With the financial markets in turmoil due to the COVID-19 pandemic, it’s even more important for corporations to be ready for the financial landscape that will exist in 2021. In fact, it’s likely that the current stress on the market caused by business shutdowns will test the smooth transition to a post-LIBOR landscape.

IBOR rates, although used among banks for short-term transactions, are ubiquitously used by corporations as a basis for credit and investment contract rates. LIBOR rates are established based on rates reported by banks. The use of LIBOR has a long history that can be traced back to 1969 when J.P. Morgan used the rate as a basis for an $80 million contract. The rate was in common use by the 1970s, and in the 1980s the British Banker’s Association formalized the practice.

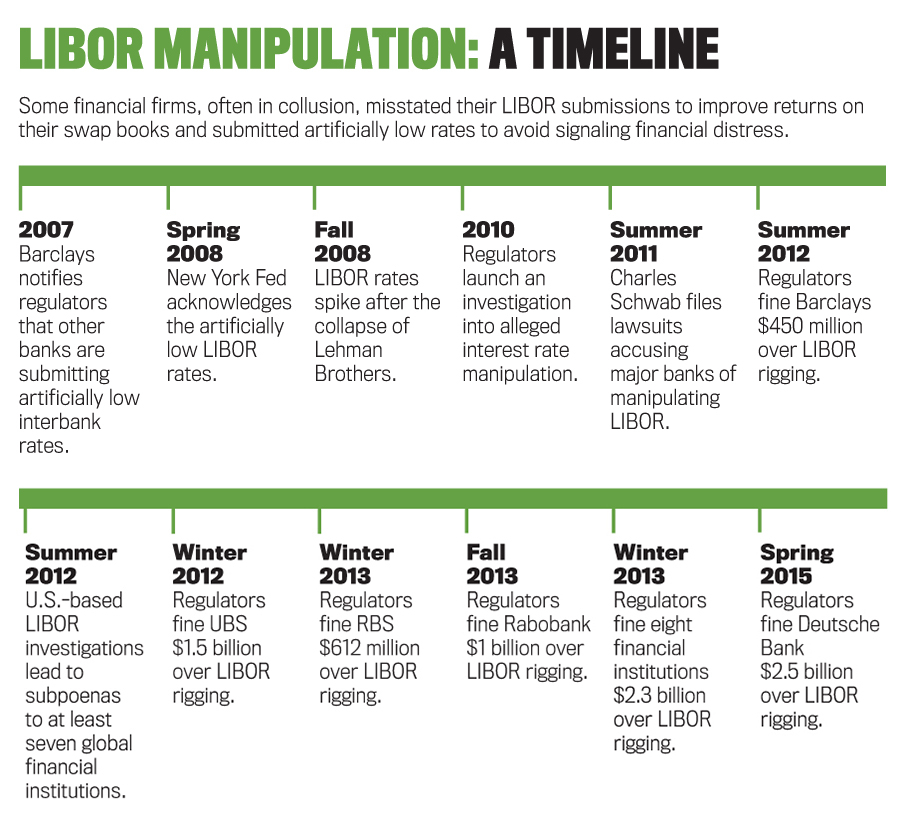

The beginning of the end of LIBOR as a reference rate came during the 2008 credit crisis when contributing bank personnel colluded when setting LIBOR rates. Unfortunately, not all banks precisely (or truthfully) reported accurate data. This resulted in LIBOR manipulation and a loss of market confidence in the LIBOR rates (see “Libor Manipulation: A Timeline”). Since that time, regulators have taken steps to phase out LIBOR and find a suitable replacement.

Click to enlarge.

As hundreds of trillions of dollars’ worth of existing contracts, derivatives, and other corporate and bank instruments reference LIBOR, companies must prepare now for any confusion resulting when the rate is no longer usable. Specifically, any existing contracts or instruments that are directly or indirectly based on LIBOR should be reevaluated, rewritten, or renegotiated. To assist with these contract changes, the Federal Reserve Board and the Federal Reserve Bank of New York (New York Fed) created the Alternative Reference Rates Committee (ARRC), which is a private group of market participants. The ARRC was created to support the transition from LIBOR to the newly established Secured Overnight Financing Rate (SOFR).

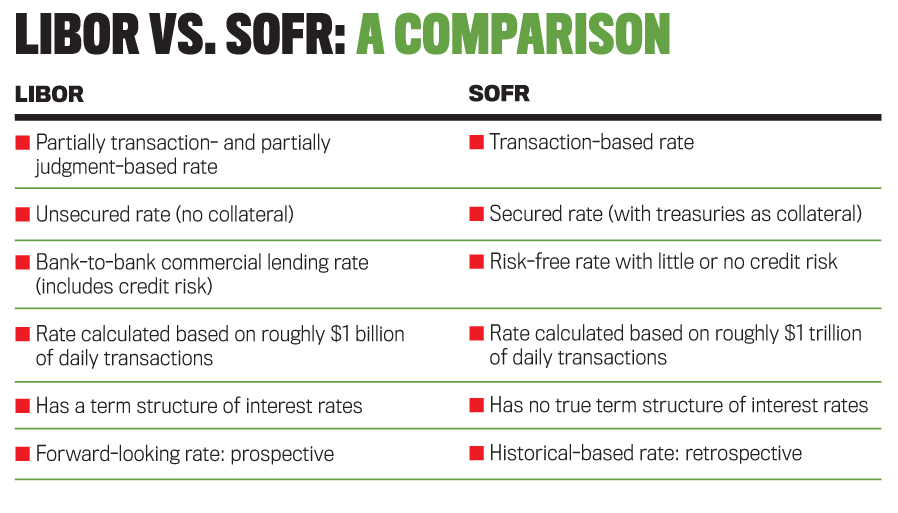

In 2017, ARRC recognized SOFR as a suitable replacement for LIBOR (see “LIBOR vs. SOFR: A Comparison”). At the same time, the Financial Accounting Standards Board (FASB) monitored the efforts being made toward reference rate reform. The New York Fed requested that SOFR be used as the reference rate for hedge accounting under Accounting Standards Update (ASU) No. 2017-12, Derivatives and Hedging (Topic 815): Targeted Improvements to Accounting for Hedging Activities, and began publishing SOFR daily in early 2018.

The FASB considered the request and in 2018 issued ASU No. 2018-16, Derivatives and Hedging (Topic 815): Inclusion of the Secured Overnight Financing Rate (SOFR) Overnight Index Swap (OIS) Rate as a Benchmark Interest Rate for Hedge Accounting Purposes. ASU No. 2018-16 allows the use of SOFR as a U.S. reference rate for hedge accounting pursuant to Topic 81 and requires companies adopting ASU No. 2017-12 to simultaneously adopt the ASU No. 2018-16 amendments.

The forced migration away from the IBORs potentially has significant financial reporting consequences for companies, especially with respect to asset and liability valuation, hedge accounting, and profit and loss recognition. In June 2018, the International Accounting Standards Board (IASB) added the “IBOR Reform and the Effects on Financial Reporting” project to its active research agenda. In October 2018, the FASB added a similar project to its agenda.

In September 2019, IASB issued Interest Rate Benchmark Reform, Amendments to IFRS 9, IAS 39 and IFRS 7, which amends three of the financial instruments standards. The amendments provide for temporary exceptions to the application of specific hedge accounting requirements when the hedging relationship is directly affected by a market-wide, benchmark interest rate reform. Under specific circumstances, if the benchmark interest rate for the hedged item or hedging instrument changes due to benchmark interest rate reform, hedging relationships are to be treated as unaltered for financial reporting purposes.

Most recently, in March 2020, the FASB issued ASU No. 2020-04, Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting. Its purpose was to respond to the concerns of market participants regarding their “ability to retain hedge accounting under Topic 815 for existing hedging relationships and asked the Board to consider potential relief to allow hedge accounting to continue in that circumstance” and also because “stakeholders indicated that reference rate reform was expected to create potential operational challenges in applying other areas of [U.S.] GAAP related to [51] modifications of financial instruments” (see ASU 2020-04).

Addressing these and other commenters’ concerns, the ASU contains exceptions and optional expedients for hedge accounting (and other financial instruments) that will be impacted by LIBOR’s sunset. In the ASU, the FASB also indicates that it has confidence that the smooth continuation of contracts that referenced LIBOR and the cost savings to statement preparers afforded by the provisions provided in ASU 2020-04 will outweigh any incremental costs incurred in complying with the revised rules. Although the New York Fed, ARRC, and the FASB have generally endorsed the use of SOFR as a primary replacement for LIBOR, the choice of SOFR met some resistance.

CRITICISMS OF SOFR

LIBOR has a subjective component that makes it susceptible to measurement errors (unintentional and otherwise). Specifically, the calculation of LIBOR begins with contributing banks answering the question: “At what rate could you borrow funds, were you to do so by asking for and then accepting interbank offers in a reasonable market size just prior to 11 a.m. London time?” After ranking the collected sample rates, trimming (to omit high and low value outliers), and averaging the data, the result is meant to represent a rate that banks would use to fund their operations in the very near (or immediate) future. Although subjective, LIBOR is intended to capture the banks’ expected cost of debt capital.

In the 2019 A User’s Guide to SOFR, the ARRC supports its choice of SOFR as follows:

- It is a rate produced by the Federal Reserve Bank of New York for the public good;

- It is derived from an active and well-defined market with sufficient depth to make it extraordinarily difficult to manipulate or influence;

- It is produced in a transparent, direct manner and is based on observable transactions, rather than being dependent on estimates, like LIBOR, or derived through models; and

- It is derived from a market that was able to weather the global financial crisis and that the ARRC credibly believes will remain active enough in order that it can reliably be produced in a wide range of market conditions.

But several criticisms of SOFR persist, starting with its calculation. The New York Fed notes “SOFR is calculated as a volume-weighted median of transaction-level tri-party repo data collected from the Bank of New York Mellon as well as GCF Repo transaction data and data on bilateral Treasury repo transactions cleared through FICC’s DVP service, which are obtained from DTCC Solutions LLC, an affiliate of the Depository Trust & Clearing Corporation. Each business day, the New York Fed publishes the SOFR on the New York Fed website at approximately 8:00 a.m. ET” (nyfed.org/3h8jAXy).

Thus, while LIBOR is “forward-looking,” SOFR is historical. Therefore, SOFR may not be reflective of the banks’ forthcoming cost of debt capital. According to critics, for SOFR (or any alternative reference rate) to be a reasonable LIBOR replacement, it should capture the banks’ expected cost of debt capital.

Critics also point out that SOFR, first published by the New York Fed on April 3, 2018, uses overnight repo rates of U.S. government treasuries, which can be volatile. But others point out that in spite of that volatility SOFR is usually averaged when referenced in contracts and that those averages are generally stable (see “Wave Goodbye to Libor. Welcome Its Successor, SOFR” in Bloomberg Opinion, December 2019).

In response to the overnight rate volatility criticism, on March 2, 2020, the New York Fed began reporting SOFR averages, which are compounded averages of the SOFR overnight rolling 30-, 90-, and 180-calendar day periods.

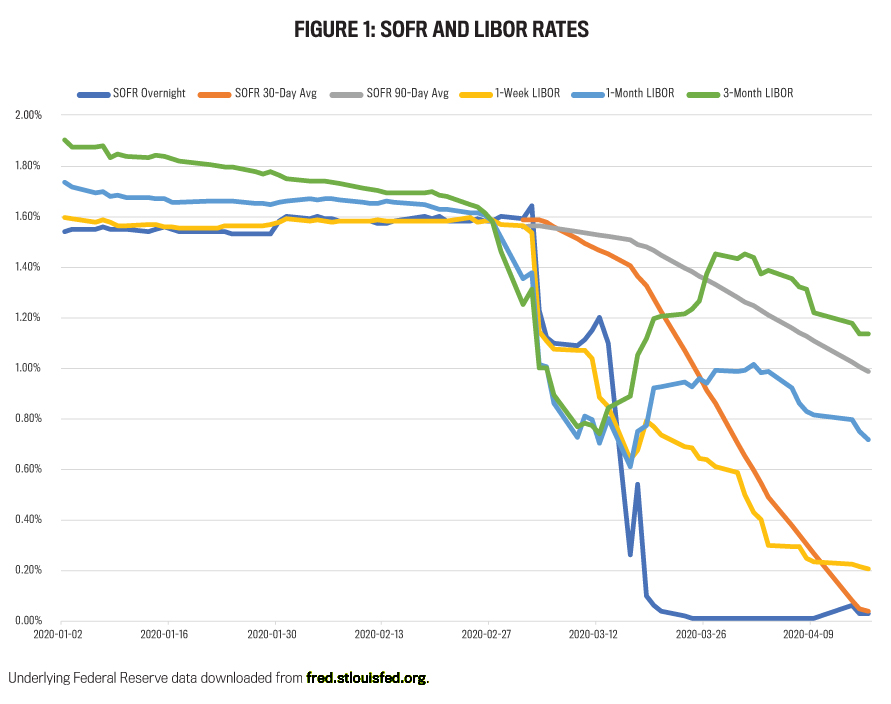

Figure 1 provides some perspective on the relative rates and volatility for six different rates: SOFR overnight, 30-day, and 90-day averages; and LIBOR one-week, one-month, and three-month rates. The SOFR 30-day and 90-day average data cover the period March 2, 2020 (the day the averages started), to April 16, 2020, while the SOFR overnight and LIBOR rates cover the period January 2, 2020, to April 16, 2020. As the figure shows, the four rates (SOFR overnight and LIBORs) moved in tandem with each other in January and February, but all six rates diverged in March and April. The SOFR overnight and 30-day average converged in the middle of April (the end of the data period).

The SOFR standard deviations, even for the 30-day and 90-day averages, were higher than their LIBOR counterparts. The SOFR standard deviations, measured over the period March 2 through April 16, were 0.57%, 0.53%, and 0.19% for the overnight, 30-day average, and 90-day average, respectively, while the LIBOR standard deviations measured over the same period were 0.37%, 0.16%, and 0.22% for one-week LIBOR, one-month LIBOR, and three-month LIBOR, respectively.

Another criticism is that SOFR is generally lower than LIBOR, a contention supported by Figure 1. A closer examination reveals that from January 2, 2020, through April 16, 2020, SOFR overnight was, on average, 12 basis points lower than one-week LIBOR, 26 basis points lower than one-month LIBOR, and 43 basis points lower than three-month LIBOR. During January and February 2020, the one-week LIBOR was, on average, one basis point higher than SOFR overnight.

But from March 2 until April 16, one-week LIBOR was, on average, 27 basis points higher than SOFR. Note that, due to the historical data that is, by definition, part of the 30-day and 90-day SOFR averages, and because interest rates trended downward during the period studied, the SOFR 30-day and 90-day average rates were higher than one-week LIBOR during March.

SOFR doesn’t include the price of bank credit risk, so as a stand-alone rate it doesn’t capture the risk inherent in the short-term unsecured LIBOR rate. This generally requires a “SOFR + spread” adjustment. Critics suggest that for such an adjustment to be effective, there should be some correlation between the unadjusted SOFR and the LIBOR rates and that regrettably the correlation is “not uniform and is very choppy” (see “SOFR, the New LIBOR? A Critique of SOFR and the USD LIBOR Replacement Process” in The Banking Law Journal, September 2019).

We compared SOFR overnight and one-week LIBOR interest rates and found the correlations to be unstable. The correlation rate for the period January 2, 2020, through April 16, 2020, has a very high correlation of 0.963. March has the highest monthly correlation rate at 0.897. In contrast, February has the lowest monthly correlation of -0.375. Despite these fluctuations in monthly correlations, the March 2 to April 16 correlations were high and similar across the different indexes. For example, one-week LIBOR had correlations of 0.87, 0.91, and 0.89 to SOFR overnight, SOFR 30-day average, and SOFR 90-day average, respectively.

Regardless of these perceived deficiencies, the ARRC maintains that SOFR contains favorable characteristics that rates based on unsecured funding markets lack. Although the FASB and the ARRC endorse the use of SOFR, their guidance suggests that other benchmarks may also be appropriate under certain circumstances.

MEETING THE CHALLENGE

As mentioned, the LIBOR sunset holds the possibility of impacting trillions of dollars of contracts. Many of those contracts lack adequate fallback language in the event LIBOR is unavailable during the execution of the terms. ARRC offers extensive guidance on fallback language that should be included in any new or renegotiated contracts, especially those that continue to reference an IBOR rate.

Two issues with renegotiation are noteworthy. The first is the possible unwillingness of the counterparty to agree to new language, and the second is the relatively short window of opportunity before LIBOR sunsets. Such renegotiated changes in language and rate references could alter the agreement significantly, resulting in an entirely new dynamic and accounting complexities.

Note that ASU 2020-04 seeks to provide relief from the increased volatility in reported earning precipitated by the termination of the hedging relationships and existing contracts for financial reporting purposes. Therefore, care must be exercised when renegotiating contracts—especially with concurrent contractual changes that are unrelated to the replacement of an IBOR reference rate, as these may nullify the optional expedients offered in ASU 2020-04.

Because these renegotiations could be detailed and lengthy, companies should begin as soon as possible. This is even more urgent due to the general slowdown created by current world events regarding the COVID-19 pandemic.

So if your company has LIBOR sunset exposure, how should it prepare for the unavoidable? Note that the following suggestions constitute general advice, and modifications and additions may be appropriate for a given organization.

The first step is to determine the company’s exposure to LIBOR. This is most likely accomplished by appointing a team led by an executive-level manager. Placing a high-level individual in the leadership role will convey the importance of the task and ensure cooperation throughout the organization. In this period of social distancing, and with online meetings replacing in-person gatherings, the task is likely to be more time-consuming. The team’s first and arguably most vital task is to identify and review all LIBOR-based contracts.

In 2018, EY identified two possible difficulties with renegotiations. First, in many companies, such loan and derivative contracts are available electronically, which enables analysis. But some contracts may be available in hard copy only and thus require more time to analyze, reinforcing the need to start the review process as soon as possible. The second challenge is the possible unwillingness by contract counterparts to agree. Renegotiation of contract terms may be met with resistance by other parties to the contract, further highlighting the need to start as soon as possible.

After identifying the scope of the task, develop a plan to alleviate the company’s exposure. Companies should plan the renegotiation of contracts where applicable. While doing so, companies should evaluate their internal IBOR-related controls and procedures to ensure that new contracts exclude references to LIBOR or at least include strong fallback language. If it’s determined that contracts should be modified, rewritten, or renegotiated, it will likely be inadequate to simply “plug-in” SOFR for LIBOR in existing contracts.

The comparatively lower SOFR rates are less problematic for new contracts that reference SOFR because such contracts could reference SOFR and adjust the terms of the loans to compensate accordingly and perhaps initially include a spread adjustment. But for existing contracts being renegotiated (or for new contracts that reference LIBOR and may not be executed before the end of 2021), the spread adjustment and fallback positions are crucial. (For more guidance on adjustments and fallbacks, see literature from ARRC at nyfed.org/2MGMm3M and the International Swaps and Derivatives Association (ISDA) at isda.org.)

Once the scope of the company’s LIBOR sunset exposure is determined, establish a strategy to not only strengthen existing contracts (and ensure that new contracts are sound), but also to assess and plan for the impact on net income. Depending on a company’s unique circumstances, the transition away for LIBOR could have a significant impact on earnings. Rate changes across contracts with various tenures could lead to inconsistent or volatile reported earnings over several or many periods. Moreover, the company’s response may take time and be costly.

As with any action, it’s important to monitor progress of the plan once it’s launched, obtaining feedback and making adjustments as needed. Transparency is vital. To the fullest extent possible, all stakeholders should be made aware of the organization’s plans and progress. This will help build trust and ease challenges in case any issues arise during the transition.

Finally, continue to monitor guidance from regulators and rule makers. Even if the company is successful at managing its exposure and transition, the transition is ongoing and fluid on a macro level. As the transition evolves, it’s likely that guidance will do so as well.

GROWING PAINS AHEAD

After a long run beginning in 1969, the LIBOR reference rate has fallen victim to unethical manipulation. As such, the rate will no longer be available after 2021. Companies that have exposure must act soon to begin the transition process. There will likely be some growing pains as contract parties and the market adjusts to the post-LIBOR landscape. The ARRC, the FASB, and ISDA, along with numerous trade organizations and professional companies, are continuously monitoring events and working to assist with the transition. Most have endorsed the use of SOFR, with caveats for spread adjustments, fallback specifications, and alternate reference rates.

But the transition is coming at a difficult time. Tom Wipf, ARRC chair, advises, “We just focus on the facts as we know them. Obviously anything can happen—these are very challenging times—but from the information that we have today, it remains clear that we should be going down the tracks by the end of 2021.” Yet there’s evidence that companies aren’t prioritizing their transition.

Reuters reports that banks and borrowers are preoccupied with their pandemic response and have moved the LIBOR transition down in priority and that small businesses “now have no time to work on LIBOR transition” (see “Banks, borrowers neglect Libor plans in coronavirus maelstrom,” Reuters, April 2020). Reuters quotes a senior executive from a United Kingdom bank who said, “Libor has just fallen way down the priority list, we are running a pilot programme for transition but it’s very difficult to ask companies to find the time to join it.”

The LIBOR transition presented challenges before the current global health crisis, and such difficulties have only been amplified. The transition period seems to be lining up with the pandemic time frame, which will place a further strain on resources and efforts (see “Never Waste a Crisis: How Coronavirus May Help Shape the LIBOR Transition” by Moore & Van Allen PLLC, March 2020, ). Given the current deadline of the close of 2021, the most important action that companies can take is to begin the process of transition as soon as possible while continuing to monitor ongoing events.

July 2020