The current noise and flurry of activity around FP&A have all the trappings of the feeding frenzies that accompanied the introduction of tools such as activity-based costing (ABC), the Theory of Constraints (TOC), balanced scorecards, and strategy maps. Each of these tools has had an important and significant impact on some organizations. Yet the successes weren’t the result of jumping on a bandwagon, but rather thinking deeply about the nature of the business, gaining deep internal expertise, understanding the essence of the tool, and applying it effectively to solve a business problem in the context of a business’s culture.

FP&A is clearly on a growth path, one of increasing importance. Advances in digital technology, Big Data, data analytics, and AI increase the potential for management accountants to use powerful tools to vastly improve and expand the FP&A function. Yet like so many advances in management accounting, the tools and methods employed tend to get in front of the thinking about foundational knowledge and the strategic direction the profession needs to take for long-term success with FP&A.

The same digital technologies that will enable better FP&A will also lessen the need for accountants in many traditional areas, including transaction processing, financial reporting, auditing (internal and external), tax work, and treasury management. FP&A is a potential growth area for the profession, but the direction and value of that growth and the possible new tasks and functions need to be defined. Accountants and the accounting profession need to think deeply about what hasn’t been done well in this area and fill those gaps with valuable information useful for decision support. This requires creating a robust definition of FP&A that will support the entire organization, looking well beyond finance and accounting’s traditional scope and embracing all the value creation and performance goals throughout an organization.

A NEW PERSPECTIVE

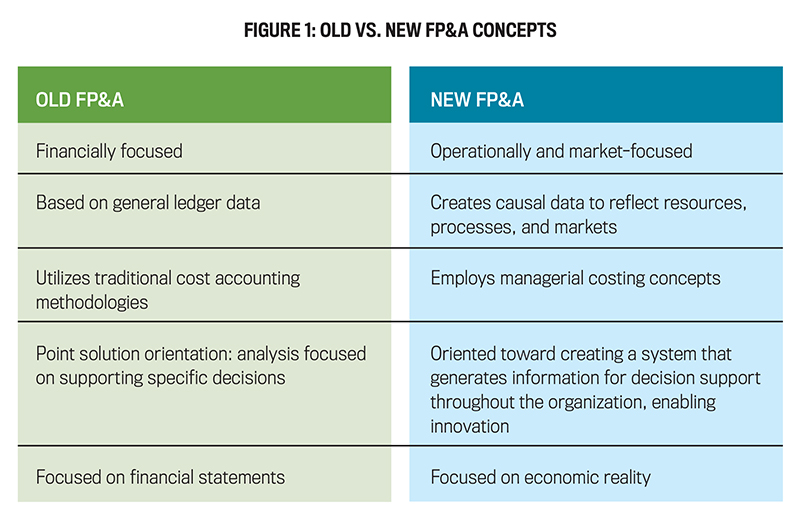

We propose profitability analytics, a new perspective on FP&A (see Figure 1) that recognizes the importance of traditional accounting tasks such as financial reporting, record keeping, and cash management and also focuses most of the attention on the developing areas of nonfinancial and financial data analytics and modeling that causally support building robust forward-looking scenarios and analyses.

The term “profitability analytics” captures the goal of most commercial and even not-for-profit organizations—creating long-term sustainable value. (See “Government and Not-for-Profit Organizations” below)

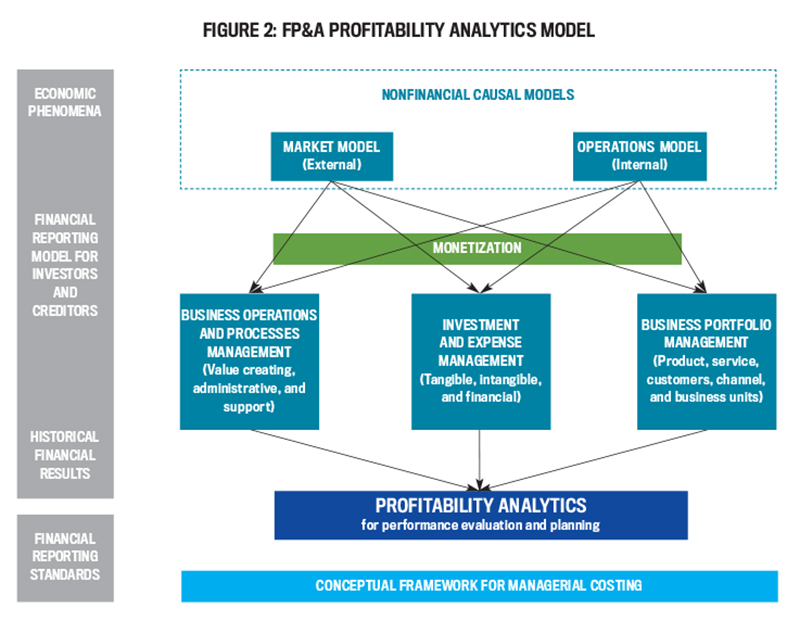

To achieve this, an organization needs to clearly understand how it can generate revenue, invest and spend for the long term, and configure and manage operations efficiently. Organizations must be capable of developing robust models of their markets, customers, and external business environments and building robust models of their internal resources, operations, and processes that create value. See Figure 2 for a model of this approach.

Let’s examine the details of this model. First, you’ll notice on the left-hand side there are two “blocks” representing the traditional, regulated financial reporting domain. This presentation differentiates this domain from the FP&A profitability analytics domain. External financial reporting is highly structured and is required to comply with financial reporting standards that are focused on providing a well-defined and standardized picture of historical performance that investors and creditors can use to assess an organization’s performance. The profitability analytics model pulls in a variety of data and relies on many models of the external business environment and internally controlled operations and processes. Examining current performance and the immediate past for lessons learned is still important, but forecasting scenarios, risks and opportunities, and responses needs to be the real focus of FP&A today.

MODELING REVENUE AND COST

The top block of the profitability analytics diagram represents the reality of what drives profitability analytics—nonfinancial causal models. Two general categories of models are critical to any business. The first category is a market model that encompasses economic conditions, customer activity, competitive environment, and any other factors that will influence the generation of revenue and the general economic environment.

The second category is a model of the business’s internal or internally controlled operations that create value for its markets. This model is focused on effectiveness, efficiency, and optimization. Both of these models are primarily nonfinancial and need to reflect cause-and-effect relationships of reality and the assumptions of forward-looking scenarios.

MONETIZATION

The next block down depicts the special competency area of the accountant: monetizing nonfinancial models in a manner that enables effective decision making. Monetization isn’t a trivial exercise. Applying money to a nonfinancial model can create distortions. Resources aren’t always divisible into small units, but money always is. The art and skill of monetization are to design, collect, and apply monetary information in a way that reflects the nonfinancial components of a model and its causal relationships without distortion.

One of the issues with traditional financial accounting information is that real business events and operations are obscured by a fog of financial accounting and reporting standards. By building models that represent causal nonfinancial business data and scenarios first and then having the monetary data collection built to reflect those models, organizations can avoid the need to clear the fog created by financial reporting standards, reducing the amount of analysis required to understand current performance and lessons learned.

DECISION DOMAINS

Continuing on, the three blocks in the center of the FP&A profitability analytics diagram represent broad domains of decisions that must be made in business. The boundaries between these domains aren’t rigid, and many decisions cross the boundaries defined in this diagram.

The decisions FP&A generally focuses on in all of these domains are twofold: (1) examining current performance and the immediate past for lessons learned and changes to replicate positive performance or change negative performance and (2) making projections and planning for the future with forward-looking scenarios, analyzing risks and opportunities, and mapping possible responses.

A critical issue for FP&A in all these domains is that decision-support information must be highly usable for decision making at all levels of the organization. What does this mean? To be usable, financial information must possess three key qualities: transparency, defensibility, and timeliness.

The critical requirement is that financial information reflect the causal relationships seen and experienced by decision makers. Managers will second-guess opaque cost information, and the resulting discussions or arguments about the financial information undercut efforts to improve decision making, profitability, and processes within organizations. Defensibility is achieved when managers and employees outside the finance department can readily apply financial information when investigating business and operational problems or evaluating solutions without worrying that the finance department will find fault with the financial information used in the analysis.

In the profitability analytics model, transparency of information is achieved through the use of the causal nonfinancial models that reflect the business events, resources, and processes that decision makers manage and observe. Careful monetization of the models creates transparency of the information; the financial figures directly relate to the events, resources, and processes.

Timeliness means financial information that is recent and consistently available. Depending on the situation, this may be seconds, minutes, hours, or days, reflecting the requirements of business and operational scenarios. Consistency requires the data, models, and systems to be in place to generate the information for managers and employees. A special study—no matter how effectively done, no matter how quickly completed, no matter how well-guided with policy and procedures—is never as useful as having information available for day-in, day-out measurement and evaluation. Only through continuous observation and evaluation by both financial and nonfinancial personnel can financial information be understood to a degree that builds confidence throughout the organization.

BUSINESS OPERATIONS AND PROCESS MANAGEMENT

The business operations and process management domain encompasses the range of resources and processes that enable a business to operate and create value. It extends outside the organization to the organization’s supply chain and beyond production or service operations to include activities such as sales, public affairs, and lobbying/political activity.

This area has traditionally been the focus of budget, cost analytics, and manager and executive performance metrics. An Association of Chartered Certified Accountants (ACCA) and KPMG study of more than 900 financial professionals from around the world found that current practices in this area were severely lacking, even when judged by those who managed the functions. (See “Financial Professional Study” below.)

Digital technology, improved systems, and AI offer some avenues for improvement, but automating today’s practices really only improves efficiency. Achieving effectiveness requires new and innovative thinking. Thinking needs to move beyond established accounting and even FP&A practices, and instead move to thinking about the needs, interests, and problems of the managers and employees in an organization. Traditional accounting thinking focuses on control. FP&A should focus on facilitating innovation. The mind-set should be that everyone in the organization wants to create long-term sustainable value in everything they do. What information will help them? How can that information be most effectively communicated? How can FP&A help them create and use the information?

INVESTMENT AND EXPENSE MANAGEMENT

This domain encompasses investment in new assets—both tangible and intangible. No statistic causes one to question the value of today’s financial reporting standards more than the fact that balance sheet assets explain less than 20% of corporate value across capital markets. FP&A needs to have data and models far beyond what exists in most accounting systems today to effectively support the investment and spending decisions of their organizations.

Justifications for investments or spending on marketing and brand development, research and development, data collection, systems, human resource development, community and social development, and other non- or marginally capitalizable activities need to be developed based on a range of highly variable and dynamic business scenarios and assumptions. What matters isn’t the accuracy of the numbers, but the causal logic of the scenarios and the probability of occurrence. The challenge is clarifying the direction and then preparing for the range of responses that may occur as you move in that direction.

BUSINESS PORTFOLIO MANAGEMENT

This domain is primarily focused on revenue generation and acquiring markets or market share. It’s focused on understanding customers and potential customers as well as existing and potential new markets both now and well into the future.

While the customer portion of this domain has been the province of sales and marketing, digital technology is changing the way this game is played and increasing the opportunities and risks. The ability of the web to follow customer actions, interests, purchases, and even movements is a data gold mine if it can be collected, deciphered, and analyzed effectively.

Entering new markets not only requires the business acumen that accountants have traditionally provided, it also requires preparing a multiscenario analysis of how to enter the market and establish a customer base. Today the options to offer products and services to markets are much more diverse. FP&A needs to help define the business cases for multiple scenarios; identify the causal factors, risks, opportunities, potential rewards, and potential losses; define plans for a fallback and plans for a massive win; and define the key operational and financial indicators senior management can watch in real time to identify what hitting or missing the target means and the option set associated with each.

There are metrics that have been around a while but that haven’t often been used by accountants, including customer lifetime value, customer cost, distribution channel cost, and profitability. These metrics haven’t been well-supported by traditional accounting data, but, with new causal models, advanced technology, and more robust cost and revenue data, these metrics can move from the “interesting, but not very timely” or “too hard” category to real-time insights for customer-facing team members.

THE FOUNDATION

The accounting profession needs to support the growth of FP&A more aggressively. It’s work that will be done in organizations; the only question is whether it will be accountants who step up, acquire the skills, and demonstrate the mind-set and drive. Many traditional accounting skills are useful in the FP&A arena, but the focus needs to be on communication, leadership, and interpersonal skills; on causality rather than accounting standards and building models that represent operational and monetary reality; and on being able to innovate with digital technology skills and having a robust understanding of statistical approaches to representing uncertainty.

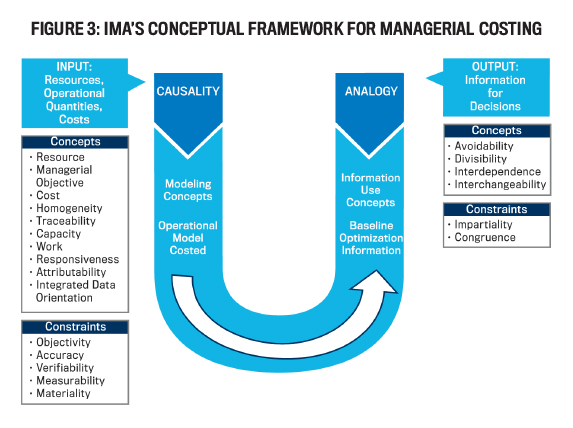

IMA has created the Conceptual Framework for Managerial Costing (bit.ly/2WTXqRK) to provide a pathway to support causal modeling (see Figure 3). Its focus is on modeling purely for internal decision making. The fundamental idea is that it’s necessary to first build an operational model of an organization’s resources and processes, then structure the collection of monetary data to support that reality. While it’s fundamentally designed for costing and most directly applicable to the first two domains discussed, it presents a very different perspective of how accounting skills and knowledge can be applied and provide insights into the entire FP&A domain.

FP&A: THE FUTURE

Technological advances and the use of leading-edge analytics create the potential for accountants to vastly improve and expand the FP&A function. Yet if we merely automate the processes of yesterday, we will fail to generate improvements in the FP&A process and perhaps jeopardize the future of our profession.

In order to stay relevant, management accountants must move beyond their traditional FP&A models based on external financial reporting requirements. The profitability analytics model described here provides a framework for doing so. By starting with the nonfinancial market and operational models of their organization and then monetizing those models, finance and accounting professionals will be able to produce transparent, defensible, and timely information. By doing so, management accountants can become true business partners with the rest of their organization.

The authors gratefully acknowledge the contributions of Gary Cokins, Doug Hicks, Kip Krumwiede, and Monte Swain to this article.

July 2019