Research by Rosemary R. Fullerton, Frances A. Kennedy, and Sally K. Widener has shown Lean manufacturing and Lean accounting need to go hand in hand in order to ensure that a company will optimize waste reduction, productivity, and financial control (bit.ly/38764yY). Ultimately, this pays off as better service to customers.

Lean production can benefit from three aspects of a Lean management accounting environment. First, Lean management accounting practices (MAPs) can contribute to a Lean environment if they’re simplified and more strategic than traditional accounting practices. Second, value-stream costing contributes to a Lean environment because it’s timely and is better understood by users. Third, visual management methods contribute to Lean by making performance measures transparent and readily available to those who need it when they need it.

Being able to see or visualize the performance measures allows for immediate adjustments, allowing the benefits of Lean MAPs to flow more quickly through the organization and positively impacting the company’s operational performance. Without visualization of the information, the benefits from Lean MAPs and value-stream costing could be lost.

These three aspects of a Lean accounting environment create the foundation for achieving an overall Lean mind-set and strategy, which leads to more appropriate and timely decision making. Fullerton, et al., show that companies can boost their returns from the implementation of Lean manufacturing by 26% if they implement these three Lean accounting practices. That, in turn, significantly increases their financial performance.

For example, assume that your competitors implement both Lean accounting and Lean manufacturing practices and find that their operational performance increases by $1,260. If your company only implements Lean manufacturing practices, your operational performance may only increase by $1,000. You’ll leave $260 (26%) on the table and be at a disadvantage relative to your competitors. You might respond by saying that your competitor had to spend money implementing Lean practices, and that would be true. But experience and research show that the resulting operational improvements from Lean far outweigh the costs.

Because accounting is an essential part of any business, managers shouldn’t make business decisions without considering the impact of accounting information. Yet if Lean operations managers are only given information based on traditional accounting and reporting methods, they’ll fail to maximize operational and financial benefits from a Lean strategy. Properly aligning Lean manufacturing operations and Lean MAPs leads to improved operational performance, greater customer value, and increased financial performance.

Given that traditional management accounting focuses so much on managing and reducing product cost, it doesn’t provide the more relevant information to operations managers to help them manage capacity and inventory. Instead of focusing on reducing product costs, Lean management accounting makes capacity visible and motivates inventory reduction with an overall emphasis on continuous improvement. So, what is it about these Lean accounting practices that has this effect?

SIMPLIFIED AND STRATEGIC ACCOUNTING

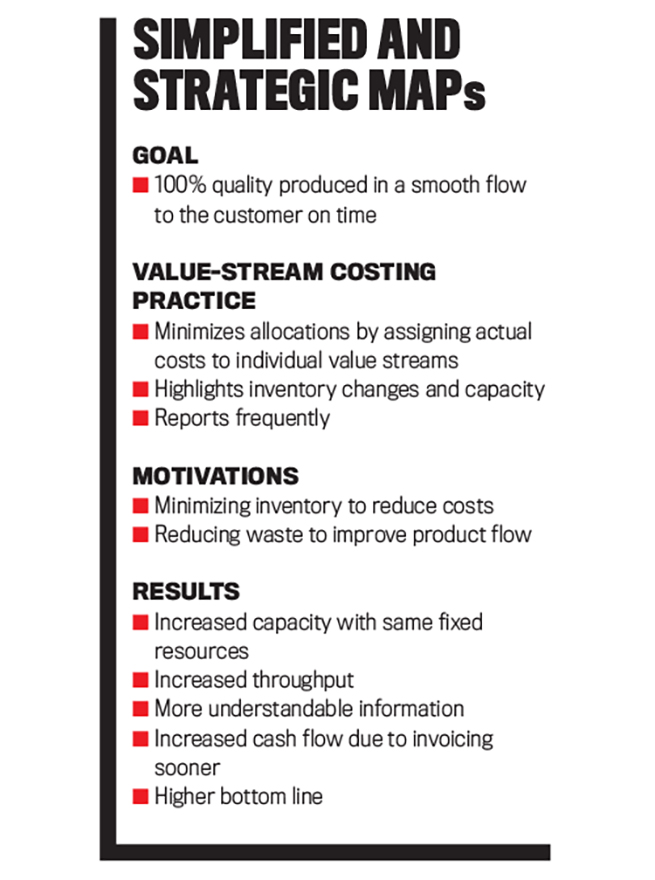

Lean manufacturing operations eliminate waste and inefficiencies in the production process. Similarly, we should expect that Lean accounting practices will reduce waste and inefficiencies in the accounting process. While Lean accounting eliminates unnecessary transactions like variance transactions and many related to inventory, more importantly, it focuses on collecting and reporting information that’s relevant to decisions made by the operations manager. By strategically aligning accounting practices with manufacturing objectives, the decision maker can better connect the dots between operating decisions and outcomes. Put another way, Lean MAPs link changes in operations to the financial impact of those changes. This alignment helps users to manage strategy (see “Simplified and Strategic MAPs”).

One of the ways that accounting practices can align more closely with manufacturing objectives is through the timing of information. In Lean manufacturing, decisions are made frequently in response to demand and changes in the process. Simplified accounting processes can deliver necessary information more frequently to support those decisions. Traditional accounting processes work on a monthly basis. Data is collected throughout the month and then summarized into statements that are intended to “tell the story” of that month’s production. By the time the statements are in the hands of supervisors the week after month-end closing, time has already been lost. Not only is it possible that the same problems are still occurring, but the supervisors and managers have to remember the decisions they made weeks ago that drove those results.

Imagine if information wasn’t provided monthly, but weekly. Supervisors could adjust their production processes more frequently with better information, and they could much more easily tie last week’s decisions to the results. Instead of 12 opportunities a year to learn and adjust, there are now 52. The learning cycle has just been dramatically improved. This shortened time frame also allows for rapid experimentation with much lower risk.

Accounting results can be more timely, as already mentioned, but they also can be more streamlined and understandable. Instead of complex variance calculations, Lean MAPs just include the actual costs. There are no complex calculations, and there is no delay to do those calculations. Simplified and strategic MAPs help ensure that Lean accounting practices are aligned with the operational goals and objectives of Lean manufacturing to support improved operations, greater customer value, and increased financial returns. Companies that recognize this necessity as part of their overall strategic plan are more likely to appreciate and incorporate value-stream costing as part of their decision making.

VALUE-STREAM COSTING

In order to have successful simplified and strategic MAPs, it’s critical to convert to value-stream costing. It’s possible to employ Lean practices within an accounting department, streamlining the processes, eliminating waste, and delivering traditional reports much more quickly and accurately. But information provided in a traditional statement is no easier to understand nor is it relevant to Lean production. Lean production includes recognizing value streams and managing those processes to reduce waste.

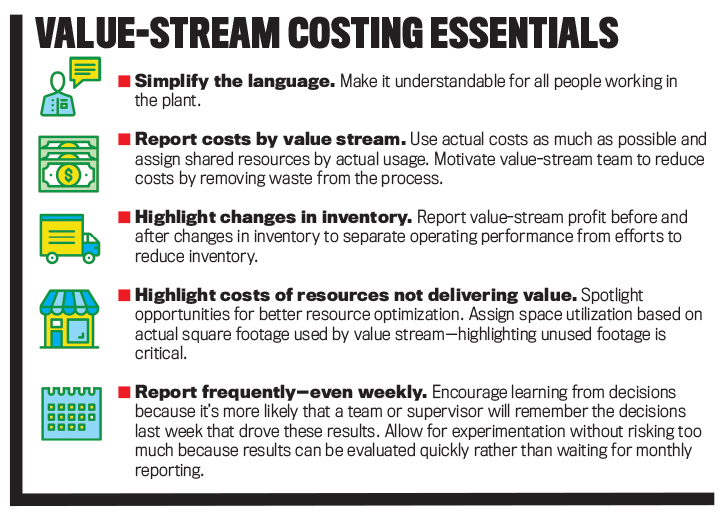

A traditional accounting reporting system organizes and reports company information by departments while value-stream costing organizes information by value stream. A value stream is a set of steps necessary to provide value to a customer (see “Value-Stream Costing Essentials”).

Click to enlarge.

Value-stream costing drives financial information based on the needs of the users, who are typically the operations manager and the value-stream team in a manufacturing environment. As such, it identifies and assigns costs based on the value created in each step from initiation to delivery. By focusing on value creation, this Lean accounting practice deals with actual costs and assigns the costs to value streams, often eliminating the need for cost allocations and creating financial information that is understandable and useful to employees.

With traditional accounting systems, accountants tend to spend a lot of time collecting data and calculating product costs to create variance reports that the user often doesn’t understand. Have you tried to explain an absorption variance or a variable overhead efficiency variance to a production line worker or supervisor? Because they often have different areas of expertise and may not understand traditional accounting, operational decision makers tend to ignore that information and make decisions independent of the accounting reporting. Thus, traditional management accounting does little to promote operational decision making in a Lean manufacturing environment.

Moreover, if they do use the information, it can actually undermine Lean objectives. Quantity variance analysis is one example. The reason traditional environments provide quantity variances is to show the impact of not producing to forecast. No production manager wants to show negative variances if it can be avoided. Of course, the easiest way to manage this variance is to produce more—and store it if you don’t have demand. That may correct the variance and result in a lower cost per unit, but now there are more handling, storage, liability, and potential obsolescence costs that will show up elsewhere on the financial statements. That isn’t Lean thinking.

Essentially, value-stream costing shifts the user’s focus from a single unit as a cost object to the costs consumed along the entire value stream. This lens not only promotes identifying and eliminating waste to reduce the overall cost of the value stream, but it also results in increased capacity, enabling more production with the same set of fixed resources. Ultimately, this means a lower cost per unit.

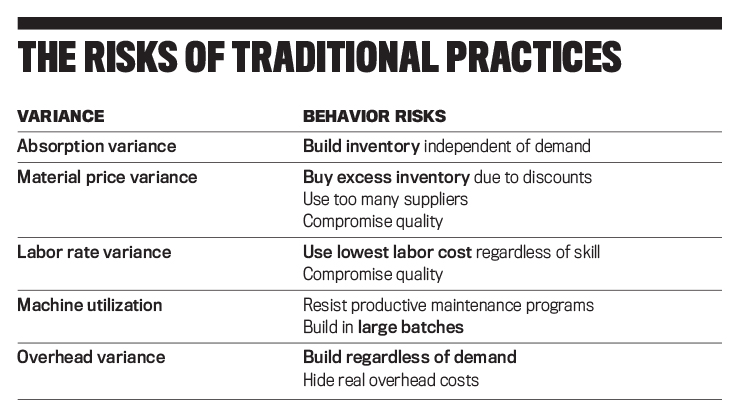

Value-stream costing allows Lean companies to collect and present actual direct cost data by value stream. No longer are there complex and hard-to-understand variances to explain. Value-stream costing involves more frequent tracking of costs (usually weekly), which allows for greater cost control and management (see “The Risks of Traditional Practices” for an overview of the risks in traditional measures).

Click to enlarge.

The information collected is streamlined, void of unusable data, and timely so that the operations manager can understand the information and use it in the current period to make better decisions. A value-stream statement highlights inventory change below the line (i.e., profit or loss of the value stream), so value-stream managers aren’t motivated to build inventories. It also highlights unused capacity so managers can use that capacity creatively to drive other revenue streams.

Value-stream costing results in easy-to-read and understandable cost accounting reports. Simple, understandable data assists operations personnel in making production and capacity decisions, such as whether to expand or outsource a product. Support of these types of decisions makes the Lean accounting data relevant to the decision makers.

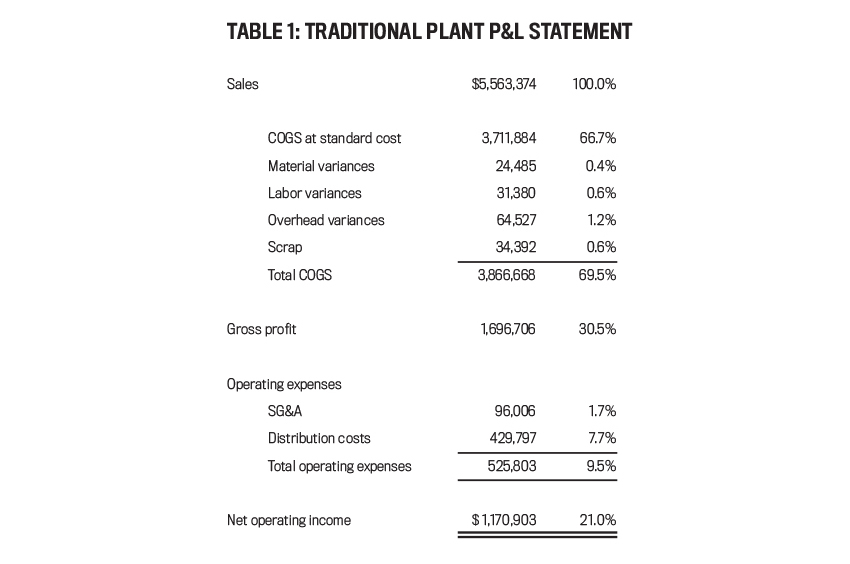

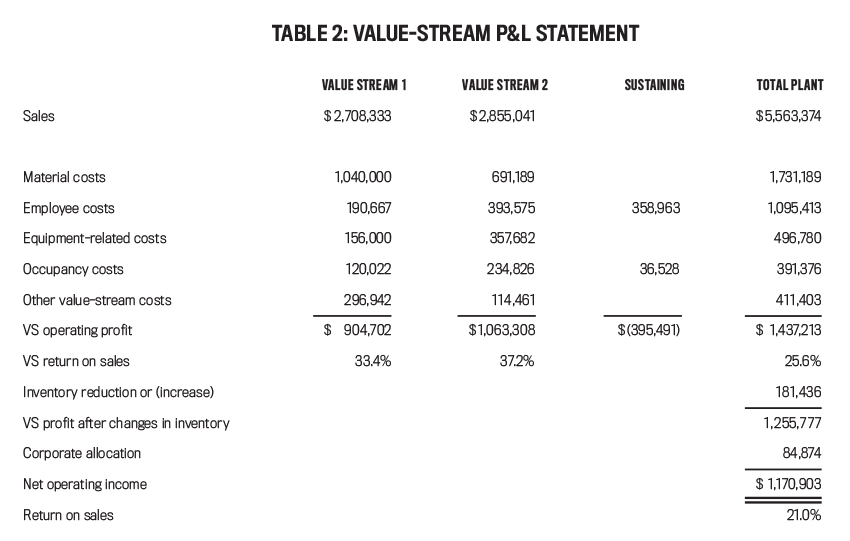

Operations managers can use value-stream costing reports to quickly analyze performance and make needed adjustments in the production process. Although variances aren’t used in Lean manufacturing, operations managers are provided visual information showing effectiveness and efficiency of Lean processes. Table 1 shows the traditional, aggregated monthly financial reporting, and Table 2 shows the disaggregated, more useful value-stream costing income statement.

Click to enlarge.

Click to enlarge.

Traditional statements are aggregated in two ways that value-stream costing reports aren’t: First, there is one column, plant total, information, etc. Value-stream costing is broken down into the value streams and the organization-sustaining costs. Second, traditional statements lump all production costs into cost of goods sold, while value-stream costing breaks them down into line items that the plant managers can control, like material costs and employee costs. Changes in inventory are also broken out. This information is more timely and easier to understand than the traditional standard-costing-variance reporting.

VISUAL PERFORMANCE MEASURES

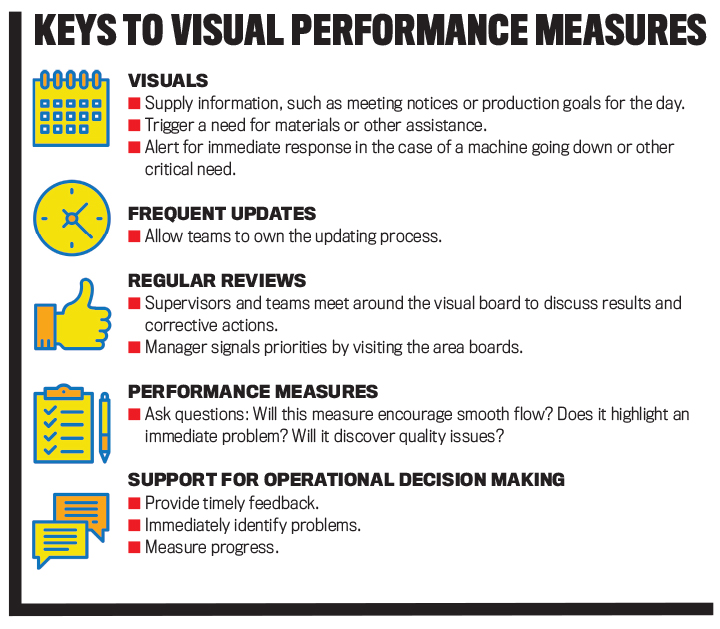

Once the company aligns the Lean management accounting practices to properly support Lean manufacturing strategy, visual performance measures can help communicate those results in real time. Fullerton, et al., have shown that visual performance measures are effective at communicating relevant, real-time Lean accounting information to manufacturing personnel. To be effective, they must be simple and easy to read and contain relevant internal financial information for operations personnel (see “Keys to Visual Performance Measures”).

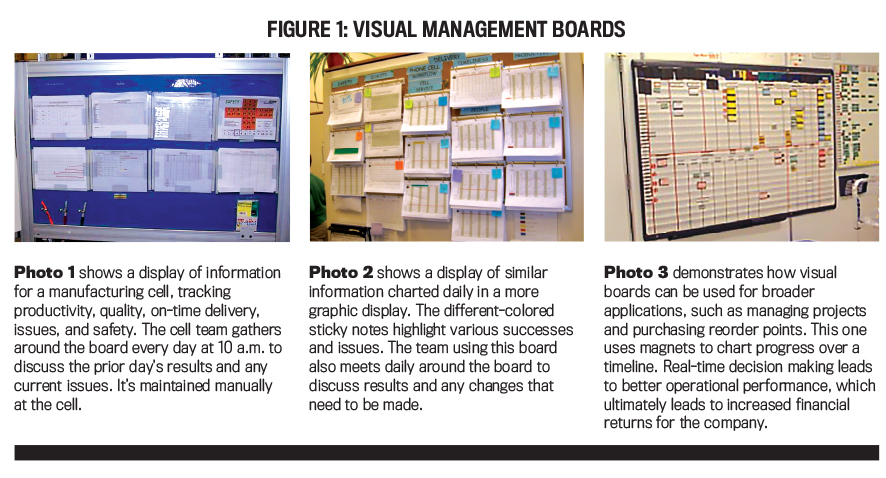

Visual performance measures provide operations personnel real-time feedback of performance information that they can use in a timely way to make necessary adjustments and decisions. Examples of visual management displays include box scores and performance measurements (such as production levels and quality) that are displayed on visual boards on the operations floor so that operations personnel can see the information. The displays can be as simple or as automated as needed. (See Figure 1 for some examples.)

Click to enlarge.

COMPLETING THE LEAN MIND-SET

Fullerton, et al., found that the use of Lean MAPs is influenced by the extent Lean manufacturing practices are used, suggesting that companies are recognizing the need to align their accounting practices to support the goals of their Lean operations. A Lean mind-set should now include financial performance. Companies can achieve a Lean environment—and the resulting improved financial and operational performance—by pursuing a holistic Lean strategy that includes not only Lean operations but also Lean MAPs.

Using traditional management accounting practices can undermine a Lean strategy whereas Lean MAPs are an essential component of an overall Lean strategy. Accounting personnel can play a crucial supporting role in following a Lean strategy by using innovative approaches like simplified and strategically aligned MAPs, value-stream costing, and visual performance measures. These three aspects of Lean accounting contribute to a complete business strategy, paving the way for companies to optimize operational and financial performance improvements when going Lean. Implementing Lean manufacturing without considering the impact of accounting practices unnecessarily leaves savings on the table.

January 2020