As the COVID-19 pandemic that first swept the globe in 2020 has taught us, an organization’s capacity for planning strategically, and adjusting as needed to changes in the external landscape, can mean the difference between prosperity and failure. Effective strategic planning is essential to every organization, regardless of industry, and whether or not it’s charged with turning a profit.

Analyzing current conditions and then assessing what those conditions mean for the future is of particular importance to those of us in the strategic finance function. Given the need for financial managers to always operate with a forward-looking strategy in mind—and that the need is even more urgent in times of crisis—let’s consider how best to make plans when even the near-term future seems uncertain or threatening.

WHERE TO START

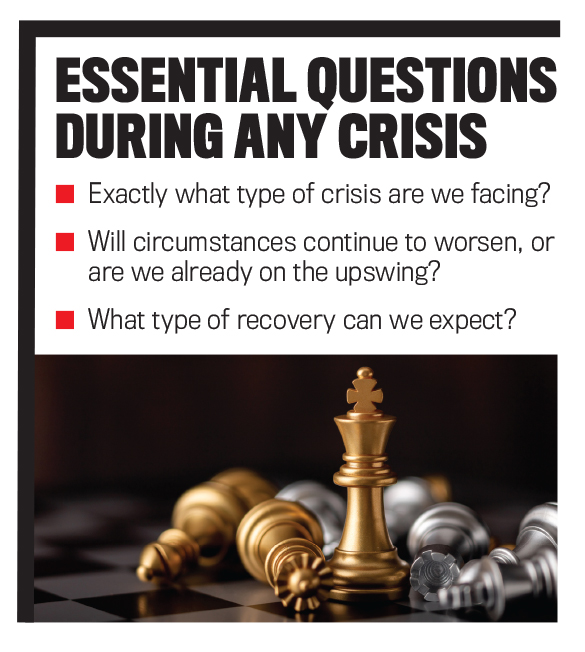

In this scenario, organizations should focus on asking a series of initial, essential questions. Exactly what type of crisis are we facing? Will circumstances continue to worsen, or are we already on the upswing? When will there be a recovery, and what type of recovery will it be?

Then, after getting a handle on these basics, it’s necessary to focus on the financial particulars unique to the current environment. What do we project for the economic and interest-rate environment? Will there be any form of government relief or stimulus to help soften the blow? How do we expect other companies—either like or unlike our own—to weather the storm?

When it comes to planning strategically, during a crisis or otherwise, organizations focused on sustainable growth are typically quite adept. The reason for this is simple: You don’t keep expanding without having carefully charted a course that you regularly review and, as needed, reassess.

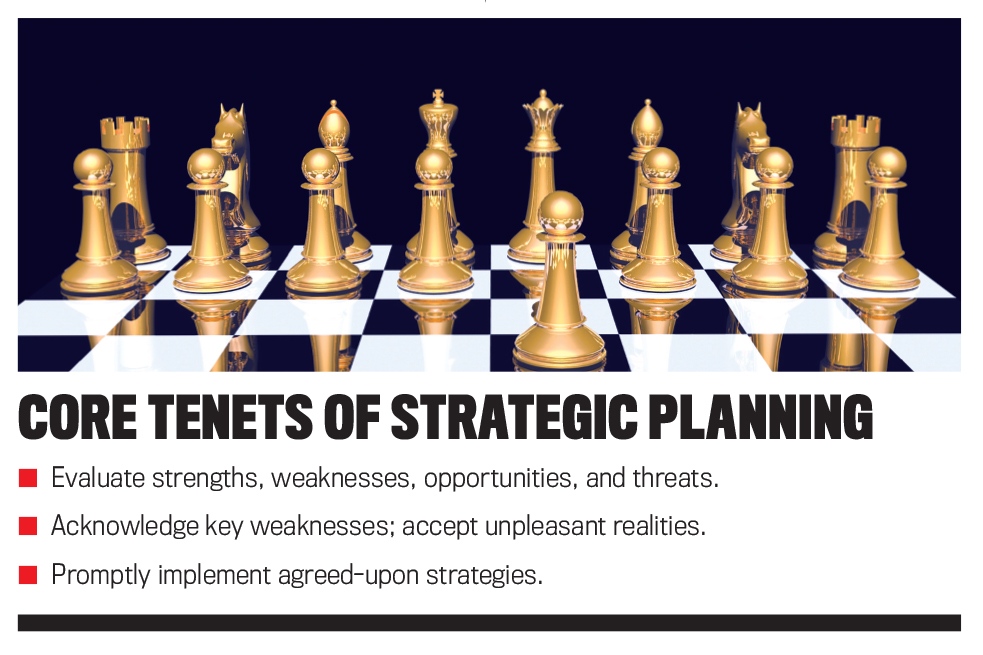

Any strategic plan needs to include a few essentials, with an emphasis on the evaluation of strengths, weaknesses, opportunities, and threats (SWOT). The tried-and-true SWOT analysis, appropriately customized to address the specific circumstances at hand, may seem like a simple undertaking, but even the savviest of business leaders can struggle to identify—or perhaps admit to—key weaknesses and threats with the potential to impede a strategic initiative.

This highlights the fact that to be truly effective, a plan must not gloss over or fail to acknowledge unpleasant realities. It needs to be brutally honest—even, if need be, at the expense of individual egos. This is even more important during challenging times, when a strategic plan will likely need to take effect immediately. If it includes “gaps” to spare someone’s feelings, it not only is likely to fail, but it may do so with disastrous results for the company that implemented it.

A company can’t successfully execute a large-scale corporate initiative, like a merger for example, without substantial advance planning. These are remarkably complicated endeavors that require extensive evaluation and analysis, as well as the creation of a comprehensive plan that will likely change over the course of time.

Kearny Bank, for which I serve as CFO, was recently named by Fortune as one of the world’s fastest-growing companies, and as a result, I have a distinct perspective on this. Our strong commitment to advance planning prepared us to make plans when times got tough.

Early in 2020, we were in the midst of a merger transaction. Negotiations were completed, and we had made a public announcement. There was every reason to believe this was going to be little different than the many other mergers we had completed in the past.

Then the pandemic struck. Almost immediately, we were contending with challenges that we had never previously encountered, including two entirely remote workforces, a floundering and uncertain economy, and interest rate and credit environments that were, at best, unpredictable. Yet, despite this multitude of serious issues, we still bore the responsibility of ensuring the successful completion of the transaction.

It was a challenging situation, but one to which we were able to bring an extraordinary amount of forethought and planning. And in the end, everything worked out. This was the case, in large part, because we had been willing to be candid, not simply about the difficulties that confronted us, but also about what, at least at the time, we didn’t entirely know.

If there’s one thing more dangerous than a flawed or inaccurate strategic plan, it’s having no plan at all. Even the most routine of corporate actions need to be driven by careful, advance planning. Otherwise, they almost certainly won’t succeed. And what’s the point of moving forward with an initiative, even one of limited scope, if it isn’t your intention to be successful? To use a crude analogy, leading an organization without a strategic plan is like driving across the country without using navigation. You may eventually arrive at your intended destination, but you’ll make a host of wrong turns, end up lost more than once, and invariably be very, very late.

WHAT NOT TO DO

When thinking about flawed strategic plans, one example that comes to mind is that of now-defunct Green Tree Financial. In the 1990s, Green Tree executed a strategy of providing borrowers with long-term mortgages on mobile and manufactured homes, which were then securitized into asset-backed securities. At the time, this approach was applauded, and Green Tree raked in sizable profits from origination fees.

But mobile homes are much like cars in that they depreciate quickly, and many borrowers found themselves owing much more than the asset was actually worth. Inevitably, this led to a barrage of defaults. At its peak, Green Tree was providing financing in all 50 states while controlling more than 40% of the mobile and manufactured home financing market. But by 1998, the company was acquired by Conseco Inc., and, shortly thereafter, Conseco began taking annual write-downs that ultimately totaled in the billions.

Regardless of the quality, or lack thereof, of an organization’s strategic plan, there comes a time when that plan must be executed. In the midst of challenge and uncertainty, there’s rarely a shortage of risk-averse leaders whose inclinations tend toward taking a wait-and-see approach.

Unfortunately, in more than a few cases, “wait and see” is actually a euphemism for being paralyzed by worry or fear. There’s a very fine line between pragmatic caution and failure-inducing indecision.

Whether in business or day-to-day life, every situation presents a trio of options—do nothing, do something, or do something more. Undoubtedly, “do nothing” may be an entirely appropriate initial strategy. But the tipping point comes if the crisis at hand continues to worsen. In that case, an effective leader will be willing to change course and try something different, while an inadequate leader will be overwhelmed by irresolution, to the detriment of the entire organization.

ACTION IS ESSENTIAL

There are times when pausing to assess current conditions can be a wise move, particularly if there’s a reasonable possibility that circumstances may improve on their own. More often, delaying implementation of a response enables chaos—or outside players or parties—to seize control of the situation and dictate the future.

In 2008, in the midst of what would become known as the Great Recession, I was working for a small start-up. During the earliest stages of this crisis, the company’s finance team was almost exclusively focused on immediate concerns like short-term liquidity management. Long-term strategic considerations needed to be placed on the back burner.

At one point during this period, the commercial paper market had frozen, which was where a portion of the company’s short-term investment dollars were placed. It was a frightening scenario, since initial indications were that redeeming those securities for cash in a timely manner would be nearly impossible. Eventually, the U.S. Department of the Treasury and the Federal Reserve would step in to support that market, but we had no way to know that in the initial days. In order to solidify our liquidity position, we needed to act rapidly to apply unrelenting pressure on our counterparties to ensure the dollar-for-dollar redemption of those securities.

While I wouldn’t want to have an experience like that again, it’s an effective illustration of how there’s no room to hesitate or be timid when an immediate and forceful response is necessary.

STICK TO THE MISSION

During challenging times, how can companies leverage their strategic plan to help them weather the figurative storm? It should always begin with staying focused on long-term goals and not overreacting to current conditions. And that means being aware of or refamiliarizing yourself with your company’s mission and vision statements. These speak to where a company desires to go, and they remain its guiding principles regardless of how difficult circumstances may be.

At Kearny Bank, for example, our mission statement emphasizes a focus on people, performance, and relationships. These particular points of emphasis are hardly unique to a bank. But when a crisis occurs and everyone is scrambling to manage the situation at hand, this mission statement is a valuable reminder to focus on the aspects of the business that provide long-term stability and value.

Kearny Bank was established in 1884, when the United States was a very different place. So different in fact that, at the time, the country was comprised of only 38 states. In order to survive, and thrive, across the better part of 15 decades, it has been essential for the bank to remain true to its core competencies, like issuing well-underwritten loans to qualified borrowers and providing appropriately designed deposit products to our clients.

Sticking to these key tenets of our business model, which are in direct alignment with our mission statement, has enabled the bank to navigate a host of adverse business environments, including the Great Depression, two World Wars, the financial crisis of 2008-2009, and a wide variety of other social, economic, and military crises.

With the importance of mission and vision statements in mind, it’s imperative, as part of any strategic planning process but particularly during difficult times, to keep in mind exactly what the company does well—ideally, what it does better than its competitors. This is best determined via a careful assessment by senior decision makers, who then must reach a consensus about strategic direction and organizational competencies. Companies do many different things, and the larger the company, the more it’s likely to do. But by focusing on and emphasizing a few key areas of excellence, an organization puts itself in the best possible position to overcome short-term challenges.

It’s then essential to identify all of the immediate risks, with an understanding that there will be more than usual because of the crisis at hand. But risk always comes with the potential for reward, so it’s also imperative to consider opportunities for growth that may be unique to the current environment.

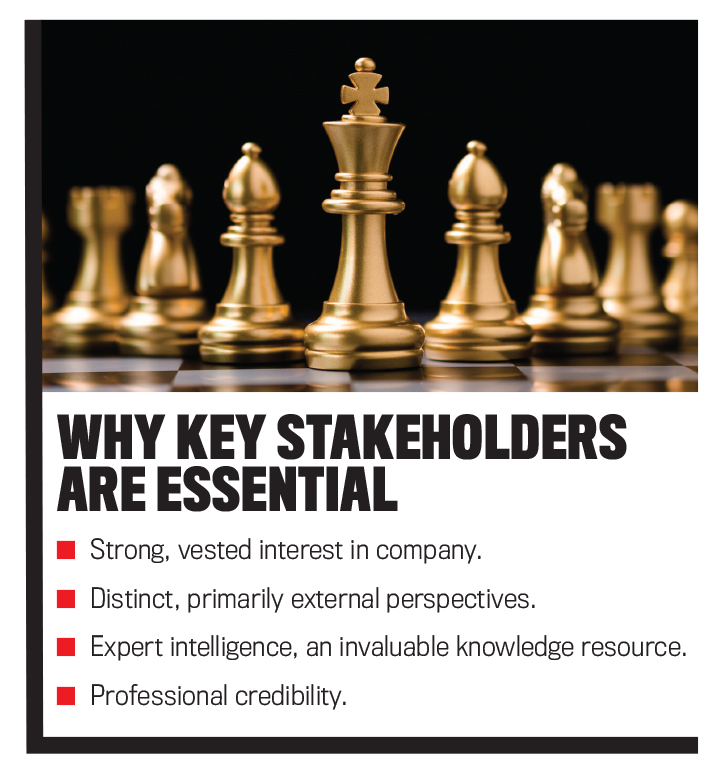

Once all of this is done—once leadership agrees on what makes the company strong, what its core direction is, and what risks and opportunities exist—then it’s time to directly engage with key stakeholders such as clients, stockholders, employees, lenders, regulators, and the communities that the company serves. These groups all have a vested interest in the success of the company, and their perspectives—though they may differ from those of senior management, or perhaps specifically because of that difference—are invaluable. This expert intelligence, refined by the natural self-interest of each stakeholder when merged with conventional market intelligence gathered via various channels, creates a knowledge resource that must be an essential component of the planning and decision-making process.

Along with other members of Kearny Bank’s management team, I spend a significant amount of time interacting with key stakeholders. Whether through in-person exchanges, phone conversations, or online sessions, we gather opinions about how the company can continue to evolve. In addition to helping us determine how well we’re addressing the needs of essential constituents, the information we collect quite often provides our management team with valuable insight that influences the process of tactical and strategic decision making.

Engaging with stakeholders can be a complex and time-consuming process, but it’s invaluable, and it often provides a level of intelligence that simply isn’t available elsewhere. And because it comes from those who have a distinct interest in the ongoing success of the company, it provides an unmatched degree of credibility.

TAKE THE LEAD

When discussing strategic planning and decision making, there remains one final consideration. Despite the time and effort put into the planning process, the amount of intelligence gathered, and how committed key stakeholders are to supporting an organization’s future, when times are at their most challenging, there is one factor that will often determine success or failure. That factor is leadership. Without a leader or a leadership team taking in all available information, providing expert analysis, and then making confident decisions, success is likely to be fleeting.

Consider the example of Paul Volcker, economist and chair of the Federal Reserve from 1979 to 1987. He was an exceptional leader due in part to his successful resolution of the extended period of runaway inflation in the 1970s. At the time, his decisions were often criticized, and he was blamed for plunging the U.S. into a recession.

His actions were so unpopular that, in 1980, public protests erupted in the streets of Washington, D.C. Yet Volcker didn’t shy away from making the difficult decisions that he believed to be right. He understood intrinsically that successful leadership was ultimately measured by accomplishment, not popularity. And now, years later and with the benefit of hindsight, his actions are widely considered to have been the key to stabilizing the economy and leading the U.S. into long-term economic prosperity.

While leadership is always critical, it’s even more so during challenging times. It’s in these periods when the quality of leadership will ultimately determine whether an organization becomes a casualty of circumstances or is able to continue on into better, more prosperous times.

July 2021