According to Gartner, by 2024 large organizations will triple their process automation capacity. According to a Business Wire report titled Global Robotic Process Automation Market Size, Share & Trends Analysis, the global market for process automation is expected to grow to $25.6 billion by 2027, increasing 40.6% per year.

The two most popular techniques to accelerate routine finance function processes are robotic process automation (RPA) and self-service data analytics. Organizations that strategically deploy both of these tools across their finance and accounting functions have an opportunity to better structure manual processes into more stable, accurate, repeatable, and readily auditable processes. Moreover, data-driven organizations that use process automation to improve efficiency can free up capacity to focus on more value-added analysis and innovation, thus providing them with a competitive advantage. Financial professionals, including management accountants, can benefit from embracing emergent capabilities to streamline their organization’s manual processing and realize control and efficiency benefits.

RPA utilizes software to automate repetitive, routine processes to increase operational efficiency. Self-service data analytics, by comparison, comprises a broad subset of analytics referring to any analytics solutions that are directly configurable by data workers. Commonly, such tools may integrate “extract, transform, and load” (ETL) capabilities and more advanced analytics and machine learning to assemble, scrub, and interrogate data; identify relationships; create visualizations; and automate spreadsheet-based processing.

While RPA has received considerable attention, organizations are increasingly deploying self-service data analytics due to its ease of configuration, packaged integration of multiple analytics technologies, and more advanced capabilities to implement process automation. According to a customer case report published by Alteryx on its website, Johnson & Johnson (J&J) integrated self-service data analytics into its compliance training program and achieved substantial results. As Adam Ehrenworth, J&J’s lead technology analyst, wrote, “We have eliminated the fragmented and manual process, which took days for the Health Care Compliance Office (HCCO) to produce a report. It is now a centralized, automated and instantly available reporting process.” As this testimonial implies, the new capabilities of analytics-assisted processing in the finance function have the broad-based attention of finance and accounting professionals—and executives alike—across many industries.

RAISING YOUR GAME

Accounting and financial professionals have relied on spreadsheets for decades, so it should come as no surprise that there’s a reluctance to adopt other analytics tools. As Pamela Schmidt, Kimberly Swanson Church, and Jennifer Riley wrote in “Breaking the Excel Routine” (Strategic Finance, March 2020), “a bias toward the status quo use of Excel has hampered widespread adoption of more advanced data analytics technology tools.” Furthermore, Molly Boyle points to a need for real change in “The Real Costs of Manual Accounting” (Strategic Finance, September 2020): “The way accounting has always been done isn’t sustainable—especially in the current environment. Manual processes tend to be chaotic and time-consuming, and the challenges are now even greater with so many companies—and their finance and accounting functions—working remotely during the pandemic.”

With businesses facing the impact and challenges of the COVID-19 pandemic—on operations as well as on employees—executives are changing their way of thinking. Some companies have turned to automation to deal with the increased demands on the finance function due to a geographically dispersed workforce, budget constraints, resource shortages, and other pressures facing management. The new environment has provided the impetus for executives to act on their long-standing automation plans and finally overcome the resistance to change.

A further driver for the adoption of cutting-edge analytics tools in the finance function is the wide availability of enterprise data, a concept known as data democratization. With vast quantities of enterprise data available directly to all within an organization, process owners are well-placed to adopt analytics tools to accelerate processing and deliver the best possible outcomes.

The most significant trend fueling the adoption of self-service data analytics has been the rise of easy-to-use analytics tools. Self-service data analytics platforms have become incredibly approachable, as they don’t require technology specialists or coding to develop and deploy. Instead, users can invoke “drag and drop” capabilities to configure analytics-assisted process automation, allowing “ordinary citizens” to directly develop solutions, without the involvement of the IT team.

The resulting direct and decentralized development model leads to expedited implementation time frames, measured in only hours or days. Armed with broad-based exposure to enterprise data—and equipped with a powerful suite of flexible, user-friendly, and efficient self-service data analytics tools—finance and accounting professionals are increasingly empowered and motivated to deploy analytics at the process level to generate value.

Driven by the converging trends of remote work, data democratization, and the wide availability of “no code” self-service data analytics tools, the evolution from manual spreadsheet-based processing to analytics-assisted automated processing will be the next critical waypoint as organizations progress along their digital transformation journey. As companies turn their focus to automating manual processes, they’re most likely to deploy RPA and self-service data analytics to improve efficiency and create a more reliable processing environment.

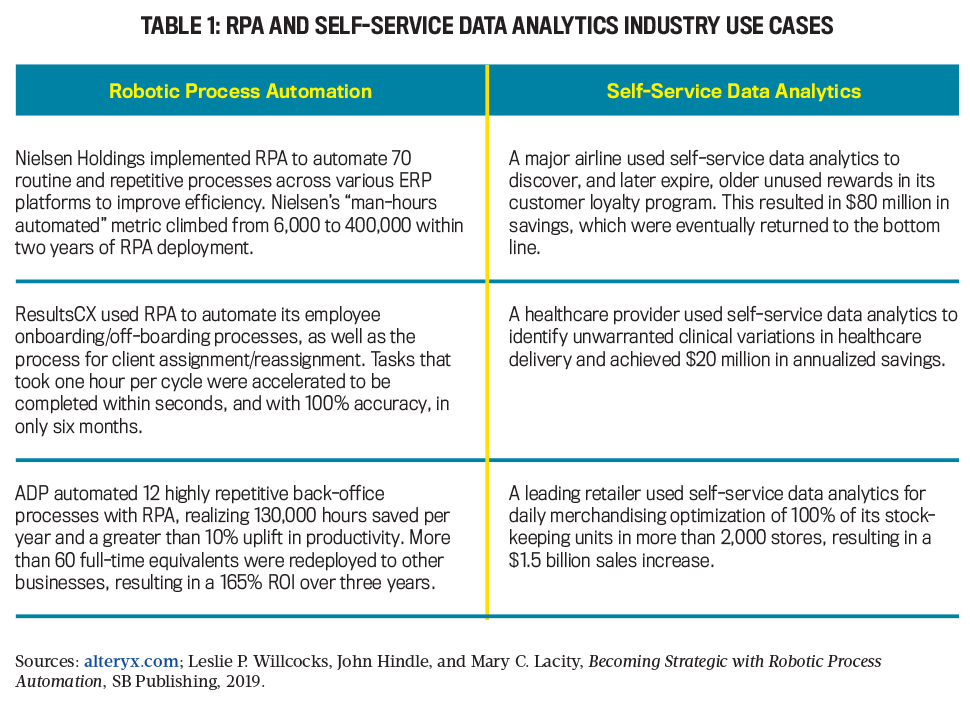

While RPA and self-service data analytics are both indispensable utilities for employing intelligent analytics and automation capabilities to streamline processing, they aren’t directly interchangeable and must not be conflated. They represent distinct tools, which, as Table 1 details, are appropriate for specific use cases that operators encounter in their daily processing functions.

PICKING THE BEST TOOL FOR THE JOB

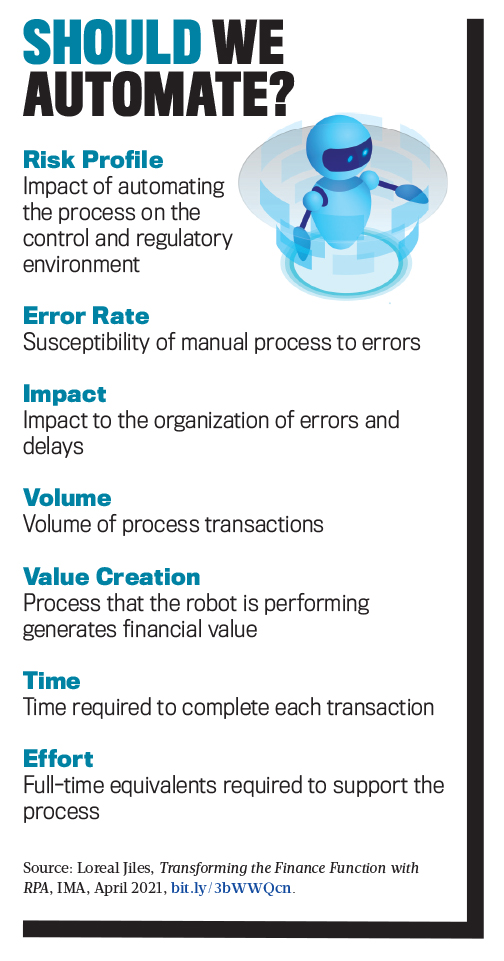

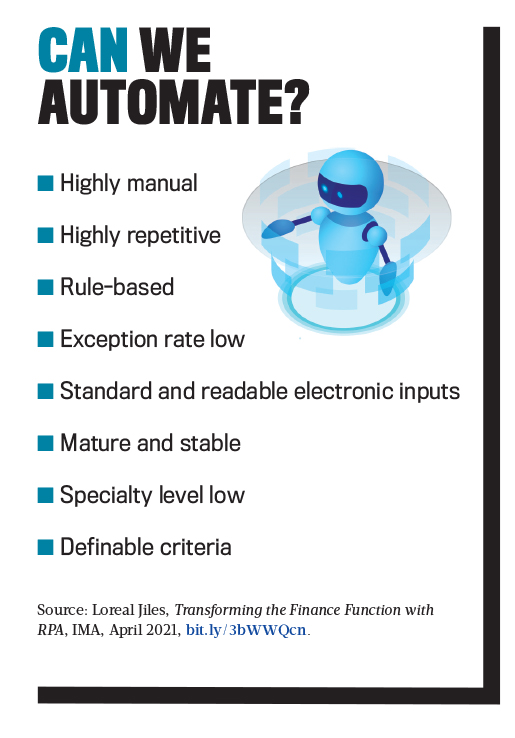

There are several key distinctions between RPA and self-service data analytics to keep in mind when evaluating which is the best one for a particular scenario. The primary determinants include the use cases represented by the projects, the project deployment timeline, recurring costs and return on investment (ROI) expectations, maintenance responsibilities, and training requirements. Finally, both solutions have unique governance requirements that must be considered in earnest to protect the value created.

While project ROIs for both RPA and self-service data analytics can be impressive, as evidenced by the case studies presented in Table 1, RPA projects present higher hurdle rates than do self-service data analytics projects because the recurring and significant bot maintenance costs in RPA projects must be surpassed by higher expected project benefits to realize equivalent ROI. Self-service data analytics deployments don’t require additional licensing fees for each marginal workflow developed, which may make them more desirable than RPA for smaller-scale automation projects due to per-bot maintenance cost considerations.

Click to enlarge.

RPA build monitoring and maintenance are ideally performed centrally through a purpose-built governance body, such as an automation center of excellence. (For more on RPA governance, see “Govern Your Bots!” by Loreal Jiles, Strategic Finance, January 2020) With self-service data analytics, users themselves deploy, monitor, and maintain automation configurations.

It’s essential that the individuals developing analytics capabilities—and using them—are adequately trained to do so. Meeting the training requirement is accomplished differently for RPA and self-service data analytics, respectively. RPA configurations are most often developed and maintained centrally by RPA developers within IT. Such specialists require significant RPA training and experience. Process owners require only minimal training to operate the bot, but as they design, build, and implement self-service solutions largely without IT involvement, they must not only have a detailed understanding of the longhand process being automated, but they also must ensure that solutions are fit for purpose, adequately controlled, and in line with organizational strategy. In both cases, the controlled introduction of RPA and self-service data analytics requires staff to be familiar with the analytics capabilities in use, the underlying business process flows, and how to deploy the tools in accordance with organization-wide development and control standards.

While both RPA and self-service data analytics require additional controls to mitigate the risks associated with their introduction, self-service data analytics requires an entirely new governance apparatus. As RPA solutions are likely to interact directly with systems and are typically developed and operated with the significant involvement of core IT, the legacy IT governance apparatus remains relevant. Self-service data analytics solutions are developed directly by process owners and operate outside of core systems, effectively sidestepping mature governance structures.

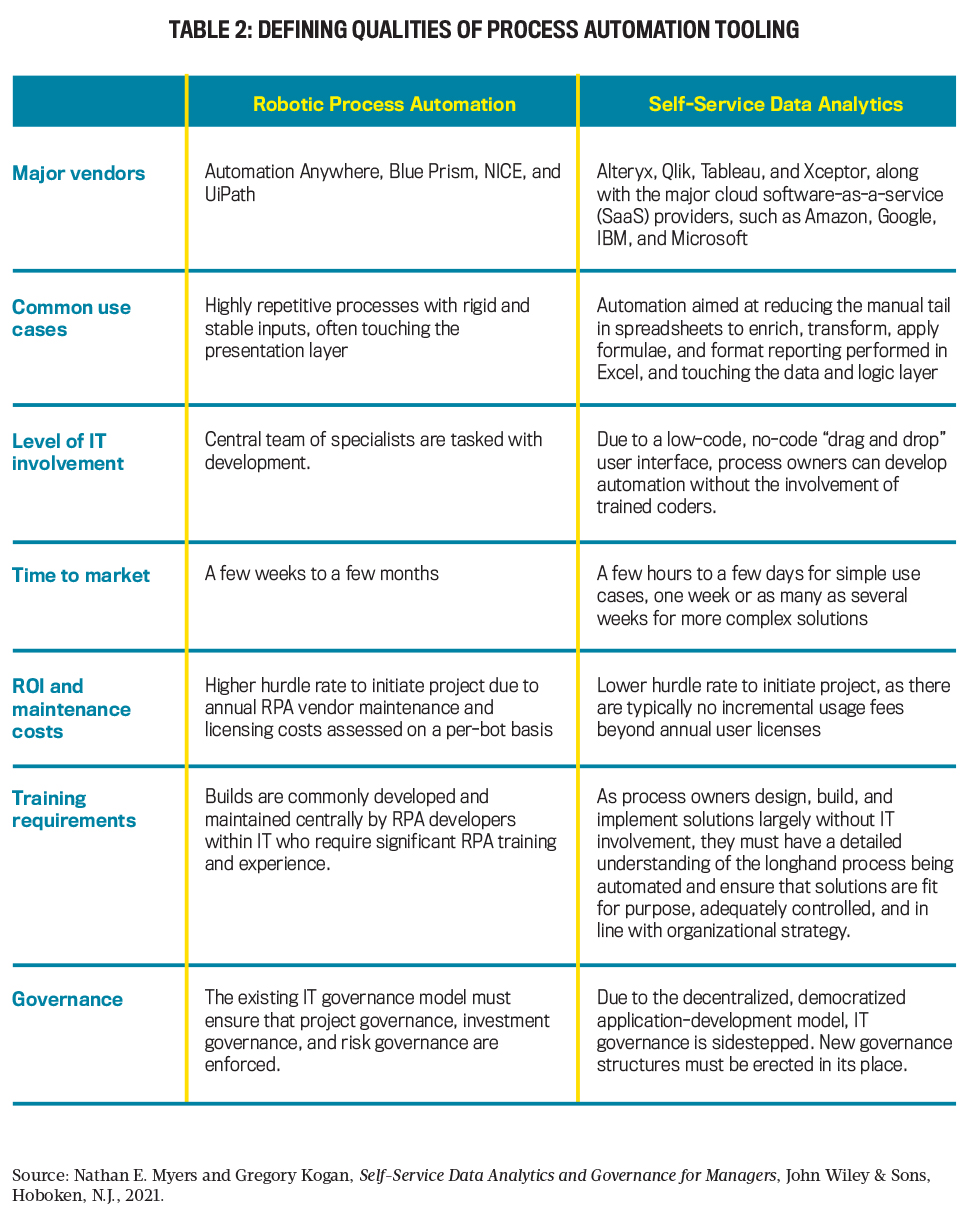

Accordingly, a comprehensive fit-for-purpose governance model must be forged to address project governance, investment governance, and risk governance in order to protect the value of the analytics program during the move to a decentralized application-development model where “ordinary citizens” are turning out applications at a feverish pace. Table 2 details the key differences between RPA and self-service data analytics.

Click to enlarge.

SPREADSHEET PROCESS AUTOMATION

It sounds simple enough: Companies can use self-service data analytics to automate all of their manual and recurring spreadsheet-driven finance and accounting processes. But how?

Instead of performing processes such as manual reconciliations, process owners can themselves configure automated workflows to invoke as needed, in lieu of the manual processing steps performed in spreadsheets. Processes can be broken down into a sequence of individual steps, and then structured thoughtfully into process flows with a logical order. Each analytics-assisted automation step becomes one link in a chain of steps that were previously performed manually, resulting in a more efficient automated process.

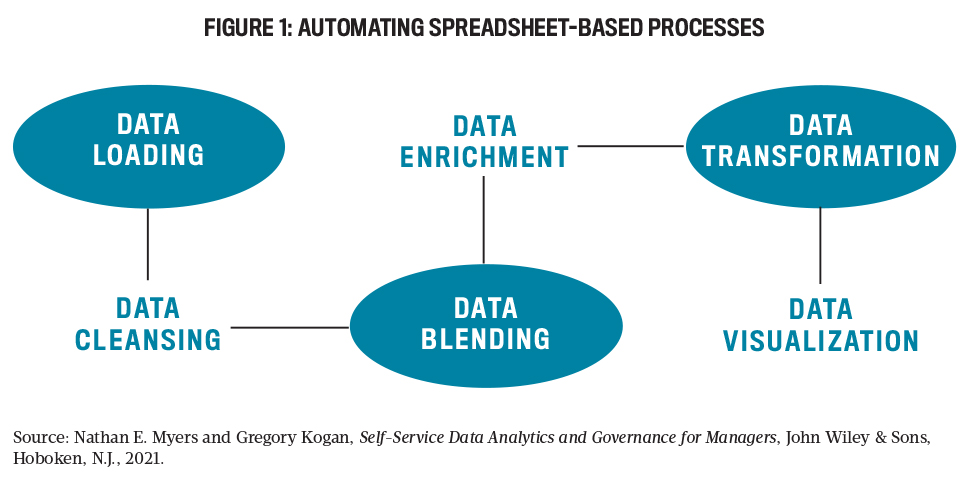

Automation not only improves efficiency and hastens processing time but also improves process control and stability. Self-service data analytics eliminates process variability because once the workflow is configured, the precise processing steps will be carried out and in the same order, without exception. Those who perform manual spreadsheet processes are the first to acknowledge that structured and repeatable tool-assisted workflows result in better outcomes than error-prone manual spreadsheet work, where hard-to-detect human errors are frequently introduced with varying and unpredictable consequences. As depicted in Figure 1, the use of self-service data analytics can markedly improve the operational efficiency of finance and accounting processing by structuring legacy spreadsheet tasks in workflows, without incurring additional costs.

ADOPTING THE NEW TECHNOLOGY

As companies continue to deploy automation and analytics programs to speed up their routine processes and create efficiencies, the biggest key to success is starting small and scoring quick wins. By optimally selecting and deploying analytics capabilities from the many tools available, you’ll secure senior management’s sponsorship for the analytics program while instituting a robust fit-for-purpose governance model to protect the value of the program at scale. With this as a framework, financial managers can drive digital transformation in their business units by focusing on the following four key strategies:

Become familiar with the technology. By better understanding the differences between RPA and self-service data analytics, financial managers can better evaluate problem statements and choose the best technology when matching use cases with available automation tooling.

Earlier, we outlined the key differences between RPA and self-service data analytics. By deploying RPA to automate work within enterprise resource planning (ERP) systems and deploying self-service data analytics around more customized spreadsheet processes, managers can use both technologies optimally to maximize their ROI for analytics projects.

Start small and “protect the baby.” If you’re a manager who wants to overcome resistance to analytics adoption, you should tread carefully and start small. Survey the processing plant for stable, routine manual processes that are performed widely across the organization and capture them in an opportunity inventory log. Assess the time spent performing each process manually, as well as the current failure rates, to document defensible benefits for each opportunity. Then estimate the costs to structure the manual work into a stable, repeatable, and automated flow. Remember that RPA often represents significant incremental bot maintenance costs, while self-service tools most often come only at the cost of individual licenses.

Once the benefits and the costs of automation are clear, it will become obvious which projects warrant prioritization. Of these, choose those that are most likely to be completed successfully. It will be important to paint the board with success to demonstrate the measurable benefits to sponsors and management, as a failure during the early stages can set the program back years.

Choose a program sponsor. The selection of an appropriate program sponsor is fundamental to a successful digital transformation. The key role of the program sponsor is to ensure that adequate funding is made available to successfully scale the program at a velocity that’s consistent with your organization’s stated goals and milestones.

A perfect candidate for program sponsor would be a senior employee in the processing plant—someone who would stand to gain from the success of data analytics, but also stand to lose, in the event of process instability. In this way, the sponsor has “skin in the game” and is most likely to promote significant opportunities to digitally advance the organization.

Be mindful of analytics governance. Sponsorship is but one pillar of governance. Governance must be stood up early in the digital transformation journey to maintain control and to protect the value created by analytics at scale. While RPA is often subject to legacy IT governance structures, self-service data analytics by definition is available to individual process owners, without the involvement of IT. Accordingly, absent specific action, there’s little to ensure that analytics is being introduced thoughtfully and consistently.

Governance is imperative to ensure that efforts have the right stakeholder support, that solutions satisfy requirements and are tested to a high standard, and that an adequate audit trail is maintained to enable process assurance capabilities. Importantly, governance helps to ensure that company resources and investment dollars flow logically to the best opportunities. Managers should consider governance as a necessary precursor to opening the door for the widespread adoption of analytics to avoid the painful exercise of retrofitting governance after the floodgates have opened.

A NEW DIGITAL DAY DAWNS

So, there you have it. While the finance and accounting functions have been moving toward digital transformation over the last decade, there’s still significant resistance to change due to the traditional reliance on spreadsheets for processing financial data. The recent trends of remote work, data democratization, and the widespread availability of self-service data analytics tools have provided the motivation to overcome this resistance and have enabled the exponentially accelerated pace of digital transformation. Business professionals who spend their days assembling and enriching information from disparate sources in spreadsheets; performing routine formulaic processing steps, comparisons, and aggregations; doing data entry; and executing system commands now have data analytics tools at their disposal to rapidly automate the least value-added portions of their roles and limit the introduction of manual errors.

Perhaps most importantly, management accountants and other financial professionals can reclaim time to focus on higher-order data analysis, the implementation of improved controls, or other emerging business priorities. Taken together, these benefits represent a quantum leap forward for organizations intent on truly harnessing data capabilities and optimally deploying their human capital.

December 2021