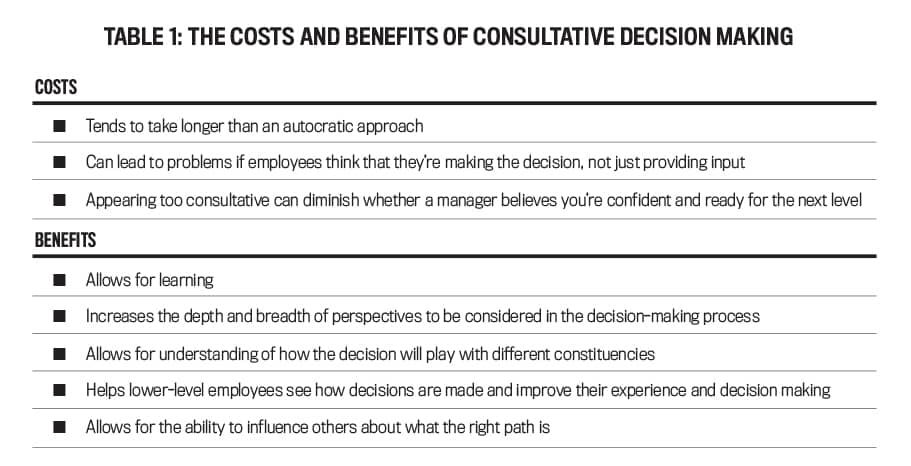

CONSULTATIVE DECISION MAKING

Simply put, consultative decision making is a process of soliciting input from others but making the final decision yourself. Contrasting decision styles include (1) autocratic, i.e., making decisions on one’s own without input, or (2) consensus, i.e., making decisions as a group. Consultative decision making has substantial benefits: It increases the number of perspectives considered, increases the understanding of how others will interpret the information presented, allows for the opportunity to build consensus or buy-in for a decision, and engages employees. In addition, being consulted can allow employees to learn how to—or how not to—make decisions. (For more, see Table 1.)

There are some potential costs as well. It can be slower and can lead to problems if employees providing input don’t realize that they’re only advising the decision maker, not making the actual decision. This is the difference between “consultative” and “consensus” decision making. For example, if you’re a leader who takes a consultative decision-making approach, you would solicit input from group members but make the decision on your own. In consensus decision making, however, you would work with the group until it votes on a course of action. Consider the situation in which the financial planning and analysis group is trying to decide whether to move from a manual Excel-based system to robotic process automation. The group leader—you, perhaps—would assemble the team and ask for input on the risks, value, time, and effort involved. In this example, imagine that the leader gets the sense that the group is against the change. A consensus-based decision would lead to no change, no automation. A consultative leader, however, would decide to automate if the cost-benefit analysis indicated it was the right decision, even if a majority of the group was against it. The decision would be made with input and more knowledge than if the leader had made it without consulting the group, but there would be no need to convince the group to agree with the decision.

THE WEIGHT OF IMPRESSIONS

It’s important to realize that consultative decision making not only leads to a decision, it creates an impression on others. That impression can be simultaneously positive and negative. On the one hand, a consultative professional is likely to be seen as someone interested in learning, which positively influences their performance evaluations. Or they may be viewed as lacking confidence and possibly as someone who depends too much on others. In contrast, a more autocratic decision maker will be seen as someone with greater self-sufficiency and more confidence. The negative impact of an autocratic style, however, is that the professional doesn’t learn as much from the process. Whether the positive impression created by consultative decision making outweighs the negative impression depends on where you are career-wise. At a lower level, consultative decision making is crucial. As you progress from the very early stages of a career, learning and trying to grow in the organization is imperative. Most professionals progress from unconsciously incompetent (they don’t know what they don’t know) to conscious incompetence (they know what they don’t know) to competence. This progression requires time and experience. Thus, it seems appropriate that managers look favorably on consultation at these lower levels. In contrast, when a person is on the cusp of promotion, managers look for signs of confidence. Therefore, at this stage, consultation is negatively related to the employee’s promotion prospects. Moreover, managers are less likely to look for signs of learning at this stage because they assume professionals have learned enough and are ready to move on to the next level.SUBJECTIVE PERFORMANCE EVALUATION

Managing impressions and knowing what bosses are looking for is vital in subjective performance evaluation situations. When jobs can’t be evaluated based on quantifiable performance measures, performance evaluation needs to be judgment-based. Subjective performance evaluation therefore focuses on tasks that can’t be quantified, like quality, creativity, personality, work ethic, attitude, and demeanor. When the job itself involves judgment, performance evaluations focus even more on these dimensions because outcomes are hard to measure. For example, did the employee deliver excellent work in a timely and professional manner? Although we can measure whether the deadline was met, this provides no indication that the product was also excellent and delivered in a professional manner. These aspects need to be assessed subjectively. When performance is assessed and not measured, the organization relies on evaluators’ perceptions and judgments. Although this allows managers to make adjustments to create fairer evaluations, it also can open the door to bias and favoritism. Even when managers aren’t intentionally biased, they may resort to shortcuts and stereotyping due to cognitive limitations; in short, as humans, we simply can’t process all the information we have. Most supervisors would prefer objective measures for ease of evaluation, but objective performance data doesn’t exist for many jobs. Because they’re professional careers, public accounting and corporate finance are rife with subjective performance evaluations. For example, each year performance is reviewed for finance and accounting professionals often using ratings of characteristics that will make for successful team players—knowledge, communication skills, professional judgment, teamwork, inclusivity, etc. Each one of these characteristics is subjective. Being a knowledgeable professional with good judgment and communication skills is going to help you be successful, but it isn’t enough. You need to be highly rated as well. To this end, try to understand how you’re being evaluated. Knowing how your boss will likely see you can help you use that information to perform in ways that qualify you for that promotion.PERFORMANCE EVALUATION VS. PROMOTION ELIGIBLE

In a professional organization, it can take years of learning the ropes at each level before getting promoted. The first year at any level is a year of learning and growth. Say you’re a first-year corporate accountant responsible for bank reconciliations, sales tax, accounts receivable analysis, and fixed-asset purchases. While you undoubtedly learned about each one of these tasks in school, understanding what to do, when to do it, and how to do it in the real world takes time. Being able to close the books at month end and seeing the variations through a seasonal business develops your ability and judgment. Without seeing that whole picture, your rookie experience is incomplete. This is why, throughout accounting and finance, it’s rare to get promoted to the next level within the first 12 months. When managers are evaluating their subordinates, they ask themselves whether these people are learning and progressing as expected. Are they on track? Do they have what it takes to make it at the next level? If not, are they heading in that direction? The more years someone remains at a certain level, the more the prospect of promotion looms in evaluation. That’s why managers may look for consultation at the early stages of a level, but not as promotion approaches. To test this idea, Bol and Leiby met with practitioners in consulting, audit, and tax and conducted two research studies—one with consulting managers and one with public accounting managers. The findings showed differences in how employees were rated depending on whether they were promotion eligible or far from promotion. Bol and Leiby found evidence that this is because supervisors look for different characteristics in people who are eligible to be promoted.THE INITIAL RESEARCH STUDY

Using input gleaned from interviews with 14 senior consultants, Bol and Leiby designed a rich study that would allow them to make broad conclusions about consultation and performance evaluation. One insight repeated by several consultants was that objective measures play a smaller role in promotions, raises, and other meaningful decisions than some might suspect. One consultant even suggested that people making promotion decisions rely solely on their subjective evaluations. Armed with this insight, Bol and Leiby asked managers to assess two junior professional workers who perform nonroutine tasks. One junior employee was somewhat experienced (and therefore eligible to be promoted); the other was a complete rookie and not likely to move up at this time. To operationalize this promotion eligibility, the participants were told that the rookie employee had been with the company for one year, and the promotion-eligible employee had been there five years. The company’s standard career path involved six years at the first level. Bol and Leiby showed managers some descriptions of the young professionals and asked them to rate each employee’s current level of performance and promotion prospects. (Each manager rated a rookie and a promotion-eligible employee.) The information that was constant across managers contained measures of customer satisfaction, budget variances, and project outcomes. In addition to the objective performance metrics, evidence of the two employees’ positive reputations and positive interactions was shared with each manager. What differed was information about employees’ decision-making styles. Some managers were told that both employees exhibited a consultative decision-making style (“sought advice from peers with relative frequency”), some were told that both employees exhibited a more autocratic style (“sought advice from peers with relative infrequency”), and some weren’t told anything about employees’ decision-making style. The results are very interesting for employees looking to be evaluated favorably and get promoted. Consultative junior employees not eligible for promotion were rated highly for current performance and promotion prospects. Those promotion eligible and consultative were rated as equally high on current performance as those who didn’t consult, but they were rated as less likely to be promoted. This not only provides insights into when to consult and when to refrain from consulting, it also shows that higher current performance evaluations don’t automatically result in higher promotion prospects. This finding poses an interesting dilemma: Why are early-stage employees rated highly and seen as promotable when they’re consultative, but later in the career stage they’re less likely to be viewed as promotable even if they continue to be consultative?THE FOLLOW-UP STUDY

Bol and Leiby’s review of the decision-making literature led them to the idea that complex judgments, like subjective performance evaluation and promotion eligibility, are made simpler by schemas, which are mental models that simplify large or difficult sets of information (see “What Are Schemas?”). As decision makers, we compare information to our schemas to see whether it matches. If it does, the decision has a favorable outcome; if it doesn’t, the decision is unfavorable. Bol and Leiby suspected that managers had different schemas in their minds that helped them make judgments about performance and promotion prospects. That is, the same indicators are used differently depending on the focus of the decision maker.

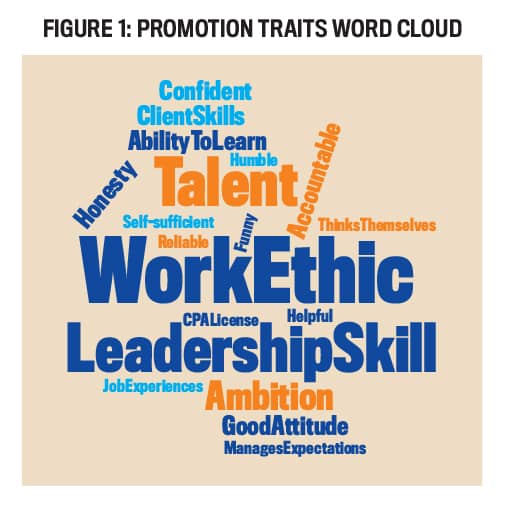

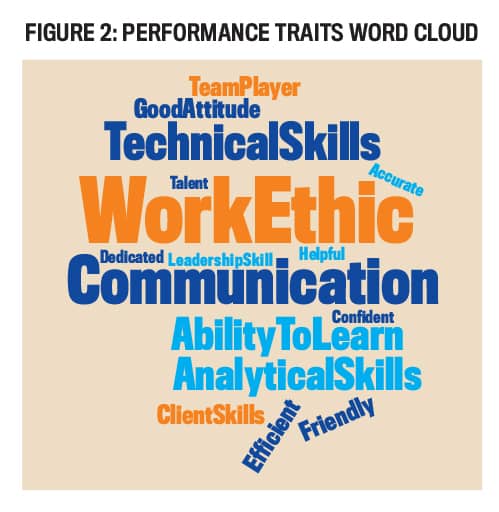

They conducted a second study, involving audit and tax managers and partners, to help explain why people were making certain recommendations. The researchers had a hypothesis that people thought differently about what qualities were important for an annual performance evaluation vs. what qualities were important for promotion. These “different thoughts” were likely organized in people’s minds as schemas. The participants in the second study were asked to list three important qualities of people who would be successful if promoted (see Figure 1) or three important qualities to describe people who are currently performing well (see Figure 2). There’s some overlap, but also substantial divergence. Both schemas include items like work ethic, client skills, and talent. The promotion schema, however, focuses on leadership, intelligence, ambition, professionalism, honesty, and listening skills. The performance schema, in contrast, zeroes in on efficiency, questioning, and skepticism.

Bol and Leiby interpret this as evidence that managers organize their thought processes differently depending on whether they’re evaluating an employee for promotion or for current performance. The performance schema focuses on current contributions, and the promotion schema examines how the employee will contribute at the next level.

PROMOTION OR NO PROMOTION?

Following the schema elicitation, the participants were asked to make either a performance or promotion decision for two employees, one promotable and one not. These results are consistent with those of the first study, with one exception: The promotion-eligible professionals who were consultative still received lower scores than nonconsultative professionals for promotion prospects but received higher scores for current performance. Bol and Leiby believe that this is because consultation is explicitly encouraged by professional standards. Other results, too, remained the same: More consultative and nonpromotable employees were rated higher on current performance and promotion prospects compared to less consultative and nonpromotable employees. For promotable employees, less consultative employees were seen as more promotion worthy. A natural question arises: If managers have different schemas for current performance and promotion prospects, then why were consultative rookies rated higher on both their performance and promotion prospects? Did managers’ schemas emphasize the same characteristics for rookies? Bol and Leiby explain that when managers evaluate the promotion prospects of a rookie, when eligibility is still far away, they aren’t yet concerned about performance at the next level. They’re still focused on what the employee can do now. Current performance at this stage is the best indicator of being on track and having good prospects for promotion.MAKE CONSULTATION WORK FOR YOU

These findings have significant implications for careers in professional services, such as consulting, public accounting, and engineering, and in corporate accounting or finance departments that are structured as shared services organizations. Because these are professional fields and employees are evaluated subjectively, it’s good to know what schemas managers use when they review your current performance and promotion prospects. It’s also helpful to know that your manager’s evaluation schemas change as you gain experience. As you navigate your way through your career, think about expectations for consultation. Early on, supervisors tend to look for, and value, consultation. Consultation brings with it learning, and managers expect employees to consult and learn as they begin each level. Your first six months on the job, and your first six months at a new level, should be filled with questions. Ask why things are done a certain way. Ask about the technical details of how to prepare a report or analyze the data. Consult on what the priorities are and where to get help. Work with your peers to learn from them and be very consultative in your decision making. Demonstrating curiosity and a desire to learn are going to be highly valued traits for your annual performance appraisal. After you’ve been at a level for a while (determined by organizational norms), you should reduce consultation, demonstrate confidence, and consult with your peers less. You should show that you’ve made decisions based on your own knowledge and judgment. Focus on advising subordinates or peers, not asking them for input. In deciding whether you’re ready to go to the next career level, managers are looking for more certainty and self-reliance. While it may be the norm where you work to consult your colleagues, you’ll need to carefully consider reducing consultation as you prepare to be promoted. This strategy may seem counterintuitive at times, but it can increase your odds of success.

July 2022