As we explored DE&I in specific regions (see “Diversifying Global Accounting Talent”), we found that, although improvement in diversity is needed across the globe, and particularly in senior leadership roles, any progress made around DE&I isn’t sustainable without persons of all backgrounds feeling welcome, accepted, and included in the profession: The profession must foster a culture of belonging.

Click to enlarge.

Belonging is the outcome of inclusion and a by-product of equality. Yet the negative effects of bias on employee interaction, engagement, and talent management pose challenges to the prospect of inclusion. Further, systemic disparities, such as unequal access to quality education, gender discrimination, or limited economic investment in disadvantaged communities, inhibit access to opportunities for members of certain demographic groups, creating an environment in which sameness of treatment (equality) doesn’t consistently result in proportional fairness (equity).

Thus, to determine how the profession can achieve a sustainable culture of belonging, we sought to present overarching catalysts for action that transcend geography; share actionable practices and metrics that can be employed by accounting and finance leaders along any point in the talent pipeline; and spark an increase in organized, collaborative action among professional accountancy organizations (PAOs), public accounting firms, academics, standard-setting bodies, and other members of the accounting profession’s ecosystem.

CATALYSTS FOR ACTION

Advances in digital technology and the expanded use of social media outlets have greatly increased visibility of social intolerance, discrimination, and inequitable treatment across the globe. The corresponding heightened awareness has prompted or exacerbated civil unrest in several countries. Research has shown that marginalized or underrepresented groups within many business disciplines, including the global accounting profession, are more likely to experience microaggressions and subtle bias than overt, blatant discrimination.

Interviews with more than 100 members of the global accounting profession and analysis of more than 8,500 survey responses reveal that these manifestations of inequitable practices, unfair treatment, and exclusive behavior yield several areas of concern: lower employee morale, increased turnover, inhibited growth of the profession’s talent pipeline, and undermining of the ability to deliver value to accountants in the future.

Our research identified three key catalysts for action among all focus regions:

- The current state of DE&I in accountancy (including some progress toward equality but also underrepresentation of certain demographic groups and a lack of equity and inclusion),

- The responsibility to protect the public interest, and

- Demands for sustainable business information around DE&I.

THE STATE OF DE&I IN ACCOUNTING AND FINANCE

Given the increased social awareness and improved understanding of DE&I matters today, the accounting and finance profession has been dedicating more resources to identifying, designing, and implementing solutions that effect expansive change. A key contribution to that effort is this collaborative research study. Findings of this research will help to improve the understanding not only of the drivers of DE&I, but of how to overcome challenges and improve the profession’s performance around DE&I issues. To enable tailoring of actionable solutions that address DE&I challenges facing the profession today, we present three key findings from our analysis of the current state of DE&I in accounting and finance.

A diversity gap. Based upon our analysis of demographic workforce and population statistics and a comparison of self-reported job titles denoting seniority, we identified what we’ve characterized as a diversity gap between senior leadership of the profession and the whole of the accounting and finance workforce (i.e., greater diversity across the profession than in leadership positions). The diversity gap also exists in the U.S. between the profession and the U.S. population for certain racial and ethnic groups. (Note: Comparable workforce statistics for the profession were not readily available across all jurisdictions.)

Sentiments toward equity and inclusion. Fewer than 60% of respondents of all backgrounds view the profession as equitable or inclusive (57%). A closer look at the individual studies reveals respondents from the U.S. and Europe are less likely to view the profession as equitable or inclusive than those in Asia-Pacific or the Middle East and North Africa. On average, male respondents are more likely than females to view the profession as equitable and inclusive.

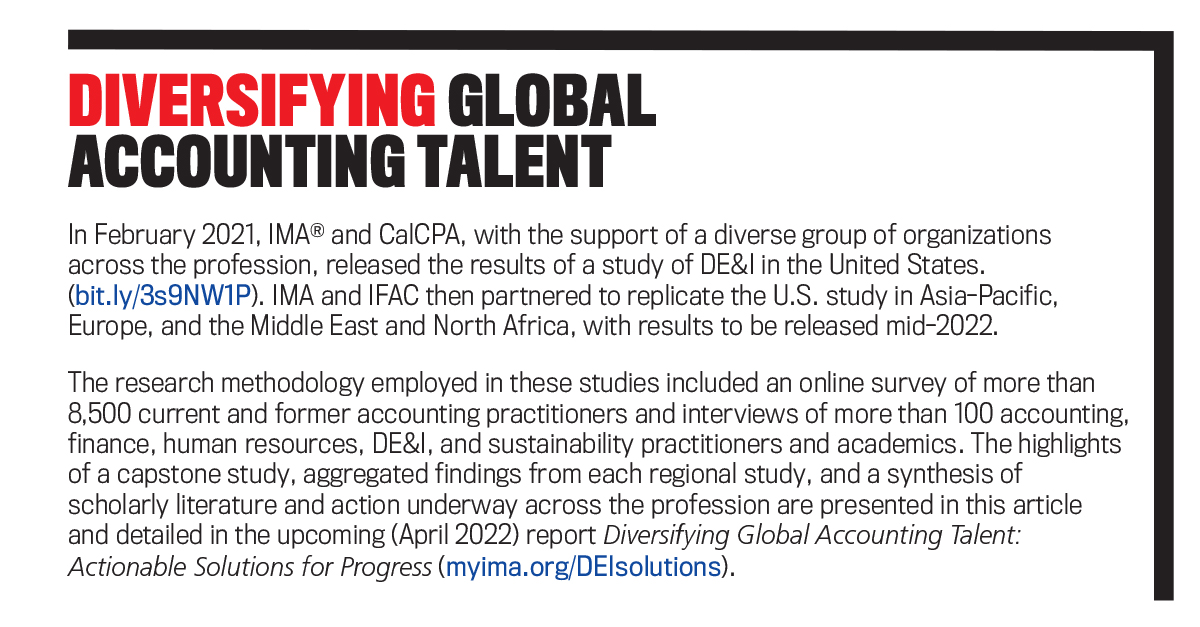

Retention of diverse talent. Although each of the global studies addressed a unique combination of demographic groups, the female demographic segment was explored in each. Women and members of other diverse demographic groups of focus report they aren’t advancing in the profession because of inequity and exclusion. These individuals cite contemporary experiences of inequitable treatment and exclusive behaviors that have impacted career decisions and prompted some to leave the profession. Figure 1 illustrates that, on average, 41% of female respondents across all regions have left a company due to a perceived lack of equitable treatment or inclusion.

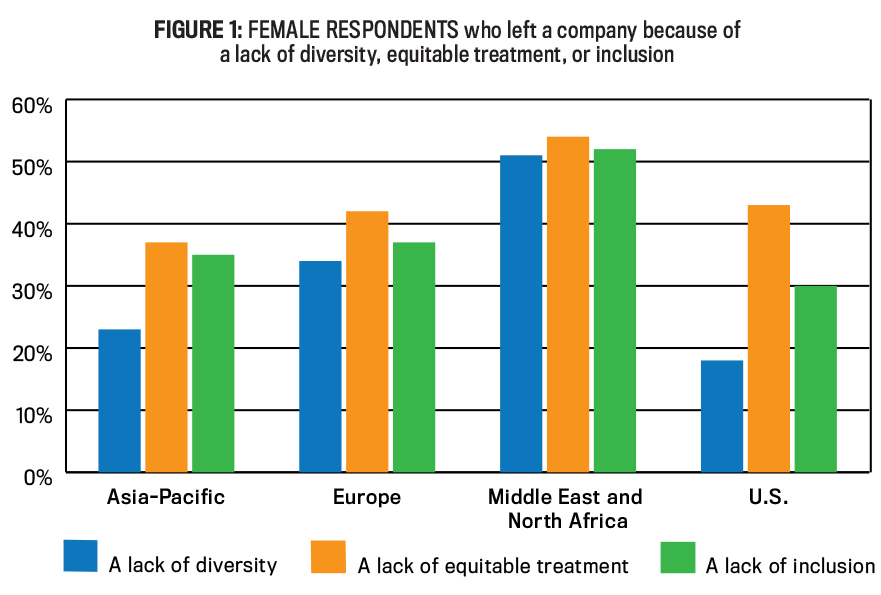

Of even greater concern, however, is that in addition to an average of 39% of female respondents reporting that these experiences impacted their career decisions, 11% of women across all regions indicate that inequitable and exclusive experiences contributed to their decision to leave the profession completely (see Figure 2). This is a significant number and one that should put all of us on notice that something must be done to curtail this loss of talent.

PROTECTING THE PUBLIC INTEREST

One of the central roles for accountants is to serve the public interest. This long-standing responsibility serves as a key impetus for the profession’s action toward DE&I progress. The International Code of Ethics for Professional Accountants (the Code) from the International Ethics Standards Board for Accountants (IESBA) sets out the fundamental principles of ethics to which all accountants must adhere: integrity, objectivity, professional competence and due care, confidentiality, and professional behavior.

These principles support workplace policies that promote openness, respect, and inclusion when interacting with individuals of all backgrounds. They also help mitigate the risk of bias affecting decisions and professional judgments. Organizations with ethical values that align to the Code’s fundamental principles nurture and support objective and fair recruitment and promotion practices.

A strong ethical culture enables the implementation of DE&I programs. Professional accountants, because of their role in fostering and maintaining an ethical culture, can make substantive contributions to the effective implementation of DE&I programs within their organizations, firms, and society at large. Under the Code, professional accountants are expected to encourage and promote an ethics-based culture within their organizations. To that end, beyond applicability to accountants’ treatment of other business professionals or how they conduct themselves personally, these obligations also extend to how accountants treat each other.

DEMANDS FOR DE&I METRICS, DISCLOSURES, AND REPORTING

A further extension of accountants’ well-established ethical obligation is the evolving role of accountancy that increasingly encompasses the reporting of sustainable business information, commonly referred to as ESG (environmental, social, and governance) reporting. With anticipated global sustainability standards forthcoming from the recently formed International Sustainability Standards Board, along with those included in frameworks such as that of the Global Reporting Initiative (GRI), accountants will play a central role in the process to gather, validate, and analyze ESG data, design internal controls, and communicate or report to management and external stakeholders.

Existing reporting standards and guidelines already require the disclosure of sustainable business information and performance metrics on human resources capital, including DE&I. Many governments, securities regulators, and accounting standard-setting bodies are already bringing attention and new mandates for organizational transparency, particularly around people in leadership roles.

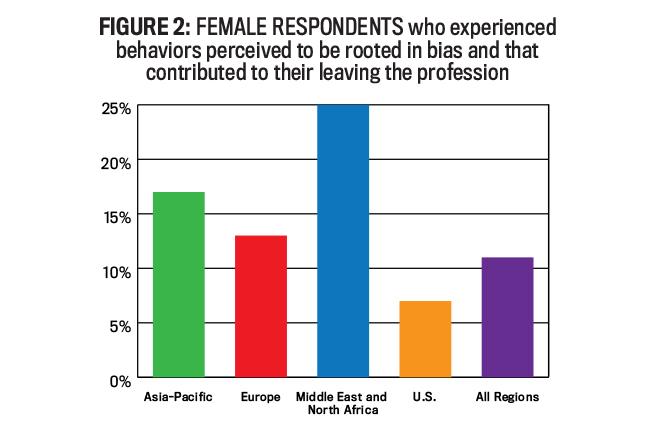

The part of this movement that focuses on the “social” aspect of ESG advances with the recognition that human capital—the contributions and value of people who make up a workforce—requires due attention and care in order for an enterprise to perform well, be more innovative, and create value. In acknowledgment, five of the United Nations’ 17 Sustainable Development Goals (SDGs) address DE&I-related matters (see Figure 3). Following good DE&I practices is a key element for making progress and realizing positive results. This includes elimination of bias (conscious or otherwise) that undermines or erodes the value of human capital.

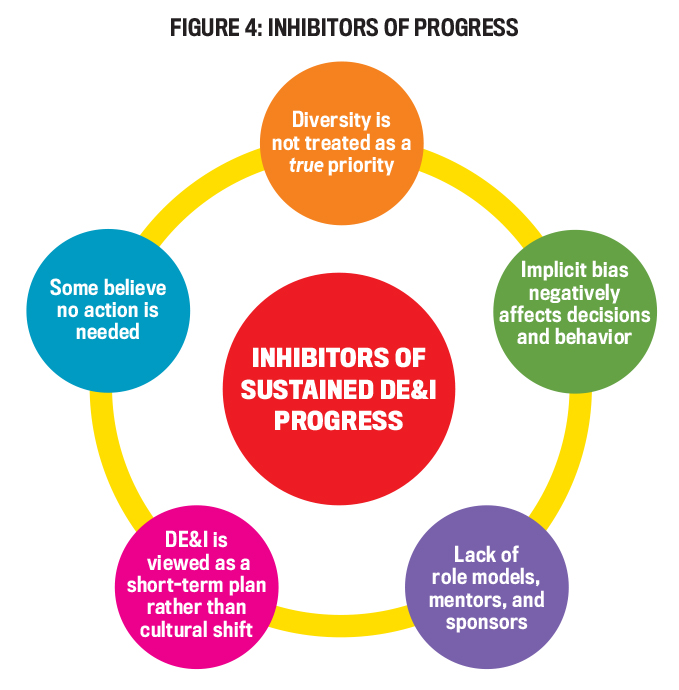

INHIBITORS OF PROGRESS

Recognizing that the catalysts for action have existed for years, even decades, many corporate, academic, and nonprofit institutions already have some form of DE&I-related strategies, policies, or initiatives in place. Yet as professors Frank Dobbin and Alexandra Kalev reported following analysis of three decades of data from more than 800 U.S. companies, “most diversity programs aren’t increasing diversity. Despite a few new bells and whistles, courtesy of Big Data, companies are basically doubling down on the same approaches they’ve used since the 1960s—which often make things worse, not better.” (For more information, see their article, “Why Diversity Programs Fail,” Harvard Business Review, July-August 2016.)

Consistent with Dobbin and Kalev’s findings in U.S. companies, more than 95% of interviewees in each of our regional studies indicated that, while working in the accounting profession, they witnessed DE&I programs that were unsuccessful or didn’t yield the amount of progress needed. Synthesis of these observations, coupled with those identified in a review of scholarly literature, revealed five key reasons DE&I efforts have been unsuccessful:

Diversity isn’t treated as a true priority. Diversity initiatives are sometimes treated as an “add-on.” Multiple study participants across all regions indicated that DE&I doesn’t consistently receive dedicated resources or defined key performance indicators for progress comparable to strategic operational or financial priorities. The research indicates that DE&I programs aren't consistently part of strategic goals and that DE&I improvement isn't often linked to leadership performance evaluations or executive compensation.

Implicit bias negatively affects decisions and behavior. Discrimination, or the effects of implicit bias (microaggressions and stereotypes), commonly manifests as unfair recruitment, promotion, and compensation practices that disadvantage members of underrepresented demographic groups.

There is a lack of role models, mentors, and sponsors for diverse talent. Role models have proven essential to introducing youth to the profession and to diverse talent’s career progression. Yet underrepresentation of females and members of other demographically diverse groups limits access to role models, mentors, or sponsors with whom current or future members of the profession can identify. While many organizations expend significant resources to recruit new talent, the research found that less effort is undertaken to retain diverse talent and ensure access to leadership ranks.

DE&I is viewed as a short-term plan rather than a long-term cultural shift. Often, diversity programs are stand-alone initiatives with plans developed for a finite period. This inhibits progress, as equity and inclusion improvements are achieved and sustained not by temporary initiatives but by long-term, genuine efforts to foster a culture of belonging, ensure equitable access to opportunities, and establish accountability for inequitable or discriminatory behavior.

Some believe no DE&I action is needed. While conducting each of the regional studies, a minority of study participants reported a belief that no further action is needed to enact DE&I progress across the profession. These perceptions, whether overt or concealed, negatively impact the success of even the best DE&I programs and the culture of the most well-intentioned organizations.

In the face of these inhibitors, efforts to raise awareness of the most effective DE&I strategies are required.

ACTIONABLE SOLUTIONS

The research for this series of studies identified a range of practices, programs, projects, and initiatives undertaken by numerous institutions throughout the various stages of the talent pipeline. Participants shared common means for improving DE&I, including mentorship programs, targeted recruitment strategies, internships, scholarships, training, grievance procedures, and affinity groups.

Scholarly literature also revealed DE&I practices that have proven effective at improving specific aspects of DE&I within an organization.

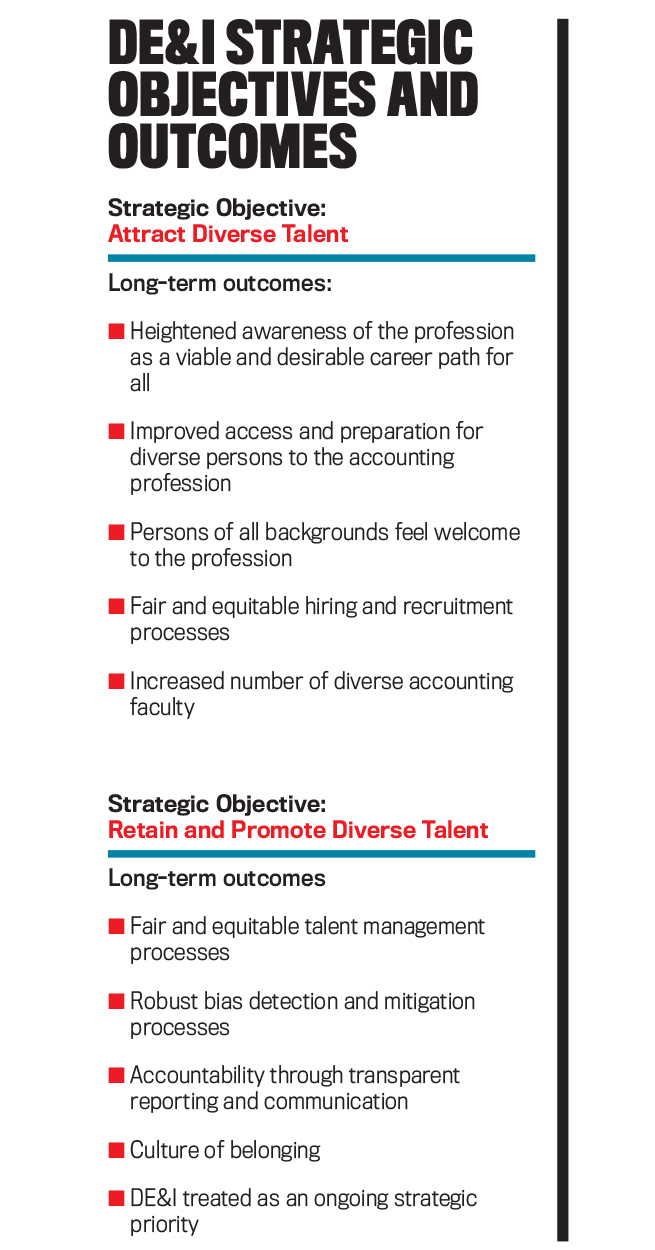

A synthesis of these findings yielded more than 60 specific and targeted actionable DE&I practices that have positive impacts or show promising results. We classified these actionable practices into one of two overarching categories that represent necessary strategic objectives for the accounting and finance profession’s DE&I efforts: (1) attract diverse talent and (2) retain and promote diverse talent. Specific long-term outcomes identified as essential to accomplishing these objectives are listed in “DE&I Strategic Objectives and Outcomes.”

The inventory of actionable practices isn’t meant to represent a comprehensive list of all good DE&I practices. Rather, the practices serve as actions that the profession, organizations, and even individuals can take to help achieve the stated DE&I strategic objectives and corresponding long-term outcomes. They serve as a catalyst for action and a resource to aid institutions and leaders in efforts to:

- Assess the effectiveness of existing DE&I initiatives,

- Bolster DE&I programs and agendas,

- Avoid inhibitors of DE&I progress,

- Measure progress toward DE&I goals,

- Align specific DE&I practices to the SDGs and other reporting standards, and

- Expand requirements for DE&I disclosure through proposed indicators.

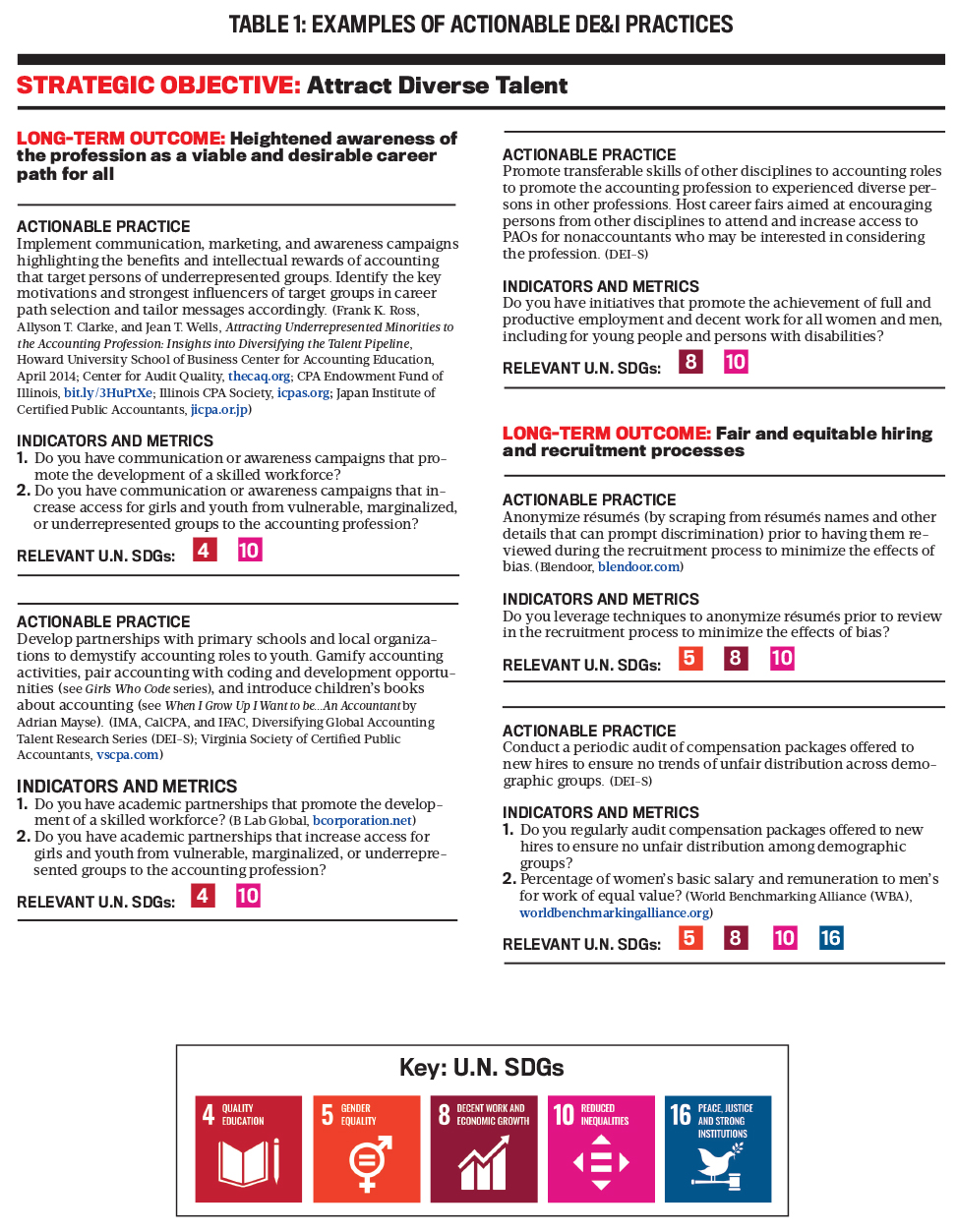

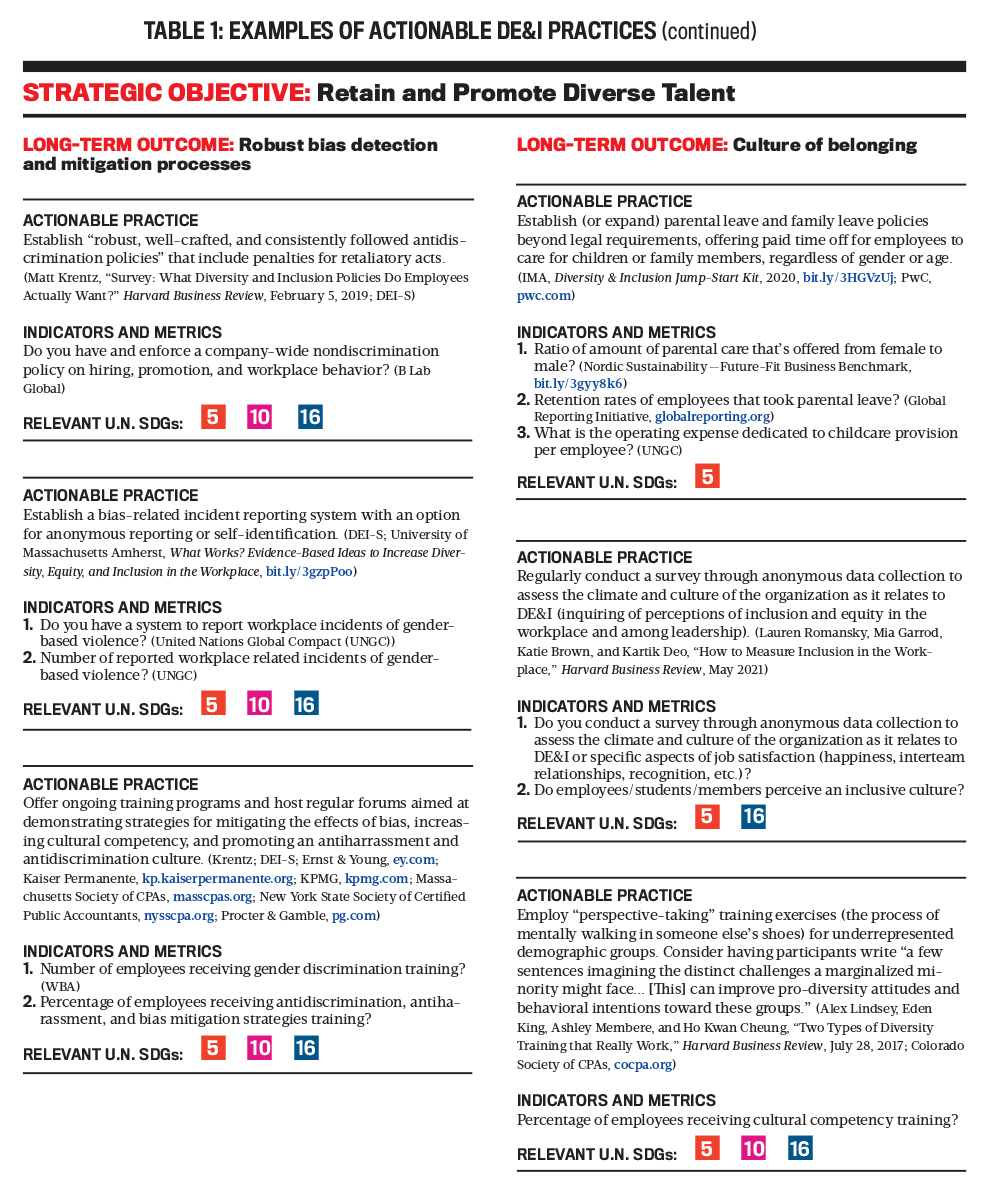

Each practice is grouped into the relevant strategic objective and linked to a long-term outcome. The inventory also includes suggested indicators and metrics, the relevant U.N. SDGs, and any original sources for the practices and proposed metrics. Table 1 presents some examples of practices for “heightened awareness of the profession as a viable and desirable career path for all,” “fair and equitable hiring and recruitment practices,” “robust bias detection and mitigation processes,” and “culture of belonging.” (Find the complete inventory in Diversifying Global Accounting Talent: Actionable Solutions for Progress at myima.org/DEIsolutions, to be published in late March/early April 2022.)

ENACTING CHANGE

Although some organizations have led robust DE&I improvement efforts for decades, many more accountancy organizations, firms, businesses, and academic departments have dedicated new and energetic efforts to DE&I initiatives since 2020. These expanded efforts are laudable steps in the right direction, but much of this activity reinforces existing practices that include limited or no accountability for progress, don’t yield the widespread results or sustainable change envisioned, or remain fragmented across the profession. The time for a change in approach is now. We must take bolder steps and challenge the status quo in an effort to do something different—and better—for the future of the profession.

Each member of the profession—students, academics, practitioners, PAO leaders, regulators, and standard setters—can enact change today. Where might you start? Review the actionable practices in the inventory and adopt those that you can implement as an individual. If you’re a leader, leverage your position to assess the effectiveness of your organization’s DE&I efforts, and then implement practices from the inventory most relevant to the structure and type of your institution. Partner with or support organizations with targeted efforts to improve access to the profession as well as inclusion and equity within the profession. We’ve done the research to get you started. This inventory is for you, your colleagues, and your management team.

The profession is clearly making progress around DE&I. Yet more needs to be done to coordinate and collaborate with collective purpose and perspective, to unite resources, and to join together with a singular vision for the outcome. We must work in unison toward a future for the profession where persons of all backgrounds have that sense of welcome, acceptance, and inclusion that comes with true belonging.

A Call for Collective Action

These research results serve as a wake-up call for the profession to take action. The future of accounting and finance rests not only on the shoulders of current and future leaders, but also with others who have a natural role as conveners and drivers of change. This includes professionals, students, academics, and professional associations. A collective effort is required to uproot the tendency toward legacy solutions that failed to achieve desired expansive results.

Effective solutions are needed to increase representation at all career levels, effectively measure DE&I progress, and enact coordinated, widespread improvement action across the profession. The time is now to effect change and unite the profession in a collaborative approach to solving what is a global issue. We are joined by dozens of organizations across the globe who are prepared to improve DE&I in the profession and serve as DE&I advocates. Together, we urge the profession to commit to take action and work together to enable and implement DE&I practices toward progress. We call on the profession’s leaders to join us in a commitment to drive change and ensure the long-term sustainability of a vibrant, diverse, inclusive, and equitable accounting and finance profession.

We’re united in what we’re asking for and prepared to achieve it. Are you?

Jeff Thomson, CMA, CSCA, CAE IMA President and CEO

Denise Froemming, CPA, CAE CalCPA President and CEO

Kevin Dancey, CPA IFAC CEO

Source: Excerpted from Diversifying Global Accounting Talent: Actionable Solutions for Progress.

March 2022