After countless hours of studying and preparation, the moment has finally arrived: You’re taking the CMA® (Certified Management Accountant) exam. Whether you’re in a Prometric test center, at a computer in your own home being proctored remotely, or sitting for the Chinese language exam in a large hall filled with other CMA hopefuls, you find yourself reading the first question. You know how much time and effort you put into preparing for this moment. But how did that question in front of you get there? What goes into the making of the CMA exam itself?

The development of each multiple-choice or essay question on the CMA exam is a lengthy, detailed process involving the efforts of volunteers, independent contractors, vendors, and staff of ICMA® (Institute of Certified Management Accountants), which is an affiliate of IMA® (Institute of Management Accountants).

The ICMA Board of Regents is responsible for establishing the standards, policies, and procedures for determining the requirements for certification, administration and grading of the exam, and continuing professional development requirements. The board also ensures that the CMA exam upholds ICMA’s vision and mission statements (see “ICMA Vision and Mission Statements”), and, most crucial, it’s responsible for approving the content of the CMA exam.

So how does ICMA determine the content of the exam? Let’s start at the beginning.

JOB ANALYSIS STUDY

The exam development process begins with a job analysis study, which is the beginning of a two-year journey. In accordance with best practices, a job analysis study is conducted every four to six years to ensure that the CMA exam remains current and relevant. The purpose of the study is to validate the tasks and knowledge that are important for the practice of management accounting and competent performance by CMAs. Conducting a job analysis study is an involved process involving ICMA staff, assessment specialists, psychometricians, and volunteer subject matter experts.

The first step in developing the job analysis survey is to identify the tasks performed in a management accounting job and the knowledge needed to perform those tasks—and then to express that in statements. This work is done by a team of subject matter experts who spend considerable time reviewing and validating each statement. In the most recent job analysis conducted in 2018, the subject matter experts identified 73 task and 215 knowledge statements, which covered 12 exam domains.

Here are a few examples of task statements:

- Record accounting entries in accordance with International Financial Reporting Standards (IFRS), Generally Accepted Accounting Principles (GAAP), and/or local standards.

- Prepare external financial statements: balance sheet, income statement, equity statement, and cash flow statement including notes.

- Prepare schedules and analyses to support the preparation and/or audit of external financial statements.

Knowledge statements are specific categories and topics that a management accountant would need to have a firm awareness and understanding of, such as:

- Balance sheet.

- Risk identification and assessment.

- Ethical decision making.

The survey is sent to a representative group of management accountants. In the most recent job analysis conducted, more than 2,000 responses were received. Survey participants rated each task and knowledge statement (from 0 = of no importance to 4 = very important) and their current skill level (from 0 = unnecessary/not applicable to 4 = mastery).

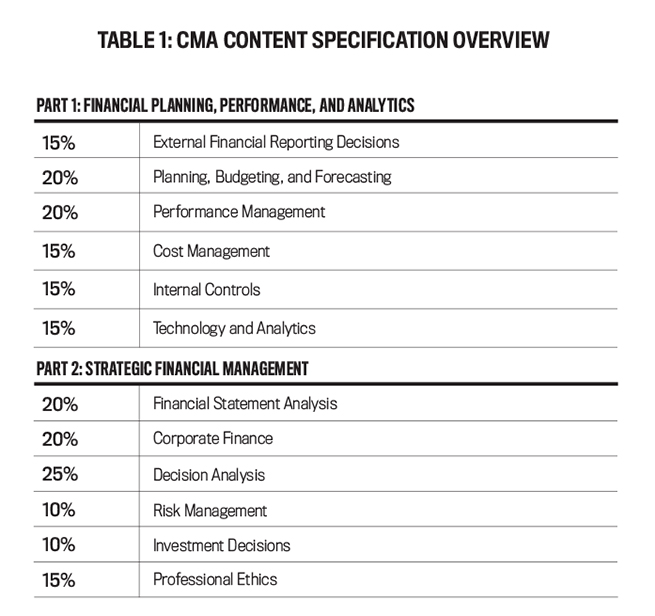

The results of the survey are compiled by ICMA’s testing vendor, Prometric, and then reviewed by members of the Board of Regents, who create the Content Specification Outlines that guide the development of the CMA exam and identify the topics covered by the exam (see Table 1).

From there, ICMA staff then develop the Learning Outcome Statements, which spell out what a CMA candidate is expected to know in each topic area. The Board of Regents reviews the Learning Outcome Statements and provides feedback. Click here for more on the Content Specification Outlines and Learning Outcome Statements.

The most recent job analysis resulted in key changes to the exam content. New and emerging topics were added, and topics that were no longer deemed relevant to the profession were removed from the exam. For example, Part 1 was renamed Financial Planning, Performance, and Analytics to reflect the addition of a new Part 1 content domain called Technology and Analytics, an emerging topic in the management accounting profession. This change also resulted in the addition of four new subdomains: information systems, data governance, technology-enabled finance transformation, and data analytics, and a number of related topics. Additionally, integrated reporting was added, and internal auditing was removed from Part 1 of the exam.

Part 2 was also given a new title, Strategic Financial Management, and a new subdomain, business ethics. The topic of sustainability and social responsibility was added to the subdomain ethical considerations for the organization, while off-balance-sheet financing, bankruptcy, and tax implications of transfer pricing were removed from the exam.

The job analysis also identified shifts in the importance of various CMA exam domains. As a result, Planning, Budgeting, and Forecasting was reduced from 30% in Part 1 of the exam to 20% and Cost Management from 20% to 15%, while Technology and Analytics was added to represent 15%. For Part 2, Financial Statement Analysis was reduced from 25% to 20%, Decision Analysis was increased from 20% to 25%, Investment Decisions was reduced from 15% to 10%, and Professional Ethics was increased from 10% to 15%.

Any time changes like these are made to the exam, there will be a need for more questions and materials for the domains with increased coverage as well as for the new topics and domain. Questions covering removed topics will be retired.

EXAM QUESTION DEVELOPMENT

The goal of the exam is to be a valid assessment of management accounting competency. The development of the exam involves three assessment principles: validity, reliability, and fairness.

- Validity ensures that the exam tests what it’s intended to test;

- Reliability ensures that the exam is consistent and that candidates with the same level of knowledge will obtain similar results on the exam; and

- Fairness ensures that all candidates are treated fairly.

The first step in question development is engaging a team of contracted subject matter experts as well as ICMA staff to develop multiple-choice questions and essays. ICMA has a team of almost 60 question writers from Canada, China, Germany, India, Netherlands, the Philippines, Qatar, Saudi Arabia, Singapore, and the United States. It continually adds new writers to its team and provides assignments throughout the year. This process helps ensure that there’s a continuous pipeline of new questions to include on the CMA exam.

CMA question writers are subject matter experts in a variety of topic areas and are part of a diverse group of academics, professionals, CMA exam award winners, and others. Question writing assignments are carefully developed to capitalize on the individual question writer’s subject matter expertise in coordination with the subject matter needs of the CMA exam.

ICMA has a staff member dedicated to providing periodic training and feedback to CMA question writers, graders, and reviewers. This ensures that new questions being developed meet the needs and requirements for the exam. Writers also receive question-writing tips approximately once a month to help continuously improve the quality of their exam questions.

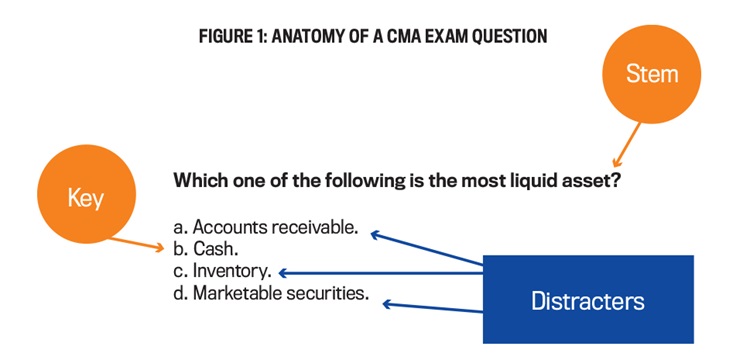

The initial training for question writers provides important information on the development of high-quality multiple-choice questions. Question writing is a technical form of writing, so training begins with the anatomy of an exam question (see Figure 1). Every multiple-choice question on the CMA exam consists of a stem, which asks a question; the correct answer, known as the key; and three incorrect—but plausible—answers, known as distracters.

To ensure the accuracy of the key, question writers are required to provide an authoritative reference (e.g., an authoritative textbook or an IMA Statement on Management Accounting) to support the correct answer.

Submissions from the question writers are reviewed carefully, and initial feedback is provided. The writer may be asked to make revisions. Once the writer makes a final submission, members of the question development staff edit and review the multiple-choice questions and reject those that don’t meet the CMA’s rigorous review criteria.

The criteria require that every question align with the Content Specification Outlines and the Learning Outcome Statements, and the questions are assigned a cognitive level, which represents the type of thinking needed to answer the question (see Figure 2). The questions must also be clear and comprehensible so candidates understand what they’re being asked. Questions should be free from bias and sensitivity issues.

After a question writer has mastered multiple-choice questions, they may be asked to write essays. Each essay consists of a scenario, which is known as the stimulus, and a series of related questions, which are known as prompts. This involves additional specialized training and ongoing feedback. Writers who are assigned to write essays also submit sample responses to help ensure that each prompt can be answered using the information provided in the stimulus. These sample responses are also reviewed and are provided to graders who read and score candidate responses.

Essays must meet the same rigorous criteria as multiple-choice questions. Each essay includes a scenario of about 250 to 350 words about a particular company or business situation. The scenario is followed by five to seven prompts. Each prompt must align with the Content Specification Outlines and Learning Outcome Statements and have an authoritative reference.

Essay prompts cover several topics and more than one domain. The scenario must be clear, concise, and realistic, and must not require industry-specific knowledge. The associated prompts let candidates know what they need to do, so it’s important for candidates to read the prompts carefully to be sure they know what’s expected of them and how to answer each prompt. The following are sample essay prompts:

- Calculate the company’s fixed overhead spending variance. Show your calculations.

- Identify and explain two factors affecting cash inflows and two factors affecting cash outflows at the company.

- Based on financial considerations, explain which one of the three alternatives the team should recommend.

SECOND REVIEW

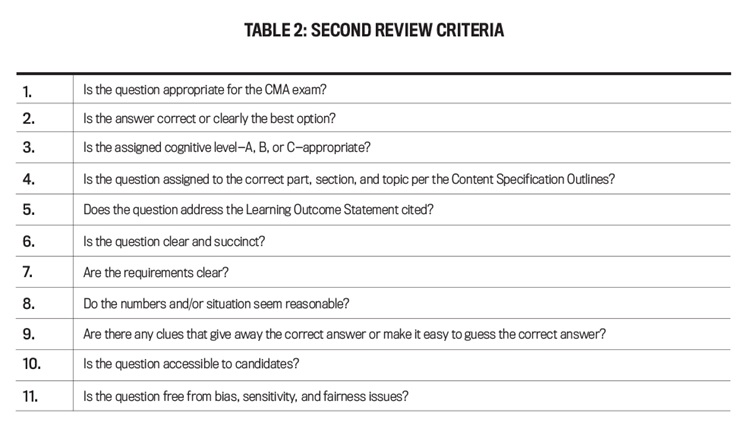

After the multiple-choice questions and essays are reviewed and edited by ICMA staff, a second review is conducted by teams consisting of members of the Board of Regents and the Exam Review Committee. The members of the Exam Review Committee are professional and academic IMA members who are management accounting subject matter experts. The teams consider a number of criteria in their review (see Table 2).

At this point, a final decision is made on the suitability of a multiple-choice question or essay for the exam. Those that are accepted can then be included on the English or Chinese CMA exam.

Once the review process is completed, question writers are provided with feedback on questions that weren’t accepted. The practice of providing feedback helps and improves the acceptance level for question writers and has enhanced the overall quality of multiple-choice questions and essay submissions.

TESTING THE QUESTIONS

There’s a continuous need for new questions for the Chinese language and English exams to ensure the exams remain robust and rigorous. The Chinese language CMA exam is delivered three times per year, generally in April, July, and November, in a paper-based format. Because of how the test is delivered, it’s necessary to build three versions of Part 1 and three versions of Part 2 every year. That requires 600 multiple-choice questions annually. ICMA staff painstakingly build these six versions throughout the year. They need to ensure that each version is balanced and that the number of questions in each domain reflects the percentage weight of the domain as defined in the Content Specification Outlines. For example, the External Financial Reporting Decisions domain represents 15% of Part 1, so of the 100 questions in Part 1, 15 must come from this domain.

The English exam is offered during three testing windows—January/February, May/June, and September/October—and delivered via computer-based testing at a Prometric test center or through remote proctoring. The exam is built using linear-on-the-fly testing (LOFT). This means that each candidate takes a unique—but comparable—version of the exam. LOFT delivers questions in each domain in accordance with the domain’s percentage as per the Content Specification Outlines.

When a question first appears in the exam, it isn’t scored and doesn’t actually impact test takers’ results. Rather, it’s included to test the question itself. After each exam window, Prometric provides key statistics on the performance of individual multiple-choice questions, such as the p-value and the point-biserial correlation. The p-value reports how many people answered a question correctly and is an indication of difficulty level. The point-biserial correlation tells the relationship between how well a candidate performed on an individual test question vs. how well they performed on the exam as a whole.

This information is used to determine whether any new, unscored questions should be included in the exam as scored questions or if they don’t meet requirements and should be removed. This statistical assessment continues even after a question is scored, helping to determine if it should continue to remain part of the exam.

This constant cycle of new questions and performance assessment helps ensure the exam content is relevant, refreshed, and consistent. Candidates don’t receive the same test, but they all receive an exam that has the same level of rigor and subject matter knowledge. By successfully completing the exam, candidates demonstrate their mastery of the CMA content. This content as confirmed by the job analysis is critical to a CMA’s performance in the management accounting and finance professions. The candidate is now ready to take the next steps to CMA certification.

AFTER THE EXAM

Now you know how the questions got there, but you aren’t finished yet. Once you complete the exam, there are a few more steps before you can call yourself a CMA. First is the essay grading.

The essays for both the English and Chinese language exams are graded by a team of talented and experienced graders. For multiple-choice questions, the English exam is graded via an online grading system, and the Chinese language exam is graded in person in IMA’s Beijing office. The grading is carefully monitored and checked for consistency and accuracy by independent reviewers and ICMA staff.

Once the grading is complete, the essay grades and multiple-choice question grades are combined by Prometric into a final grade. For the English exam, grades are sent to candidates approximately six weeks after the end of the month they tested in. For example, candidates who test in May will receive their grades around mid-July, and candidates who test in June will receive their grades around mid-August. It’s the same for the Chinese language exam: Grades are sent out approximately six weeks after the testing event.

Second, within seven years after passing both parts of the CMA exam, candidates must meet the educational and experience requirement. To meet the education requirement, candidates must submit verification that they hold a bachelor’s degree from an accredited college or university or hold a professional certification approved by ICMA. The experience requirement entails that the candidates complete two continuous years of professional experience in management accounting and/or financial management.

After passing the exams, candidates are required to complete 30 hours of continuing education annually, including two hours of ethics—even if they haven’t been certified yet. When the education and experience requirements are met, the CMA certification will be awarded. Completing 30 hours per year of continuing professional education ensures that CMAs remain current in the competencies required by the management accounting and finance professions.

This whole process, from the job analysis to continuing education requirements, ensures that holding the CMA certification demonstrates an individual’s commitment to professional excellence and a mastery of the competencies required to be a key member of accounting or finance teams. The CMA is a recognition of the hard work, dedication, time, and effort it took to achieve the certification, and it will make you stand out among your peers. It’s an honor well-earned.

June 2022