Knowing that uncertainty comes with the territory, multinationals contend with an array of external factors, internal considerations, and other forces that specifically influence budget policies, composition, and control. At a more general level, their strategic planning must reflect and respond to an increasingly uncertain business environment. As a management accountant or finance professional working in business, you’re likely well aware that budgeting in a global business setting calls for an enhanced level of coordination and communication because of the variety of powerful components that impact the organization’s performance.

This article is the first in a series of three that will examine budgeting for international operations. First, we’ll examine and portray how international issues influence the budgeting process of multinational companies that control foreign affiliates. The second article will deal further with the specific elements of budgeting during uncertain times, and we’ll close with an article on critical strategic planning considerations and components.

BUDGETARY PRESSURES

Three factors affect multinational budgets: foreign currency exchange rates, interest rates, and inflation. CFOs know they have no influence or control over this “Bermuda triangle” of outside forces. Nonetheless, these elements must be estimated, evaluated, and examined as part of a multinational’s strategic plan. They’re also interrelated—for example, higher inflation tends to drive down the value of a country’s currency, which impacts the exchange rate, whereas price inflation would drive up interest rates. While higher interest rates would attract more investors and increase the value of the local currency, changes in exchange rates have the most direct effect on the budgeting process for a multinational corporation.

Shifts in these three external factors stem from several sources, including economic conditions, government policies, monetary systems, and political risks. Each factor is a significant external variable affecting areas such as policy decisions, organizational procedures, and budget control. To minimize the possible negative impact of these factors, managers who work for multinational corporations must establish and implement policies and practices that recognize and respond to them. The presence of other external forces—such as political turmoil, competition, labor quality, and cultural or religious orientation—tends to be related specifically to one country or particular region of the world.

Unanticipated events can also impact multinational corporations, prompting them to focus on safety and security measures, employee counseling, and other special training that they probably hadn’t paid much attention to in the past. For example, in recent years, the occurrence of terrorist acts in various regions of the world has forced businesses to allocate more resources toward insurance and security measures. More recently, the social and economic fracturing resulting from the coronavirus pandemic calls for adjustments to otherwise normal corporate strategies and business plans. For an international organization to be successful, its budgeting must address all of these novel conditions.

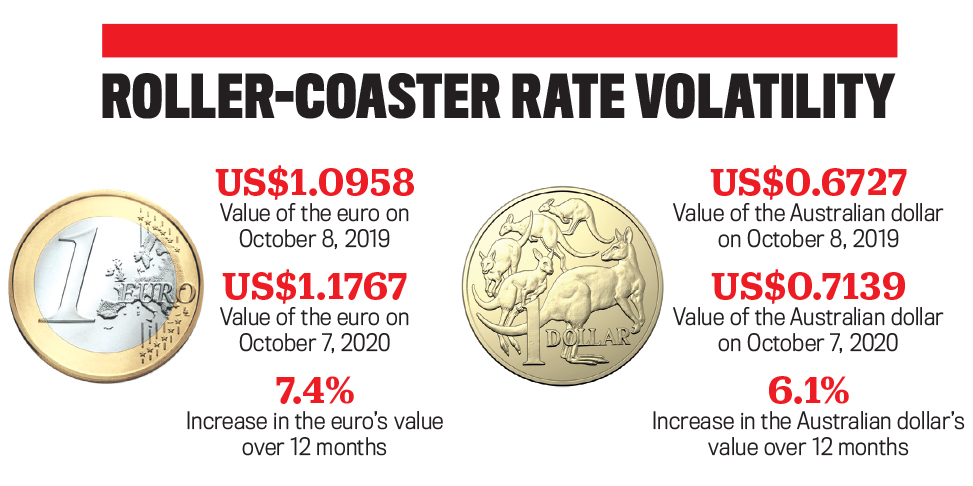

Multinational corporations must include their best estimates of future foreign exchange rates when preparing their annual and strategic budgets. This should be a key task of financial managers, given the volatility and uncertainty of foreign currency exchange rates in recent years (see “Roller-Coaster Rate Volatility”).

In addition, multinationals must closely observe the trends in international exchange rates, as these can potentially affect the business’s budgeting and performance. For example, in 2019 the Chinese government had put pressure to keep the yuan closer to, or lower than, the historical threshold of 1 U.S. dollar equivalent to 7 Chinese yuan. Consequently, the general strengthening of the dollar observed in 2019 was expected to negatively impact the trading position of U.S. exporters in the global marketplace.

Of all the factors influencing international budgeting, foreign exchange rates have the most significant and pervasive effect. Changes in foreign exchange rates are explained by different theories but essentially are based on the underlying demand for assets denominated in a particular currency. Foreign exchange rate fluctuations affect a multinational through translation exposure, transaction exposure, and economic exposure, each of which has a different effect on the entire budgeting process and on the strategic marketing and operating decisions of multinational corporations.

EFFECTS OF TRANSLATION EXPOSURE

Translation exposure influences financial statements during the development of a budget and/or while the budget is being used for control purposes. Specific exchange rates, usually based on forecasted values, must be determined and applied when preparing the budgeted financial statements from the applicable operation budgets.

So what’s the process that forward-thinking multinationals follow? First, when preparing budgetary data for financial statements denominated in foreign currencies, the accounting team begins by identifying the functional currency, which is the currency of the economic environment where the company operates. (For more, see FASB Accounting Standards Codification® (ASC) Topic 830, Foreign Currency Matters.) Thus, for a business operating in the U.S., the functional currency is assumed to be the U.S. dollar. For the foreign affiliates of U.S. companies, once the functional currency of the country where they operate is confirmed, their pro forma financial statements are translated into dollars at the expected exchange rates, as per the guidelines of ASC 830.

Later on, as operations proceed during the budgeted period, the actual exchange rates might vary from the anticipated exchange rates used in the budget, and those differences can generate unpredictable—and often uncontrollable—results during interim and final budget performance reviews. Because management can’t control shifting exchange rates, the effects of the fluctuations on the business’s profits can be removed from the budgeting control process by setting aside the variations due solely to changes between the budgeted and actual exchange rates. After removing these effects, however, there still may be some variances between the forecasted and actual budget, due in part to exchange rate movements that influenced taste trends or the preference for certain products in the marketplace.

Properly addressing translation exposure in international budgeting is very important, as its effects can influence: (1) the modification of pricing policies to compete with either higher- or lower-priced goods that aren’t produced in the same country, usually price-sensitive items such as consumer electronics, table wines, and textiles; (2) positive or negative changes in sales volume resulting from lower- or higher-priced competing goods and services either in a domestic or foreign market; and (3) deviations from standard input efficiencies because of alternate domestic or foreign suppliers who become more price competitive as a result of changes in the exchange rate.

If the effects of foreign exchange rate fluctuations for each individual transaction were removed, a specific exchange rate would need to be estimated for each and every revenue and expense category—a cumbersome, expensive, and time-consuming process. Instead, a more practical and accepted approach is to use expected average (monthly) exchange rates for the translation of the budgets of those foreign units. Average exchange rates are also permitted and used for the actual financial reporting, as per ASC 830.

ANOTHER CHALLENGE: TRANSACTION EXPOSURE

International transactions such as unhedged contracted cash flows that characterize international trade, repatriation of profits, and acquisition or disposal of foreign assets all come under the umbrella of transaction exposure. To compare the actual cash flows with the expected cash flows in a multinational corporation’s foreign units, accountants generally apply an expected future exchange rate. Because of transaction exposure risk, however, multinationals tend to hedge their international cash flows using two basic modes: (1) a “natural hedge” mechanism, such as pricing decisions, risk shifting, exposure netting, or currency risk-sharing, and (2) “an artificial hedge” that’s created with foreign exchange contracts or derivative hedging instruments, such as options, swaps, and futures. (For more on this topic, see Alan C. Shapiro’s Multinational Financial Management, 10th edition, John Wiley & Sons, 2014, pp. 292-307.)

Hedging involves additional transactions and expenses that must be recognized in the budgeting process. Corporate finance executives should develop a hedging policy as part of their strategic plan that identifies the minimum amount of cash flow to be hedged, the hedging methods to be employed, and the conditions for using such methods. Managers involved in planning cash flows should identify transactions that require hedging during the upcoming budget period. The potential gain or loss differential when foreign transactions occur and aren’t hedged could be significant (see “The Cost to Foreign Competitors”), so companies are wise to cover the risk of exchange-rate fluctuations through hedging.

Click to enlarge.

Click to enlarge.

If the volume of international cash flows is significant, some multinational corporations create a separate budget that will help to facilitate planning, controlling, and evaluating hedging activities and policies that are included in the organization’s strategic plan. Finally, hedging expenses should be included in the other income and expenses budget, as prescribed by ASC 815-30 and 815-35.

FACTORING IN ECONOMIC EXPOSURE

A third impact of foreign exchange rate variations is uncontracted future cash flows from foreign operations or investments. This is considered “economic exposure” and requires policy decisions important to the budgeting process. As such, strategic planning activities should consider policy decisions that are covered by the questions in “You May Ask Yourself…”.

Click to enlarge.

Click to enlarge.

The marketing-related policies—questions 1 through 4—will dictate the manner in which the tactical sales budget will vary according to fluctuations in the exchange rate. The production policy considerations—questions 5 through 7—indicate that the budget must be able to handle severe production changes. As a reaction to tariffs and other trade war dysfunctions, companies are reallocating and adjusting their production resources and supply chains. As the markets respond and costs climb, multinationals redirect their efforts toward cost containment and reduction to maintain an acceptable level of profitability. The management policies resulting from these shifts will become part of the strategic planning effort while being incorporated into the budgetary planning and control process.

Flexible budgeting will assist in implementing and controlling marketing and production changes. The final two strategies (as described in questions 7 and 8) attempt to assist multinationals in matching cash outflows (production and financing costs) with cash inflows (revenue and capital proceeds) in the same currency to minimize the cash flows between countries and, ultimately, reduce economic exposure. Once established, these policies will be part of the budgeting process and will be used to evaluate the actual performance of foreign operations that are subject to exchange rate fluctuations.

THE IMPACT OF INTEREST RATES

Interest rates affect multinational corporations through the Fisher Effect, the International Fisher Effect, and interest rate parity relationships. As history has demonstrated time and again, organizations that ignore interest rates, or assume they will remain stable, are playing with fire.

Fisher Effect. The Fisher Effect maintains that the nominal interest rate is a function of the real interest rate and the inflation rate. Furthermore, it contends that real returns are balanced between countries through arbitrage and that the resulting inflation rate and interest differentials are approximately equal between two countries.

International Fisher Effect. Based on the Fisher Effect, the International Fisher Effect indicates that a change in the interest rate differential between any two countries will objectively help to predict future movements in the spot exchange rate. In reality, however, changes in the interest rate differential must be examined carefully to determine whether a shift in the inflation rate or real interest rates is the cause. These two underlying factors in an interest rate differential change will have opposite effects on the future movements of the spot exchange rate.

Interest rate parity. This asserts that, under normal conditions, the forward premium or discount on a currency is approximately equal to the interest rate differential between the two countries. A complete understanding of the past, present, and future real interest rates and inflation rates will help multinationals forecast future changes in nominal interest rates and subsequent changes in the spot and forward exchange rates. Such changes would impact budgets that include the flow of goods and capital across international borders.

In the short term, accurate interest rate forecasting can help determine potential changes in forward exchange rates. In more efficient markets, such as those within the eurozone, forward exchange rates are based on both current and future expectations of the interest rate differential. Therefore, forward rates—instead of the spot exchange rate—will play an important role in sales and purchasing budgets because of their use in determining prices for international transactions. When engaging in such transactions, each entity will determine an acceptable price based on the forward exchange rate that coincides with the payment date. Accurate short-term interest rate forecasts will permit the sales manager to determine the appropriate price or converted amount for the transaction, depending on the budget currency.

Keep in mind, forward exchange rate predictions are only as good as the underlying nominal interest rate forecasts that are used to predict them. Inflation rate changes, real interest rate alterations, and changes in people’s expectations can have varying effects on the nominal interest rate differential between countries. This makes interest rate forecasting very difficult.

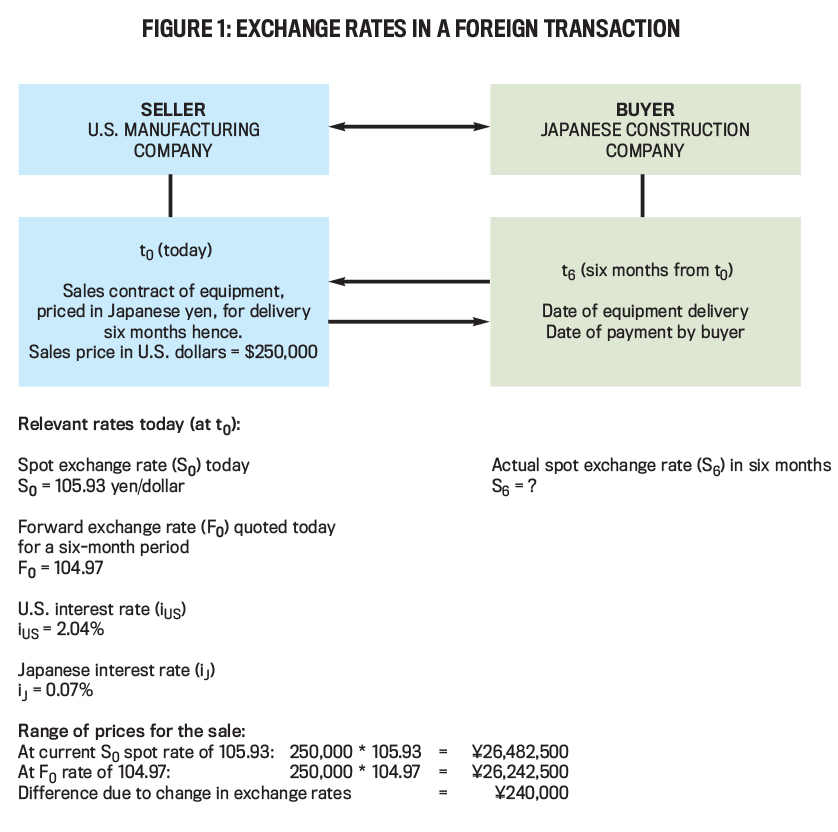

Figure 1 shows an example of a U.S. manufacturer selling to a Japanese construction company. As it illustrates, the minimum contract price that the U.S. manufacturer should accept is ¥26,242,500, using the forward exchange rate of ¥104.97 that coincides with the payment date. Based on the spot and forward exchange rates for the yen, however, the market expectations for six months hence are for the yen to appreciate against the U.S. dollar.

Click to enlarge.

Click to enlarge.

Given this, the U.S. company would be inclined to use the more favorable current spot rate of ¥105.93 to price the $250,000 sales contract, for a total value of ¥26,482,500. Assuming that the forward rate of ¥104.97 materializes, the difference due to the change in the Japanese rate between now and six months is ¥240,000 (or $2,286), representing a foreign exchange gain from this transaction for the U.S. company. Nevertheless, regardless of the sale’s final negotiated price in yen, the U.S. company might consider it prudent to enter into a derivative contract to sell forward the yen it expects to receive from the transaction, as the actual exchange rate of the dollar into yen in six months isn’t guaranteed.

THE LONG SHADOW OF INFLATION

The inflation rate differential between countries affects multinationals through purchasing power parity and the Fisher Effect. Purchasing power parity is the expected inflation differential between countries and is inversely proportional to the spot market foreign exchange rate. Usually this theory holds in the long run because the prices of goods tend not to move as freely as exchange rates. Also, different goods are used to determine inflation in different countries. Because of its long-term nature, purchasing power parity has limited application in the budgeting process but rather has more meaning as part of an entity’s strategic plan.

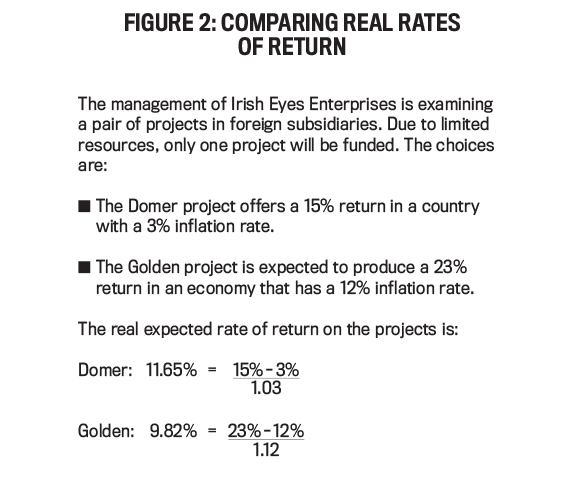

The Fisher Effect is useful when evaluating a specific important component of an organization’s strategic plan (e.g., capital budget alternatives). It permits multinationals to determine the real rate of return that a market demands given a country’s rate of inflation and the nominal rate of return required. As Figure 2 makes clear, this is especially useful when comparing investment opportunities between different countries.

Click to enlarge.

Click to enlarge.

In general, the differential in the nominal rate of return for two identical budgeting opportunities in two different countries should be approximately equal to the inflation differential between the countries. In exceptional cases, some countries (like Venezuela in recent years) experience an inflation rate that exceeds 100% over a three-year period. In this situation the “functional currency” is no longer reliable nor practical for the translation of financial statements of foreign subsidiaries. Those statements then have to be translated using the controlling company’s reporting currency. For this unique situation, it would be wise to revise the budgets of those foreign affiliates just before their implementation to accommodate inflation changes that have occurred since the budgeting process started.

Likewise, when analyzing variances, the uncontrollable effect of inflation should be recognized by applying the actual inflation rates in the flexible budgeting process beforedetermining the revenue and expense variances. Overall, management must be careful when analyzing and interpreting the effect of hyperinflation or sudden changes in foreign exchange rates; their impact may not apply equally to all revenue and expense categories, such as those that are tied to long-term contracts.

Multinationals generally do a good job of tracking foreseeable trends in inflation in foreign countries and, as a result, devise strategic policies to avoid or prevent any related losses. For example, in the middle of 2019, a U.S.-based company with a subsidiary in Argentina could accelerate remittances of quarterly sales from the Argentine operation as a strategy to preserve the U.S. dollar value of the cash flow. At that time, there was an apparent crisis of confidence in the economy caused by the uncertainty of upcoming national elections. Those conditions generated a great deal of pressure on the value of the Argentine peso relative to the U.S. dollar, as the peso slid from a value of $0.0230 on July 29, 2019, to $0.0170 on August 15, 2019—a 26% drop in a matter of a few weeks.

WHAT CAN BE LEARNED?

Any business large or small—whether acting as a buyer, supplier, distributor, producer, or provider of services—is prone to be impacted by international factors that are out of its complete control. The need to measure and manage the impact of variables such as foreign currency rates, interest rates, and inflation is crucial for companies engaged in foreign operations (either directly or through their foreign affiliates) because those variables, singly or jointly, can affect the business’s target profits and cash flows. The tasks of incorporating the impact of those key factors or variables must start with management accountants and their respective teams as they prepare annual budgets and strategic business plans.

It’s also evident that foreign currency exchange rates, interest rates, and inflation inherently carry an element of uncertainty and volatility, which represents risks that financial professionals must manage in order to better forecast, monitor, and control the performance of their organization’s international business operations.

Granted, there still might be unusual, unexpected events or circumstances that require further adjustments or revisions to the budget once the estimated effects of these variables are incorporated into the annual profit plan. Nevertheless, having a well-prepared budget constitutes a solid base to map, guide, and control the actual operations of the business as it makes its way through these ever-changing and often turbulent times.

November 2020