores of value—that an organization uses and affects, as well as the process of creating value over time.

This value is embodied in the capitals, also referred to as resources and relationships. Organizations depend on six different types of capitals: financial, manufactured, intellectual, human, social and relationship, and natural (see “Leading Practices in Integrated Reporting,” Strategic Finance, September 2014).

The relationship between Integrated Thinking, the IIRC Framework, and Integrated Reporting is an important one and is mirrored in the evolution of the SDGs. The SDGs have been popularized by the icons developed to represent the 17 goals and are seen to have substance by the detail of the 169 targets and 304 indicators. In some ways these are the equivalent of the IIRC Framework and detailed work on Integrated Reporting. What’s interesting is that there’s less talk about the mind-set and purpose behind the SDGs. Sustainable development is broadly defined as the combination of economic development, social inclusion, and environmental sustainability. And within this principle, the aim is to stimulate action on five key themes: people, planet, prosperity, peace, and partnerships.

The defining principle of sustainable development and the five “Ps” is the Integrated Thinking or purpose behind the SDGs. The goals, targets, and indicators are useful snapshots of what can be achieved and measured. But without the organizing principle and aims, the risk is that they become checklists that are peripheral to the core of the operating mind-set and everyday thinking. Progress can be made by reference to the goals, targets, and indicators, but can sustainable transformation and constant innovation be achieved without a purposeful mind-set change? Ultimately, it’s the mind-set change that keeps the purpose in the forefront of thinking and allows companies and people to respond to the threats and opportunities that may be particular to their industry, sector, geography, and context in a way that contributes meaningfully to the overall purpose of the organization and the underlying principle and themes of the SDGs.

WHAT IS PURPOSE?

Purpose is an organization’s enduring reason for being. It defines the organization’s existence and societal contribution in a way that aligns the long-term financial performance with benefits to all stakeholders and society. If the mission of a business refers to what the organization is trying to accomplish, the purpose is the “why” (for example, see Simon Sinek, Start with Why). Purpose reflects something more aspirational—it isn’t about just rephrasing the business model. It can become a way to understand where strategy comes from and what kind of outcomes and performance are being sought.

If Business2030 is to enable a change from business as usual, it also is meant to indicate that it’s about the mind-set change reflected in the SDGs rather than simply reporting on the goals, targets, and indicators. And, of course, it means purposeful thinking beyond 2030. Through Integrated Thinking, the comprehensive financial and nonfinancial relationships and resources that make up purpose become part of the strategy and processes of long-term value creation. As Larry Fink urged, a company’s statement of long-term value-creating strategy is essential to understanding that company’s actions and policies. This is an area where performance trade-offs between long-term sustainable value creation and short-termism are likely to arise (see “Creating Greater Long-Term Sustainable Value,” Strategic Finance, October 2018).

We offer a word of caution when considering performance measures because the performance metrics that are chosen send signals about what a company considers important. Make sure you think through this process very carefully and choose the right metrics that would apply to Business2030. This is where management accounting can play a major role as performance metrics can produce desirable behaviors but also can produce unintended negative consequences.

LINKING PURPOSE TO PERFORMANCE

Now let’s look at three case examples of companies that have made and are making strides with purpose.

Unilever

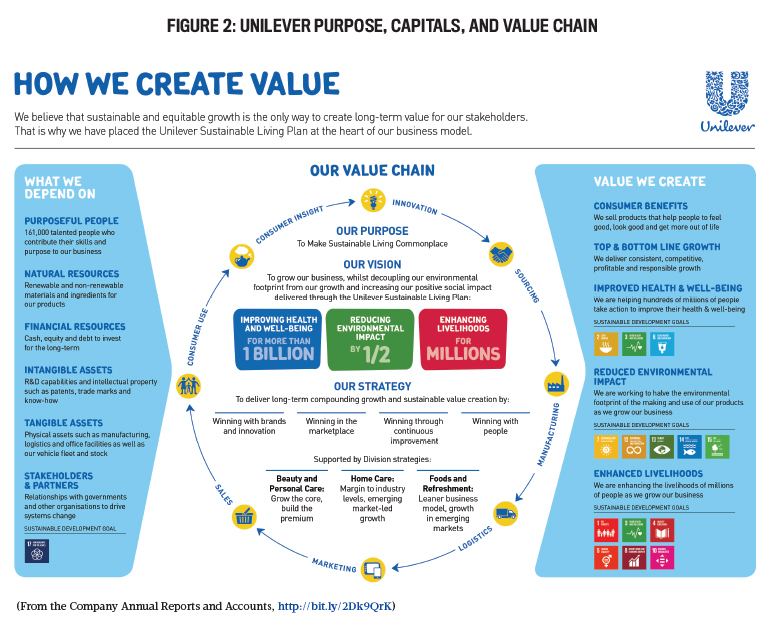

Unilever was one of the pioneers in understanding the importance of a purposeful business. In 2001, it bought the American ice cream manufacturer Ben & Jerry’s, which had the following core values “…to make the best possible ice cream in the best possible way” (see www.benjerry.com/values). Ever since, the company has been striving to make acquisitions with a clear purpose in mind: “to make sustainable living commonplace.” In doing so, Unilever has put a “sustainable living plan” at the heart of its business model (see Figure 2). This has defined Unilever’s strategy and has impacted brands and products, behavior, and partnerships across the company value chain.

Interestingly, the Unilever Sustainable Living Plan provides a detailed path for how the company aims to achieve sustainable growth while delivering its purpose and vision. It covers all aspects of Unilever business across its value chain from operations to sourcing to the way consumers use their products. The plan is designed to drive profitable growth and fuel innovation so that all Unilever stakeholders benefit.

Within Unilever, value creation depends on a series of capitals (see Figure 2). The human capital (“Purposeful People”) includes talented individuals who contribute their skills and purpose to the business. “Natural Resources” comprise renewable and nonrenewable materials and ingredients for Unilever products. “Financial Resources” include cash, equity, and debt to invest for the long term. “Intangible Assets” comprise capabilities and intellectual property such as patents, trademarks, and know-how.

“Tangible Assets” are physical assets such as manufacturing, logistics, and office facilities as well as vehicle fleet and stock. Finally, “Stakeholders and Partners” consist of the relationships with governments and organizations to drive systems change. Through the energizing force of purpose and the dialogue in which these capitals and relationships are embraced, Unilever’s business models create value in terms of consumer benefits, top- and bottom-line growth, improved health and well-being, reduced environmental impact, and enhanced livelihoods. All these are linked to achieving the SDGs.

Barilla

The Annual Report of Barilla (the Italian food company) is named after the company’s purpose: “Good for You, Good for the Planet.” This translates into a mission where all products and brands must bring to the world food that is good, healthy, and sourced from responsible supply chains inspired by the Italian lifestyle and the Mediterranean Diet. Barilla’s mission defines its business model that’s rooted around the three benefits for people: Good Food, which means gastronomy, flavor, culinary experience, pleasure, and conviviality; Healthy Food, which means selected raw materials, clean and safe recipes, and balanced nutritional profiles to support correct lifestyles; and Food Sourced from Responsible Supply Chains, which means purchasing ingredients and processing them in a way that’s sustainable, transparent, and respectful of people, animals, and the environment. In pursuit of this mission, Barilla says it intends to invest in four dimensions:

- increasing the value of brands, their distinctive nature, and the emotional bond they form with people;

- providing products with superior quality, including from a nutritional point of view;

- enhancing the sustainability and transparency of the supply chains end to end from “field to fork”; and

- incentivizing an entrepreneurial spirit among Barilla people.

EasyJet

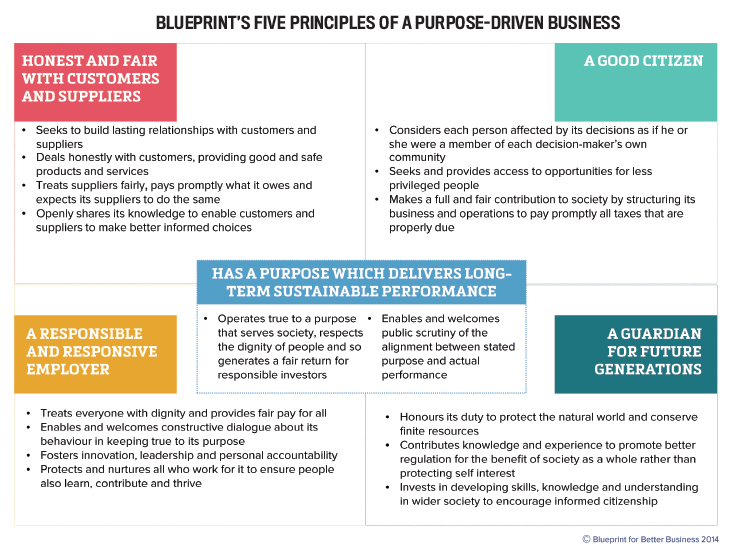

EasyJet, the European low-cost airline, has used the framework of A Blueprint for Better Business to communicate how it seeks to align its operational thinking with purpose. EasyJet has defined its purpose as “connect people across Europe for work and play.” The company suggests it should do this by challenging itself and the industry “to make travel easy and affordable for all” through a spirit that defines the company as it tries “to do things in the right way, every day” for people, customers, society, and the environment. While safety (through security and supply chain management, managing crew fatigue, protecting passengers and crew from disruptive behavior, and more) is EasyJet’s “number one priority,” the company has used Blueprint’s model to communicate its Integrated Thinking about purpose by focusing on the following areas:

- Honesty and fairness with customers and suppliers (by supporting passengers during disruption, supporting passengers with special assistance, building positive supplier relationships, and by preventing bribery, corruption, and modern slavery);

- Responsible and responsive employer (by employing people locally, working with trade unions, encouraging a diverse workforce, and by offering fair rewards);

- Guardian for future generations (by investing in efficient aircraft, by operating efficiently, and by encouraging sustainable tourism);

- A good citizen (by partnering with UNICEF, emergency charity appeals, local donations for employees, and by reducing aircraft noise).

TOWARD PURPOSE-DRIVEN ORGANIZATIONS

The U.N. SDGs, the IIRC Framework, and the principles elaborated by Blueprint potentially suffer from the same flaw: They tend to look to implied tangible outcomes—the first to an inventory of measures, the second to better reporting, and the third to specific identifiable actions or outcomes. Fundamentally, the SDGs, the IIRC, and Blueprint advocate something more: behavioral shift, integrated thinking, and changed mind-set, respectively. A checklist or event or initiative may have good outcomes, but the risk is that they are actions taken alongside core operating decisions, so they may be peripheral and limited in impact. Thinking differently about how the operational model is designed and used leads to long-term systemic change and constant innovation to improve outcomes.

The company examples described in this article illustrate how important it is to link thinking (at different levels from board engagement to operational engagement) and relationships (stakeholder engagement) to implement change and move toward Business2030 through sustainable strategy. This message has also been included in innovative corporate reports and disclosures. The danger, however, is to depend on outcomes (also backed up by compliance with new regulatory standards) as catalysts for new thinking rather than to engage in the thinking needed to produce unique outcomes.

Organizations are likely to successfully embrace the comprehensive approach of Business2030 only if they can engage stakeholders in meaningful conversations and enable people to move toward purpose-driven change. Then measures, reports, and actions will support and sustain this path. How can CFOs and management accountants be part of the solution and contribute to these conversations?

FINANCE AND THE PURPOSE-DRIVEN ORGANIZATION

New regulations and novel investor policies have contributed to the adoption of organizational practices tailored to better understand, redesign, and maintain sustainable business models. Taken together, this means that new business opportunities are opening for companies that are able to operate true to a purpose that drives them to be a force for good in societies in which they seek to prosper. An integrated approach—Business2030—can take into consideration how the interests and the contributions of a series of stakeholders that participate in the execution of the strategy are linked in the business model through innovation, partnership, and sustainable supply chain (see Figure 3).

Key features of a 2030 business are in the boxes. Mind-sets, measures, and conversations are levers you must manage carefully to get there. CFOs in particular have the opportunity and responsibility to explain the impact for all stakeholders, not just the investors, of this way of thinking on the sustainable prosperity of the business.

Business2030 calls on the CFO and the finance organization to make corporate purpose visible as a fundamental pillar of the management system of the business. As we have noted, Business2030 builds on Integrated Thinking, which is about understanding, measuring, and connecting a comprehensive set of relationships and performances with corporate purpose. It involves identifying, executing, and monitoring business decisions and strategies for long-term value creation. Integrated Thinking builds on the need to reconcile competitiveness and sustainable growth within the context of inclusive business models to take advantage of the opportunities and face the challenges of the market. But such a comprehensive approach brings potential trade-offs to the surface, leaving accounting and reporting practices with a central role in making sustainable strategies happen in practice. But how?

Accounting and reporting practices offer tools and engagement platforms that can go beyond communication of the initiatives of sustainability through a set of ad hoc targets and key performance indicators. They go deeper into the business operations and the process of value creation, and they can shed light on the integration that takes place as the business model unfolds. In this area, management accountants can lead the search for comprehensive performance by suggesting pragmatic solutions to monitor, improve, and communicate the ways in which such an inclusive business purpose may be converted into added value for stakeholders.

Most important, management accounting signals and shapes behaviors and actions as well as records outcomes. Business2030 is about people thinking about what they do and why they do it. Tools, platforms, and indicators need to help create the conditions that enable that thinking: The tools need to be used by people making decisions in pursuit of purpose rather than compliance with tools, platforms, and indicators becoming the purpose.

Together with other management accountants, the CFO and the finance organization can act as designer and enabler of an integrated process of thinking, measuring, and reporting that facilitates conversations and fosters the development of innovative solutions that are characterized by multiple backgrounds and points of view. Here the role of the management accountant is essential to focus on the purpose of the business and on the multiple objectives to be achieved, considering the various stakeholders that engage within the value chain. The understanding of the financial and operating objectives, as well as the expected targets that are linked into the strategic plan of the organization, become the area where corporate purpose becomes visible.

Within this area, the CFO and the finance organization can engage in new conversations and enable purpose-driven organizations to identify the resources, activities, drivers, and stakeholders involved in the execution of a comprehensive business model. This is the area where the trade-offs, interests, and risks that characterize the value-creation process can be recognized. In this process, the focus can shift from business outcomes to how those outcomes are reflected in the overall positive impact of a business.

Ultimately, this will offer management accountants the opportunity to share the achievements of a purpose-driven organization with the board and key organization leaders, to maintain championship in terms of recognizing their contribution to the core business operations, and to ensure that data and analysis are used effectively for enabling responsible management, innovation, and decision making. In doing so, management accountants can play a leadership role in aligning corporate purpose with performance and long-term sustainable value creation for stakeholders.

Sidebar: Using the Blueprint Framework

Among the numerous initiatives, institutions, and foundations that recently have been challenging business organizations to be a force for good in society, A Blueprint for Better Business (Blueprint) developed a framework that captures and articulates five principles of a purpose-driven business. Blueprint is a U.K.-based charity that encourages companies to operate true to a purpose that serves society, respects the dignity of people, and generates a fair return for responsible investors.

The Blueprint Principles are based on the premise that businesses prosper by enriching the key relationships on which all successful businesses are founded. The energizing force that guides these relationships is purpose, which both provides a common direction for all relationships and encourages a dialogue between those relationships and the company rather than the company asserting positions and being a one-way transmitter of information.

Blueprint has a simple proposition: It is people and their relationships (internally and externally) that make business successful. A purpose that respects people and serves society enables and strengthens these relationships, and shareholder value flows from operating to that purpose. The Blueprint framework suggests that the key relationships connected by a purpose drive the search for long-term sustainable performance and sustain the generation of a fair return for investors. Within this context, the five principles for a purpose-driven business provide a route map to a new personal and organizational mind-set and aim to generate behavioral change in business by impacting the fundamental relationships that define each organization’s business model.

As you might expect, the principles are another accessible icon that represents outcomes that derive from a mind-set about business and, more fundamentally, about people and what motivates them to contribute to a common good such as a purposeful business. Without the mind-set, the principles can become another checklist. The deeper thinking is contained in what Blueprint calls the framework to guide decision making (see the Five Principles of a Purpose Driven Business, A Framework to Guide Decision Making at http://bit.ly/2B42g36).

December 2018