Corporate bribery is bad business. In our free market system it is basic that the sale of products should take place on the basis of price, quality, and service. Corporate bribery is fundamentally destructive of this basic tenet. Corporate bribery of foreign officials takes place primarily to assist corporations in gaining business. Thus foreign corporate bribery affects the very stability of overseas business. Foreign corporate bribes also affect our domestic competitive climate when domestic firms engage in such practices as a substitute for healthy competition for foreign business.—United States Senate (1977)

Corporate corruption has long been recognized as a global issue that victimizes honest businesses and impedes long-term social and economic development. Enacted in 1977, the U.S. Foreign Corrupt Practices Act (FCPA) prohibits U.S. organizations, companies that are listed on the U.S. capital market, and certain non-U.S. organizations that conduct business within U.S. territories from offering bribes to foreign officials to obtain or retain business.

The FCPA seeks to deter corporate corruption by making foreign bribery more costly. The U.K. equivalent of the FCPA, the U.K. Bribery Act, was passed in 2010. Similar laws and regulations have also been enacted in other countries such as Brazil, Canada, and China. As enforcement of these anticorruption laws, especially the FCPA, has dramatically intensified in recent years, it becomes imperative that organizations doing business outside their home country have a comprehensive understanding of the costs of foreign bribery.

FCPA ENFORCEMENT ON THE RISE

The FCPA contains two sets of provisions. The antibribery provisions prohibit organizations from making bribery payments to foreign officials in exchange for unfair business advantages, and the internal control provisions require organizations to maintain effective internal control systems and accurate accounting records. The U.S. Department of Justice (DOJ) and the U.S. Securities & Exchange Commission (SEC) jointly enforce the FCPA.

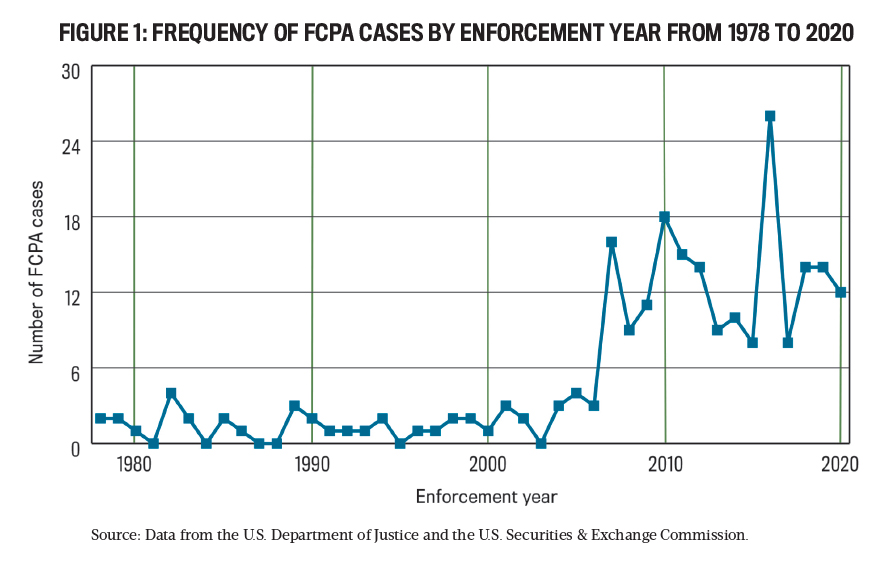

Recent years have seen a rapid increase in the frequency of FCPA enforcement. According to a 2020 Strategic Finance article (“Kicking Back Against Kickbacks,”), an average of fewer than two FCPA cases were pursued each year from the FCPA’s inception in 1977 to 2000. After 2000, however, prosecution increased to more than nine cases per year (see Figure 1).

The social, economic, and legal factors that may have contributed to this upward shift in enforcement frequency include the following:

- Globalization of the world economy

- Cross-border cooperation in anticorruption enforcement

- Expanded scope of the FCPA in its 1998 amendments

- Passage of the Sarbanes-Oxley Act of 2002

- Financial motivation of enforcement agencies

- New FCPA resolution vehicles

- Increase in the SEC budget

COSTS OF ALL KINDS

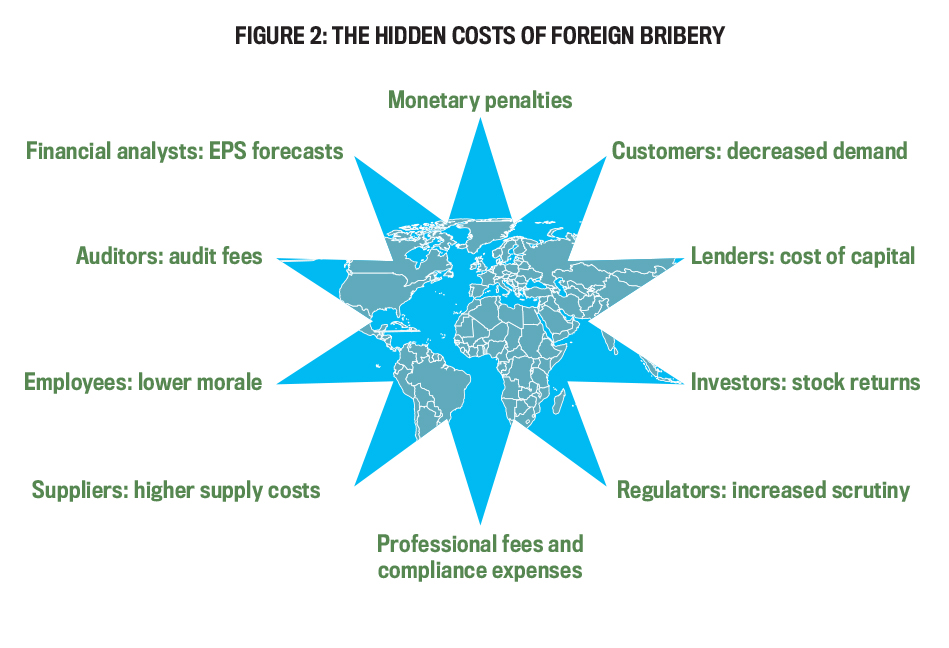

Vigorous enforcement of the FCPA has triggered complaints from multinational organizations that are primarily concerned about the potential costs associated with FCPA scrutiny. While some costs are easy to identify, others are less straightforward and may be easily overlooked. As FCPA enforcement intensifies, companies must understand and be prepared for the direct, indirect, and sometimes hidden costs of foreign bribery (see Figure 2).

Click to enlarge.

Monetary penalties: Organizations targeted in FCPA enforcement actions face financial exposure on multiple fronts. The most direct costs are monetary sanctions imposed by the enforcement authorities, i.e., the DOJ and SEC, which typically consist of disgorgements, prejudgment interest, and civil and criminal fines. In addition to increased enforcement frequency, another noticeable trend in FCPA enforcement in recent years is greater monetary penalties imposed on FCPA defendants. Before 2000, the average monetary sanction per FCPA case was around $3.5 million. This number increased to nearly $61 million after 2000, representing an increase of more than 17 times.

Several influential FCPA cases, such as cases against Siemens, Halliburton, Total, and Alcoa, also made the headlines of major financial newspapers for their hefty settlement amounts. While the substantial monetary sanctions imposed on FCPA defendants should be a cause for concern for multinational organizations, in the overall picture of FCPA compliance, monetary sanctions are actually “often only a relatively minor component of the overall financial consequences that can result from FCPA scrutiny or enforcement in this new era,” wrote Mike Koehler, law professor and leading expert on the FCPA, in his 2014 book, The Foreign Corrupt Practices Act in a New Era. He further suggests that FCPA enforcement could create a ripple effect that extends to various aspects of an organization.

Professional fees and compliance expenses: In addition to court-mandated penalties, organizations targeted in FCPA enforcement actions also pay substantial professional fees to law offices and accounting organizations for legal services, internal investigations, and the design and implementation of FCPA compliance programs. According to a 2015 article in The Economist, Siemens spent more than $3 billion on FCPA compliance on top of the $800 million in court-mandated penalties for its FCPA violations in 2008. Avon incurred $350 million in legal and compliance fees, which is more than double the imposed penalties ($135 million) and “not far short of its 2014 operating profit.”

Since FCPA compliance usually involves complicated procedures and can be quite challenging for organizations that operate in multiple markets around the world, the expertise provided by professional service organizations is very beneficial to an organization’s FCPA compliance, but it often comes at a steep cost. Moreover, professional and compliance costs often escalate soon after the initial concern about bribery is raised, as noted by Koehler in his 2018 article in the American University Business Law Review. Scrutiny is heightened throughout the organization. The logical next question from executives and investigators is, “Is this happening elsewhere?”

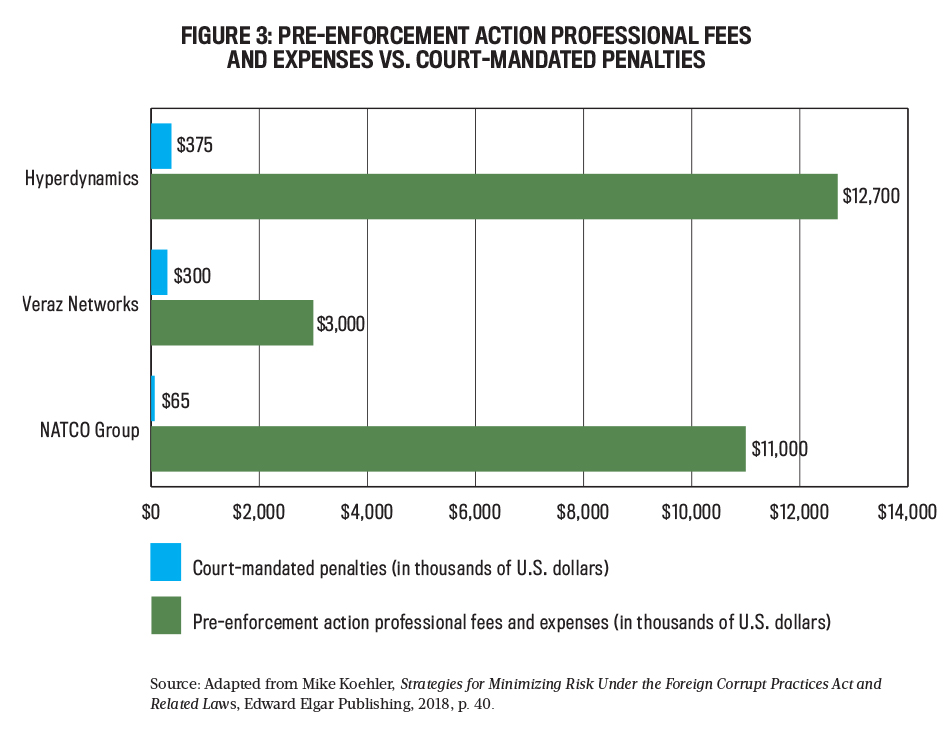

The process of expanding scrutiny may be referred to as the pre-enforcement action. These costs include internal investigations, interviewing witnesses to gather information, reviewing documents, and expanding the investigation to operations in other countries where permitting, licensing, and compliance issues may be related. Reproducing relevant documents and preparing reports for the government are also major costs.

For smaller organizations, the cost of pre-enforcement may be 10 or more times the actual enforcement action. For example, although they incurred settlement amounts ranging from $65,000 to $375,000, the approximate spending on professional fees and expenses was $11 million for NATCO Group, $3 million for Veraz Networks, and $12.7 million for Hyperdynamics. (See Figure 3. For more information, see Koehler’s 2018 book, Strategies for Minimizing Risk Under the Foreign Corrupt Practices Act and Related Laws.)

Click to enlarge.

Stock market reaction: For publicly listed organizations, managing stock market expectations and maximizing shareholder value are often top priorities. For these organizations, becoming an FCPA target comes with another cost: the negative stock market reaction.

An FCPA enforcement action triggers a number of concerns for stock market investors about the future prospect of the organization. First, investors anticipate court-mandated penalties and increased compliance expenses, which negatively affect the organization’s profitability. The loss of future business in the foreign market could also raise investors’ concerns about the organization’s long-term growth and competitiveness. Second, investors may become worried that FCPA investigation and compliance could divert management’s attention from normal business operations, which can impair the organization’s operating performance.

Given these negative consequences of an FCPA enforcement action, it isn’t surprising that the stock market generally reacts negatively to news of FCPA enforcement. In their 2017 working paper, “Foreign Bribery: Incentives and Enforcement,” Jonathan M. Karpoff, Scott Lee, and Gerald S. Martin showed that on average organizations experience a stock return decrease of around 3% when an FCPA enforcement action is initially revealed. As more information about the case is uncovered through later events, the organization’s cumulative stock return decreases by more than 5% after adjusting for overall market returns, representing a significant loss of an organization’s market capitalization.

To the extent that stock returns provide a measure of aggregate investor sentiment toward an organization’s future prospects, the negative stock market reaction to the FCPA enforcement suggests a decline in investor confidence in the FCPA-targeted organization. Around the time of the passage of the U.K. Bribery Act 2010, a similar drop in firm value can be found in U.K. firms that operate in countries with a high rate of corruption, according to Stefan Zeume (“Bribes and Firm Value,” The Review of Financial Studies, May 2017).

Analyst forecast revision: Financial analysts are information intermediaries who collect, synthesize, and distribute information to investors. Similar to stock market investors, financial analysts also react negatively to an organization’s involvement in an FCPA enforcement action. Weishi Jia’s 2017 doctoral dissertation, “In the Aftermath of Foreign Bribery: The Ripple Effects of Anti-Corruption Enforcement on U.S. Multinational Firms,” analyzed the earnings forecasts for organizations accused of FCPA violations. This investigation reveals that analysts revise their earnings forecasts downward for an FCPA-targeted organization in a systematic manner.

On average, a targeted organization’s earnings per share (EPS) forecast drops from $2.99 per share to $2.92 after news of FCPA enforcement. Moreover, the magnitude of analysts’ forecast revisions is strongly associated with the amount of court-mandated penalties imposed on the targeted organization—larger penalties lead to larger downward revisions.

One example of such an analyst forecast revision is for Och-Ziff Capital Management (now Sculptor Capital Management), a hedge fund that was being investigated for its potential FCPA violations in multiple African countries including Libya, Chad, Niger, Guinea, and the Democratic Republic of the Congo in 2016. According to a news report by James Passeri on TheStreet (“Looming DoJ Investigations Dampen Och-Ziff Outlook”), upon news of Och-Ziff’s FCPA investigation, financial analyst Daniel Fannon from Jefferies Financial Group cut Och-Ziff’s 2017 earnings forecast from $0.88 to $0.62 a share—an 18% decrease—and downgraded the organization’s investment rating from Buy to Hold.

Fannon explained his revisions in a report: “The FCPA investigation is having an impact on multiple fronts including the firm’s profitability, capital position (i.e., legal costs, potential fine, etc.) and client demand for its products.” A similar downgrade for Och-Ziff was also performed by Keefe, Bruyette & Woods, which dropped its rating from Outperform to Market Perform, citing uncertainties arising from the investigation. Overall, given the vital role of financial analysts in capital markets, the downward analyst forecast revisions signify analysts’ increasing concern for the organization’s outlook, which could further affect investors’ assessment of the organization.

Cost of capital: The cost of capital or access to capital is another hidden cost for organizations that are charged with FCPA violations. For example, Avon’s credit was downgraded by Fitch Ratings, and Willbros Group Inc. had its line of credit reduced by one-third, from $150 million to $100 million.

All multinational organizations must be mindful of the local environment for bribery activity because it affects access to local lending. While it’s advantageous for organizations to borrow in the local currency so that repayment doesn’t require currency exchange, borrowing locally may be hindered by corruption. Shusen Qi and Steven Ongena, in their Financial Management article published in 2019, found that bribe activity causes greater uncertainty for lenders, and one standard deviation in the number of organizations involved with bribery reduces credit access by 9.2%.

The researchers demonstrate that this isn’t just an association: The local bribery is the cause of the reduced access to credit. Moreover, the problem is driven by supply, so organizations that don’t plan to engage in bribery are equally affected, and the lack of access to credit impedes organizational growth.

Audit fee increases: Auditors contribute to the efficiency of a capital market by independently providing assurance on the credibility of an organization’s financial statements. How do auditors respond to an organization’s FCPA risks? For auditors, client organizations with FCPA violations present higher audit risks because those violations reveal deficiencies in the organization’s internal control systems, suggesting increased control risks, which is a key element of audit risk. Moreover, audits of organizations with FCPA violations may require greater effort because auditors have to perform specific procedures to address risk factors identified in FCPA investigations.

Overall, FCPA cases can increase targeted organizations’ audit fees by increasing the risk and effort associated with the audits. Consistent with this notion, in a 2019 study in Auditing: A Journal of Practice & Theory, researchers Bradley P. Lawson, Gerald S. Martin, Leah Muriel, and Michael S. Wilkins showed that on average, FCPA violators pay 36% higher audit fees than nonviolators. Audit fee increases for FCPA violators occur during both the FCPA violation period and investigation period (see Figure 4).

Click to enlarge.

During audit engagements for clients with FCPA violations, auditors pay special attention to accounts such as payables and selling, general, and administrative expenses, which are more susceptible to FCPA risks. FCPA violators are also more likely to experience auditor changes than nonviolators, suggesting that auditors may remove themselves from client engagements with FCPA violations in response to the increased risk.

Employee morale: Human capital is an integral part of an organization’s strategic assets and contributes to an organization’s long-term growth and competitiveness. Therefore, it’s important to consider whether and how detection of corporate bribery may affect employees, especially their morale. George Serafeim, professor of business administration at Harvard Business School, in his 2014 working paper evaluated responses from a PwC survey. Managers were asked to assess the significance of the impact of bribery on multiple aspects of the organization. An overwhelming majority of managers identified employee morale as the most significant impact from corporate bribery.

Moreover, the impact of bribery on employee morale varies based on the identity of the initiator, the method of detection, and the organization’s response after detections. For example, bribery internally initiated by senior executives has a larger impact on employee morale because it signals a corporate culture that is tolerant of corrupt behavior, with the “tone at the top” failing to set a good example.

An organization’s subsequent remedial efforts such as self-detection of bribery and firing of key personnel involved could alleviate the negative impact to some extent. Given that low employee morale may subsequently lead to not only low employee productivity but also high employee turnover and labor force disruptions for an organization, the negative impact of bribery on employee morale, and thus organization competitiveness, is by no means trivial.

Relationships with customers and suppliers: As important stakeholders of an organization, customers and suppliers may be adversely affected by the organization’s involvement in foreign bribery and related FCPA enforcement action, causing damage to the relationships between the organization and its customers and suppliers. Customers may lose confidence in the organization due to concerns about the organization’s integrity and ethical behavior, leading to reduced demand for the organization’s products.

This is consistent with the findings of Elizabeth H. Creyer and William T. Ross Jr. in their research paper “The influence of firm behavior on purchase intention: do consumers really care about business ethics?” published in the Journal of Consumer Marketing. To quantify the reputational penalties associated with FCPA violations, researchers Vijay S. Sampath, Naomi A. Gardberg, and Noushi Rahman showed in their 2018 Journal of Business Ethics article that for publicly traded organizations investigated for FCPA violation, 81 cents of each dollar of market price decline was due to reputational penalties.

Suppliers may also question the organization’s integrity and effectiveness of internal control systems and perceive the organization as having higher business risks. This could result in an impaired relationship with the supplier, leading to decreased supplier responsiveness and weaker long-term financial performance for the organization, according to a 2004 Journal of Operations Management article. Taken together, damages to relationships with consumers and suppliers would result in lower future sales, higher cost of goods sold, and lower profitability for the FCPA-targeted organization.

Regulatory agency interactions: In addition to the negative effect on relationships with customers and suppliers, organizations also have to carefully manage their interactions with regulatory agencies such as the SEC, DOJ, Internal Revenue Service, and U.S. Environmental Protection Agency. An FCPA violation that results in an enforcement action from the SEC or DOJ puts the organization on the regulators’ radar, which likely attracts increased scrutiny from the regulators and increases the likelihood of future regulatory actions against the organization.

Moreover, FCPA investigations by the SEC or DOJ often reveal deficiencies and inappropriate conduct in other areas of the organization’s operations, which could trigger new enforcement actions.

Law professor Amy Westbrook points out that FCPA investigations often lead to a variety of collateral civil actions such as shareholder lawsuits and securities fraud class action suits. (See “Double Trouble: Collateral Shareholder Litigation Following Foreign Corrupt Practices Act Investigations,” Ohio State Law Journal, 2012.) The additional enforcement actions and collateral lawsuits associated with FCPA investigations can result in increased legal fees and expensive settlements.

THE RIPPLE EFFECT

In an era of heightened anticorruption enforcement, foreign bribery is becoming increasingly costly for organizations that operate in the global market. Foreign bribery and related enforcement actions create a ripple effect that extends to various aspects of the organization.

There are at least nine channels through which foreign bribery can have a significant impact on organization competitiveness. Aside from the monetary sanctions imposed by the enforcement authorities, FCPA-targeted organizations also face negative consequences related to increased professional fees; stock market reaction; downward analyst forecast revisions; higher cost of capital and auditing fees; employee morale; and relationships with customers, suppliers, and regulators. These costs can be substantial and aren’t often apparent to organizations engaged in FCPA violations. Moreover, these costs and consequences also apply to organizations that are subject to other anticorruption laws rather than the FCPA.

In the face of the increasing costs of foreign bribery, multinational organizations need to continually improve their FCPA compliance and risk management. Here are a few tips to achieve successful FCPA compliance:

- Evaluate corruption risks in your foreign markets.

- Evaluate corruption risks for your industry.

- Be aware of what can trigger an investigation.

- Self-report your potential violations.

- Engage professional services.

Table 1 contains a list of resources to help organizations evaluate their corruption risk in different markets and industry sectors.

Click to enlarge.

Overall, current conversations and events demonstrate the inherent, sometimes irreversible damage associated with foreign bribery. Managers of multinational organizations would do well to maintain a holistic view of the consequences related to foreign bribery and to stay on the right side of antibribery enforcement.

June 2021