This new annual award is named in memory of Curtis C. Verschoor, a longtime member of the IMA Committee on Ethics, editor of the Strategic Finance Ethics column for 20 years, and a significant contributor to the development and revisions of the IMA Statement of Ethical Professional Practice. Curt was a passionate, renowned thought leader on ethics in accounting, having earned a Lifetime Achievement Award from Trust Across America—Trust Around the World for his leadership in and advocacy for trustworthy business practices.

The Curt Verschoor Ethics Feature of the Year highlights an article that focuses on the importance of ethics in business as a whole and finance and accounting in particular—issues that Curt deeply cared about.

THE VALUE OF TRUST

Curtis C. Verschoor, a respected champion in the field of ethics, often wrote about the alarming trend of declining trust that institutions are experiencing in many parts of the world. In the United States, for example, the 2018 Edelman Trust Barometer revealed some shocking data on changes in perceptions of trust.

For example, in the U.S. between November 2016 and November 2017, the composite global trust index—a combination of trust in business, government, nongovernment organizations (NGOs), and media—dropped from 68 (among the very best in the world) to 45 (last in the world). The decline of 23 points in one year was the largest single-year change in trust for any country in the history of the Edelman Trust Barometer by a factor of two times.

Undoubtedly, this precipitous decline is related to such matters as seemingly endless reports of corporate fraud, political scandal, and what some have coined “fake news.” As Richard Edelman, president and CEO of Edelman, noted, “The United States is enduring an unprecedented crisis of trust….The root cause of this fall is the lack of objective facts and rational discourse.”

The problem is thus much more than just an interesting subject of conversation—for Americans, it has indeed become something of a crisis of faith.

To get a clearer understanding of the trust deficit and to identify appropriate remedies for management accountants and other financial professionals, we surveyed and interviewed a number of notable and highly respected “trust” experts. We asked them about the kinds of trust issues that accounting and finance professionals will likely need to consider when managing their careers, the practical implications of these issues, and how individuals and organizations can assess and improve their own trust-building skills.

THE IMPORTANCE AND BENEFITS OF TRUST

Research clearly indicates that trust is, in fact, inherently and absolutely essential to the proper functioning and sustainability of an organization and to individual career success. For example, Bart DeJong, Kurt Dirks, and Nicole Gillespie analyzed the findings from 112 independent studies and concluded that there’s a positive relationship between the achievement of trust and high performance. (For more, see their article, “Trust and Team Performance: A Meta-Analysis of Main Effects, Moderators, and Covariates,” Journal of Applied Psychology, vol. 101, no. 8, August 2016.)

Additionally, according to a Watson Wyatt Human Capital study, which serves to quantify the link between effective human capital management and a company’s financial performance, high-trust organizations achieved a total return over a five-year period that was nearly three times higher than that experienced by low-trust organizations. Most recently, the 2019 Edelman Trust Barometer Global Report, an online survey of more than 33,000 members of the general public, found that building trust with customers is also of critical importance, with 67% agreeing that “a good reputation may get me to try a product, but unless I come to trust the company behind the product, I will soon stop buying it” (bit.ly/2ScRakU).

Verschoor may have understood this better than anyone else. As the editor of the Strategic Finance Ethics column, he often wrote about the important role trust serves in organizational performance and the career success of financial professionals. In his January 2017 column, “Trust as a Constant”, he stated, “Though just about all aspects of business may shift over the course of decades, one thing remains the same: the need for an atmosphere of trust in the workplace.” He goes on to report the findings from advocacy group Trust Across America—Trust Around the World that indicate trust in organizations leads to timelier and less costly decision making, higher employee engagement and retention rates, improved levels of innovation, and increased profitability.

Verschoor’s important observations and findings were further reflected in his May 2017 column, “Trust in Institutions is Eroding”, which spoke to the 2017 Edelman Trust Barometer survey that reflected a decline in the general population’s trust in all four institutional groups (business, government, NGOs, and the media). Verschoor noted that “academic research studies have shown that good ethics (specifically, an environment of trust) lead to lower costs and higher revenues and profits.”

Not surprisingly, Verschoor’s findings are supported by other experts’ research. In his article “How the Best Leaders Build Trust”, Stephen M.R. Covey provided an eye-opening example of how high-trust organizations increase speed and reduce costs:

Consider the example of Warren Buffett—CEO of Berkshire Hathaway (and generally considered one of the most trusted leaders in the world)—who completed a major acquisition of McLane Distribution (a $23 billion company) from Wal-Mart. As public companies, both Berkshire Hathaway and Wal-Mart are subject to all kinds of market and regulatory scrutiny. Typically, a merger of this size would take several months to complete and cost several million dollars to pay for accountants, auditors, and attorneys to verify and validate all kinds of information. But in this instance, because both parties operated with high trust, the deal was made with one two-hour meeting and a handshake. In less than a month, it was completed. High trust, high speed, low cost.

LOOKING INWARD

The value of trust to the success of an organization seems abundantly clear, but what about its significance to the success of individuals within the organization? Trust is, of course, essential to establish credibility, which most people realize is paramount to achieving true “success.”

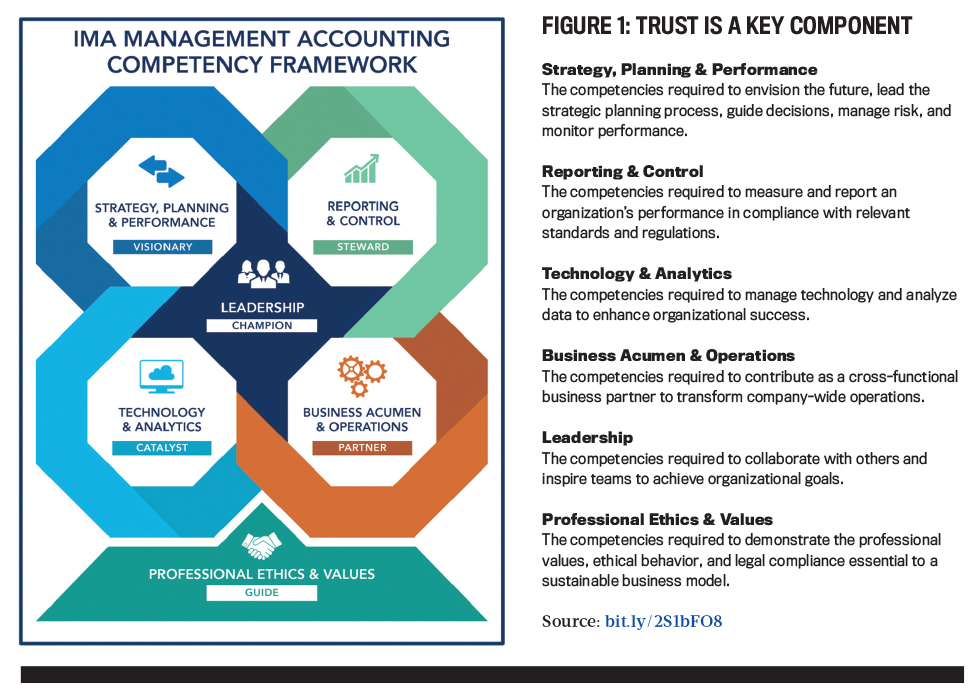

Accountants and other financial professionals are no exception. The 2019 IMA® (Institute of Management Accounting) Management Accounting Competency Framework (see Figure 1) identifies “six domains of core knowledge, skills, and abilities that finance and accounting professionals need to remain relevant in the Digital Age and perform their current and future roles effectively.” Indeed, trust is described in two of IMA’s six domains: Leadership and Professional Ethics & Values.

The Leadership domain includes collaboration, teamwork, and relationship management and states that financial professionals need to “work effectively with others in order to achieve a trusting relationship that yields positive results.” Communication skills are a huge part of this domain as well. In fact, we’ve found that “building trust” ranks high in importance as a dimension of communications skills at each career level—supervisory staff, manager, executive, and so on. Thus, in order for a financial professional to maintain success throughout his or her career, the establishment of trust is essential. (For more on this topic, see Douglas M. Boyle, Brian W. Carpenter, and Daniel P. Mahoney, “Developing the Communication Skills Required for Sustainable Career Success,” Management Accounting Quarterly, Fall 2017.)

The Framework goes further in the Professional Ethics & Values domain by pointing toward the need for financial professionals to “understand the importance of trustworthy behavior.” Consistent with this idea are the observations that Jolene Lampton made in “The Trust Gap in Organizations” (Strategic Finance, December 2017, in which she identified four key elements of trust: fairness, honest communications, leaders who do and mean what they say, and follow-through.

Lampton also offered questions that leaders should ask themselves to help achieve ethics renewal within their organization, including:

- Are you increasing your own integrity?

- Do you genuinely try to be honest in all dealings?

- Are you clear on your own values?

- Do you walk the talk, showing others that your intentions and/or purpose are authentic?

BARRETT’S TRUST MATRIX

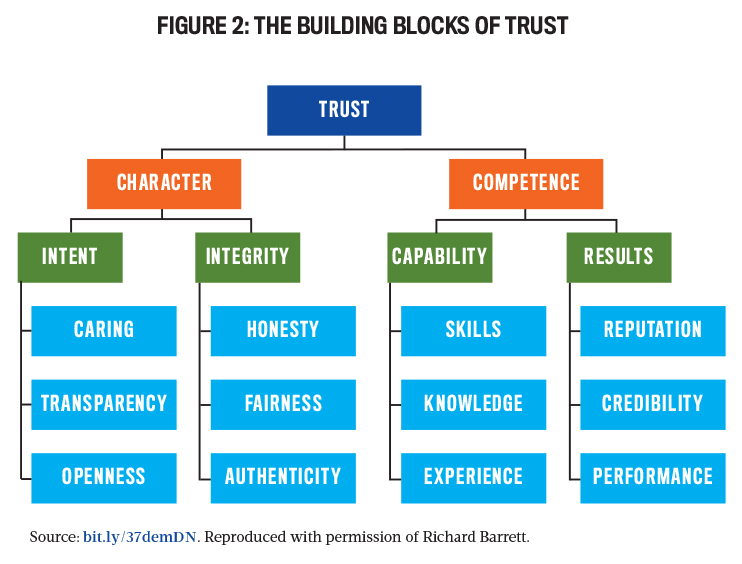

Given the importance of trust to both organizations and accounting and finance professionals, an obvious question to ask is: How can trust best be achieved? A widely recognized model to understand the concept and elements of trust is Richard Barrett’s Trust Matrix. In “The Trust Matrix,” Barrett states, “To build a strong team there must be a high level of trust. Trust is the glue that holds people together.” He adds that “trust increases the speed at which the group is able to accomplish tasks and takes bureaucracy out of communication.”

Barrett’s Trust Matrix shows that the two principle components of trust are character and competence (see Figure 2). “Character” refers to intent and integrity, which depend on the individual’s emotional and social intelligence. Character is required for bonding and takes time and effort to develop. “Competence,” on the other hand, refers to capability and results, which depend on the individual’s mental intelligence, education, and professional learning.

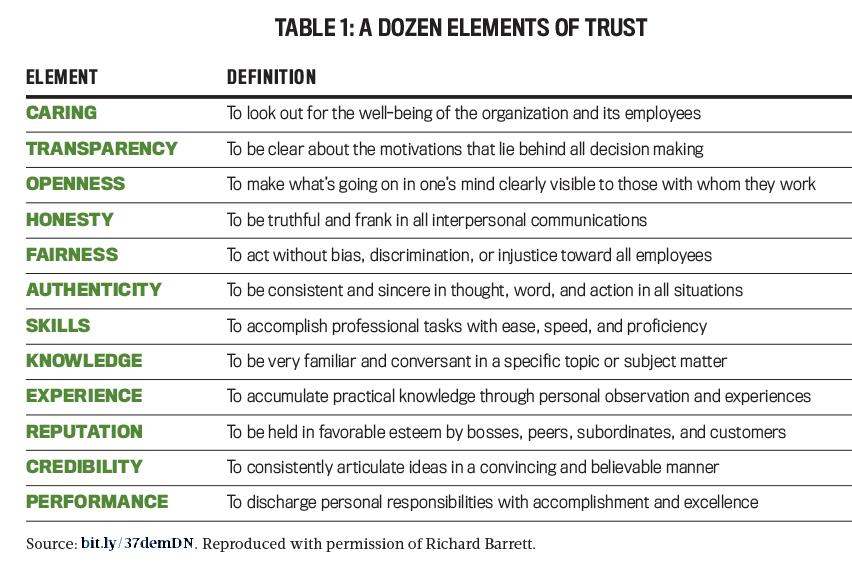

In summary, “trust” consists of two principal components (character and competency), four traits (intent, integrity, capability, and results), and 12 elements (caring, transparency, openness, honesty, fairness, authenticity, skills, knowledge, experience, reputation, credibility, and performance), which are defined in Table 1.

Click to enlarge

Click to enlarge

INSIGHTS FROM TRUST EXPERTS

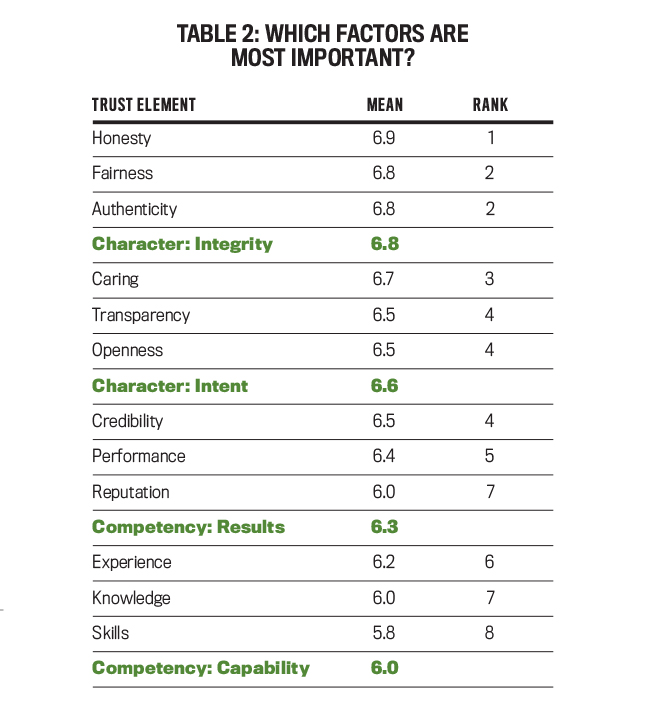

To help provide greater insight into the 12 trust elements in Barrett’s matrix, we partnered with TRUST! Magazine—published by Trust Across America—to ask 36 recipients of the organization’s Lifetime Achievement Award to rank the relative importance of the elements. (Each of the survey respondents is highly skilled, with more than 20 years of professional experience, and together represent a broad range of industries.) They were also asked to respond to open-ended questions dealing with the issue of trust (see “The Experts Weigh In” at end of article).

Table 2 presents the survey participants’ ranked ordering of the trust elements and the respective mean rating (on a seven-point scale, with 1 = not important and 7 = very important) of each element with regard to the development of a trustworthy accounting or finance professional.

While all elements were rated as “important” (with the lowest rating, 5.8, going to skills), the character elements were deemed to be of greatest importance, with means of 6.8 and 6.6, respectively, for integrity and intent. This finding compares with means of 6.3 and 6.0, respectively, for results and capability. The rankings suggest that while the competency trust component, which emphasizes producing results and acquiring capability, is essential, it’s in fact the character trust component that management accountants and other financial professionals should give priority to in their efforts to develop trust. Why is this finding important? Because most professional development and continuing professional education (CPE) requirements focus primarily on the attainment of competency skills, whereas this finding points more toward the need to develop character-building traits.

THE BOTTOM LINE

Several noteworthy conclusions can be gleaned from our analysis. First, it seems clear that those entities that can be labeled “high-trust organizations” realize a trust dividend of high speed and low cost, while low-trust organizations incur a “trust tax” of low speed and high cost. While this finding should be of interest to financial professionals, it shouldn’t come as a surprise given that the IMA Management Accounting Competency Framework identifies “building and maintaining trust” as an important factor in two of its six domains of core knowledge, skills, and abilities that finance and accounting professionals need in order to succeed both now and in the future.

In terms of character traits, we found that all six—honesty, fairness, authenticity, caring, transparency, and openness—are essential. Therefore, organizations might (perhaps through their human resources component) develop in-house seminars that focus not just on the development and continuous strengthening of these traits, but also on the absolute necessity of such ongoing “conditioning” as a requirement of continued employment. Barrett’s Trust Matrix would be an outstanding foundation on which organizations can develop these seminars, webinars, and the like.

Any individual and organizational efforts aimed at fortifying trust should also, as revealed by our study, focus on the continuous improvement of competency traits. More specifically, reputation, credibility, performance, knowledge, and experience are found to be significant determinants of trust. Here again, continuing education seminars or webinars, as well as personal development classes, can prove instrumental to providing accounting and finance professionals with the attributes that are essential to the truest form of success.

It’s no surprise that trust is a critical component of successful careers. What matters most, therefore, is that you’re able to identify the specific factors that can best enhance the level of trust with which you are perceived within and outside of your organization. To paraphrase the legendary Curt Verschoor, the risks of engaging in untrustworthy behavior are as high as the rewards of engaging in trustworthy behavior. So take the long-term view with regard to trust. You’ll be glad you did.

THE EXPERTS WEIGH IN

In order to gain further insight into the results of our survey, we conducted interviews with Trust Across America-Trust Around the World Lifetime Achievement Award recipients Donna Boehme (principal at Compliance Strategists LLC), Barbara Brooks Kimmel (CEO and cofounder of Trust Across America), David Reiling (CEO of Sunrise Banks), Jeffrey Thomson (president and CEO of IMA), the late Curtis Verschoor (founding member of IMA’s Committee on Ethics), and Robert Whipple (“The Trust Ambassador” and CEO of Leadergrow Inc.).

When you think of “trust” within a business context, what does it mean to you? Thomson: Trust is so foundational to business success that without it nothing else follows in accomplishing strategic goals and serving the public interest. It’s part of the “golden thread” to being successful.

Whipple: Trust is the most essential ingredient for business success; without trust, organizations battle gremlins on every front and eventually fail.

Boehme: It’s the essential element of trust that bridges the divide among individuals, teams, and leaders and breaks down barriers and silos. Trust fuels a workplace in which individuals and teams can and do cooperate and collaborate to achieve great success and results.

Verschoor: It is the confidence that the associated person or counterparty will perform as they have promised.

In considering your own personal experiences with corporate financial leaders, what are some examples of situations in which you applied Barrett’s Trust Matrix? Reiling: When facing organizational change, the combination of the Trust Matrix elements is key to success. First, transparency and credibility are key to effective communication during times of change. Whether positive or negative, I have seen firsthand the effect that transparency from a trusted leader can have on organizational change. For example, when we faced gaps in staffing, I was able to trust that my team would be able to fill in and pick up the slack. They exhibited the elements of caring and experience together to make sure that we continued down a path to success.

Thomson: All 12 elements are important. Caring is critically important to IMA’s core values. Also important are skills. If I’m going to trust you, then I also must trust your competence.

Within the list of skills that are essential to a financial professional, where should trust rank? Thomson: Trust does not rank among skills but is foundational. Trust is absolute: I either trust you or I do not, and if I do not trust you then you should not be part of the organization.

Whipple: Trust is the bond that holds everything together and is the foundation to the other skills.

Kimmel: Regardless of the profession, trust should rank at the top.

Reiling: Many of the skills can be learned at any point in a career. Trust, on the other hand, takes time to foster and requires constant care to maintain. Rebuilding trust when it’s lost or neglected is incredibly difficult.

What specific benefits does a trustworthy financial professional bring to an organization? Boehme: Organizations with high levels of trust and ethical leadership protect their reputation and brand in the marketplace and avoid finding themselves in the prosecutor’s crosshairs or in scandal headlines.

Thomson: Trustworthy financial professionals provide not just the information that I want to see, but also the information that I need to see.

Kimmel: Regardless of the profession, and in its simplest form, a trustworthy individual brings character, competence, and consistency to the organization.

What’s the most critical advice that you can give to a financial professional with respect to building their own level of trust? Reiling: Be authentic. Make sure you’re listening to the needs of not only your clients but also your team. People will know when you’re serving your own interests over theirs. Work to learn the specific needs of the people you work with every day and make a direct effort to match your needs and values to theirs. This alignment creates an environment where success comes naturally.

Whipple: Learn to create a safe environment where individuals can share their beliefs without fear of retribution.

March 2020