This article is based on research funded by a grant from the IMA® Research Foundation.

Academic research has shown that individual audit partners can have a more significant impact on the client’s financial reporting quality than the audit firm (see, for instance, Daniel Aobdia, Chan-Jane Lin, and Reining Petacchi, “Capital market consequences of audit partner quality,” The Accounting Review, November 2015). Therefore, leaders must be prepared to evaluate partner characteristics to determine the fit for the company. With a grant from the IMA® (Institute of Management Accountants) Research Foundation, we surveyed more than 100 accounting managers and executives to shed light on those audit partner traits that management most values.

FINDING THE RIGHT FIT

Depending on the organization, management may have a formal or informal role in selecting an auditor. Either way, management’s unique perspectives and insights are essential to the audit partner selection process. This includes management’s expertise and intimate knowledge of the company’s financial goals and operations (including its risks and strategies). In addition, management should expect to have interactions with the audit engagement team, especially the lead audit engagement partner. By actively participating in the auditor selection process, management can help the organization make an informed assessment of each potential audit partner’s knowledge, competence, and integrity.

The managers and executives who participated in our survey work in various industries and organizations of different sizes, and their responses cover public accounting firms of all sizes. The results reveal several important audit partner characteristics, discussed here along with excerpts that reflect why these managers and executives believe these specific audit partner characteristics are important in the auditor selection process.

KNOWLEDGE AND EXPERIENCE

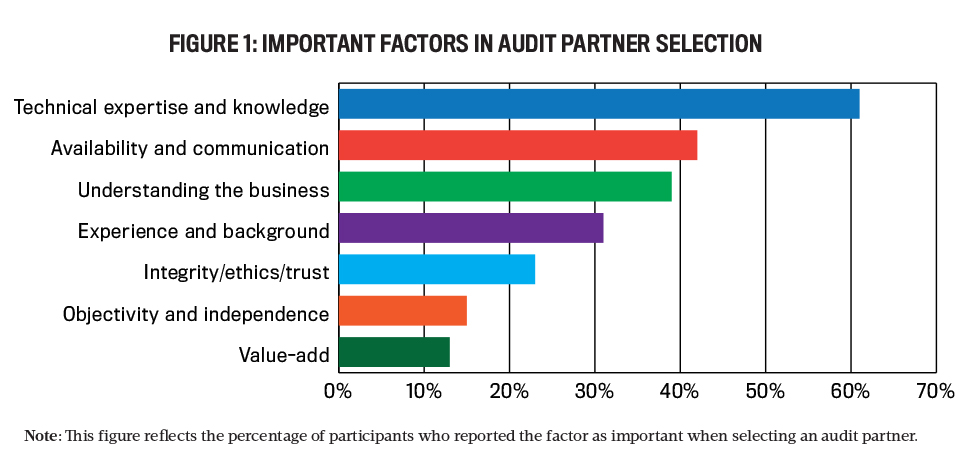

As shown in Figure 1, 61% of participants selected the audit partner’s technical expertise and knowledge as the most important audit partner characteristic. Respondents also stated that they value an understanding of the business, the industry, and current market trends as well as experience and background (the third and fourth most important factors). This understanding of the economic landscape and factors unique to that company, coupled with technical accounting expertise, can help management meet the company’s objectives.

Click to enlarge.

Importantly, this knowledge is often shaped by the partner’s background and experiences (e.g., serving certain clients). Therefore, an assessment of the audit partner’s knowledge can help align the fit between the partner’s abilities and management’s needs and preferences. The following quotations from participant responses illustrate what managers look for when evaluating various aspects of an audit partner’s knowledge and experience:

Technical expertise and knowledge

“For us, technical experience and industry experience in a global environment [are] a necessity to ensure proper tax guidance and communication and relevant explanation of any new U.S. GAAP [Generally Accepted Accounting Principles] and IFRS [International Financial Reporting Standards] developments.”—a CFO

“I look for technical expertise as well as coordination with tax and compliance members of the firm. I tend to lean toward an audit partner who specializes in specific fields (i.e., software as a service). I look for these qualities because I want someone to bring forward areas of risk that I may not see myself.”—a controller

“Technical experience to match or exceed my own.”—a director of accounting

“Technical expertise is critical because it can help make us better.”—a retired CEO

Understanding the business and industry

“I look for a partner that understands the industry that I’m in. I don’t want to have to teach my partner about the general industry, and I prefer someone that understands the nuances of our business needs.”—a CFO

“Industry knowledge. I work in a specialized, heavily controlled industry with specialized controls and accounting. Knowledge of these from an operations standpoint is crucial in audits to identify risks.”—a vice president of finance

“I look for an audit partner who understands the industry my company is in. It is good if he/she has a number of clients in the industry. I also look for an audit partner who has good technical expertise. It is important that the partner is not spread too thin with too many clients. His or her communications ability is important too.”—a managing director

Experience and background

“Years of experience, years with firm, experience with similar organization.”—a controller

“Experience and knowledge that I do not have. I try to surround myself with people who are smarter than I am.”—a CFO

“Nobody knows everything, but if you are working with someone with significant experience you will most likely be exposed to something new.”—a controller

AVAILABILITY AND INTERPERSONAL SKILLS

Many participants stated that strong technical expertise is a necessity for an audit partner but not sufficient on its own to win them over. They also recognized the importance of the accessibility of the partner and the partner’s interpersonal skills. Forty-two percent of participants mentioned partners’ communication (such as being a clear and timely communicator) and availability as important to their auditor choice.

Almost half of our participants indicated they’re looking for a partner with whom they can form a good working relationship, including a partner who is reliable and works well with management. The following quotations illustrate managers’ desire for a partner who is easily accessible, has a manageable workload, and possesses the necessary interpersonal skills:

Availability and workload

“We look to be sure we are able to communicate and get information as needed. If we are unable to reach an audit partner when needed, why have one?”—a director of finance

“Workload...how much time can the audit partner allocate to our engagement.”—a controller

“Response time and effectiveness. Waiting on responses from audit partners can bring things unnecessarily to a halt. Combining that with an effective audit are the main things I look for.”—an accounting manager

Interpersonal skills and personal fit

“Someone who is technically competent but can communicate clearly. I always look for someone who is eager to work with us and not against us.”—a CFO

“If there is a communication barrier, you have thrown an unnecessary obstacle in the path to getting your audit completed timely.”—a controller

“Someone who I can like as a person, not just their technical expertise. I don’t want to work with someone who is arrogant.”—a controller

INTEGRITY AND INDEPENDENCE

Further, 23% of participants discussed the integrity of the partner, and 15% mentioned independence and objectivity when selecting an audit partner. These considerations are enlightening, given that the U.S. Securities & Exchange Commission (SEC) is loosening auditor independence standards. The following comments illustrate that technical competence and expertise are necessary, but managers are also looking for a partner with strong integrity and objectivity:

Integrity and ethics

“Expertise, history, and ethics: I need to trust them above all to provide honest expertise in areas that I lack, and not be on the questionable side of ethics.”—a controller

“The relationship needs to be honest and have the highest integrity.”—a CFO

“Professional, trustworthy, and outstanding communication skills: I am looking for someone I can have a respectful conversation with should difficult topics arise.”—a vice president

Objectivity and independence

“They need to be objective and add value. Understanding how effective we are as management is important.”—an associate vice president of finance—controller

“Independent (neither advocate nor adversary) but at the same time easy to work with.”—a comptroller

PARTNERS WHO ADD VALUE

Lastly, 13% of participants indicated that they look for an audit partner who will add value to the organization while still maintaining independence. Specifically, managers want to leverage the audit partner’s expertise and experience to help improve the organization (e.g., identify weaknesses and opportunities for improvements) and share best practices. The following quotations illustrate these perspectives:

“I would want the audit partner to be independent and push our organization to do better each year. I would want them to provide best practices with a matrix of cost-benefit for improvements. Also, to call out deficiencies and provide options for solutions to correct...again providing the cost-benefit for each option.”—a COO

“Diligence…ability to find undiscovered SWOT [strengths, weaknesses, opportunities, and threats] items.”—a business manager

“Looking for a partner to be a value-add to our organization.”—a vice president

PUBLIC VS. PRIVATE COMPANIES

Depending on your company type (e.g., public vs. private or not-for-profit), certain partner characteristics may be a better fit for your company’s needs. The survey responses reveal that managers of private companies value audit partners’ communication skills and their understanding of the business to a greater extent and value objectivity to a lesser extent, than managers of public companies. This latter result is consistent with the stringent Public Company Accounting Oversight Board (PCAOB) and SEC independence rules with which public companies and their auditors must comply.

Because they’re faced with fewer regulatory restrictions, managers at private companies likely place more importance on the additional value-add that audit partners can provide, including providing permitted advisory services related to the risks and opportunities of the company. While managers of public companies also desire a partner who can add value, there’s likely more concern about a potential independence impairment. Nevertheless, auditors could provide value to public companies through internal control reviews and recommendations and the identification of fraud risks. Overall, managers value an audit partner who is accessible and can serve as a trusted business advisor within the applicable independence rule framework.

MORE VS. LESS EXPERIENCED MANAGERS

Because audit partners can be business advisors, you might also seek to identify partners that complement your specific responsibilities and expertise. On one hand, the survey finds that more experienced managers (such as those in C-suite and vice president, director, or partner positions) list more factors as important to their audit partner selection decision than managers with less experience (such as accounting managers and controllers). Specifically, more experienced managers list ethics, understanding the business, and communication as important characteristics for an audit partner more frequently than less experienced managers. On the other hand, although technical expertise was an important factor mentioned by most participants, we find that less experienced managers list technical expertise and knowledge more frequently than more experienced managers.

The difference in the audit partner characteristics considered most important to different experience levels illustrates the importance of considering the needs of various stakeholders and that a “one-size-fits-all” mentality may be detrimental if used in the audit partner selection process. Accounting managers and controllers are directly involved in the audit process (e.g., in answering audit inquiries and providing audit evidence). As such, it’s important that the parties responsible for making the audit partner selection decision (e.g., audit committee, board of directors, C-suite) consider the unique audit partner characteristics desired by management.

The Role of Social Relationships

We also asked survey participants how a social relationship with the audit partner would affect their assessment of the partner, and the trade-offs between the relationship and potential independence impairments on their assessment. More than half of our participants said they would be more likely to recommend an audit partner with whom they have a personal relationship. The following quotations illustrate participant considerations regarding personal and professional relationships with the audit partner, both before and after the selection process. In general, participants perceive that having a social relationship with the audit partner improves their working relationship through greater trust.

“A personal knowledge may assist in judging the character and expertise of the audit partner.”—a financial planning and analysis manager “Personally knowing the partner provides knowledge of character traits that may not otherwise be easy to detect.” —a vice president of finance “Personal relationship creates open, honest dialogue to achieve correct and fair results.”—a controller “I would have to look objectively at the relationship to ensure it didn’t skew my judgment. Assuming it was a surface-level social tie, I would look for strong moral standards in their personal life and note the ability to work/interact with others (the employees they will engage during the course of the audit). These aren’t critical factors but could be helpful with a personal knowledge of the individual.”—a CFO

“They still need to have the résumé and technical experience. If so, there should be a greater degree of trust based on the personal relationship.”—a retired CEO

OBTAINING INFORMATION ABOUT A PARTNER

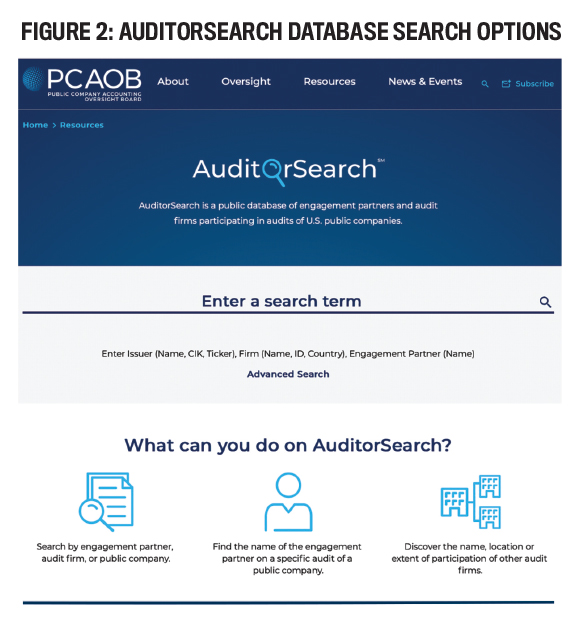

In 2017, the PCAOB began requiring audit firms to disclose the identities of the lead engagement partners of all issuer, issuer employee benefit plan, and investment company (i.e., mutual funds and broker dealer) audits in Form AP, Auditor Reporting of Certain Audit Participants. Form AP information can be accessed on the PCAOB website under the AuditorSearch, which is a public database of engagement partners and audit firms participating in audits of U.S. public companies.

As shown in Figure 2, you can enter an audit partner’s name, an issuer, a company, or an audit firm into AuditorSearch to find all of the filings related to that person or entity, or easily download an Excel file of the entire database. The database is updated daily, so information is timely. Consequently, information on the experience of all audit partners participating in public company audits can now be gleaned by reviewing the current and former partners’ audit engagements from this publicly available data.

Using information gathered from the Form AP database on the AuditorSearch website, you can learn about the audit partner’s recent experience, effectiveness, collaboration with other cultures, and workload. Specifically, Form AP provides information about audit partners’ public client experiences since fiscal year 2016, which can help you assess partner characteristics, such as industry knowledge/ experience and experience on global clients, based on the types of clients served.

By knowing who the lead engagement partner was for a given issuer, investment company, or issuer employee benefit plan audit, management can also review the related audit opinion to potentially assess the partner’s independence/objectivity and audit effectiveness (e.g., based on internal control weaknesses identified and reported in the audit opinion and/or restatements of previously audited financial statements). Form AP also includes information about other auditing firms that participated in the audit, which oftentimes are from other geographical jurisdictions.

This could provide information regarding the partner’s collaboration with other firms and their experience with other countries and cultures. It may also reveal some insights about partner workload and availability based on the number of public clients a partner serves in a year. But Form AP can only provide partial insight about partner availability and the extent of their workload because private companies aren’t required to report this information.

Using the download of the entire AuditorSearch database, you can also easily filter the downloaded Excel data set to proactively identify specific partners you’d like to interview or potentially hire (as opposed to waiting for the audit firm to present potential partner candidates). For example, you could filter the spreadsheet on a specific city and company names to identify partners in your area who have experience with similar companies.

You can also filter the data set for specific accounting firms of interest. Based on the identified partners in this targeted search, you could then use other publicly available data (e.g., from LinkedIn) to gather more information about the selected partners (e.g., outside board experience and previous work experience) that may be important to your search.

SUGGESTED INTERVIEW QUESTIONS

An important part of assessing fit is interacting with the audit partner. Depending on the characteristics that are most important to you and your company, we provide suggested interview topics and questions that you could use to obtain information about the partners’ accounting knowledge, communication skills, industry knowledge, availability, integrity, and other aspects of their experience and background. The following is a list of potential questions organized by the key partner characteristics identified in Figure 1:

- Accounting technical expertise and knowledge

- Does the audit partner currently serve, or did the partner previously serve, on any technical accounting or auditing standard committees or advisory committees, particularly in a leadership role?

- Has the audit partner participated in any thought leadership publications provided by the audit firm?

- What is the partner’s relationship with the firm’s national office and specialists, such as tax specialists, valuation specialists, and consultants (e.g., does the partner engage with them often)?

- Does the audit partner currently serve, or did the partner previously serve, on any technical committees as an engagement quality/concurrent reviewer or in other technical leadership roles in their audit firm?

- Workload and availability

- How many public, private, not-for-profit, and government audit engagements does the partner oversee annually (and their size), and what are those companies’ year-ends?

- Does the audit partner currently serve in any leadership or volunteer roles that may be time-consuming?

- Business and industry knowledge

- What are some examples of ways the partner has added value to other clients?

- Is the audit partner active in or have they written articles for any business and industry trade groups?

- Has the audit partner led any continuing professional education sessions or presented on any technical accounting, auditing, business, or industry topics relevant to your organization?

- In what geographic markets has the partner worked? What is the typical size of the organizations the partner serves?

- Integrity

- What does the audit partner’s background check indicate? Does anything in the audit partner’s record indicate a high tolerance for risk?

- Objectivity and independence

- Have any audit quality issues, including any inspection findings or peer review deficiencies or restatements, ever been identified in the partner’s audits?

- How does the partner communicate audit, business, or fraud risks and issues to management?

Along with asking partners these questions, you can use your personal and professional networks to seek out information about potential audit partners. You can ask about the audit partner’s reputation in the business community and look for indicators of how active audit partners are in their communities (e.g., serving on boards).

Management plays an important role in the auditor selection process. Individual audit partner characteristics have recently garnered increased attention from audit firms, regulators, and stakeholders. The survey results suggest managers value audit partners who not only possess necessary technical knowledge and expertise but also desirable traits such as communication skills, integrity, and the ability to add value to the company.

While technical expertise is important, other characteristics also warrant consideration to determine the right partner “fit” for your company. You can use publicly available information as well as our suggested interview questions to select an audit partner that will satisfy the company’s specific needs. It’s essential to identify an audit partner who not only promotes confidence in the financial statements, but who also can serve as a trusted (and objective) business advisor.

AUDIT TIPS AND TRAPS: MANAGEMENT’S CHECKLIST

After selecting an audit partner and beginning the relationship, be proactive in briefing your staff and establishing rules for productive interactions.

- Cooperatively support the auditor in their work.

- Avoid common misperceptions about auditors or the audit.

- Avoid seeing the audit as a threat or necessary evil.

- Realize that the auditor is neither a friend nor a foe of the company.

- Help the auditor maintain professional skepticism. Beware of the cult of personality or an attitude that the company or CEO is too important or too big to fail.

- Ensure clear communication between the auditors and executives.

- Establish procedures and protocols for mandated auditor change or rotation and to build a trusted working relationship with a new auditing firm.

- Keep in mind that the audit’s purpose is to enable the auditor’s key roles. It isn’t a punishment or adversarial exercise. That will help expedite the audit and establish a trustful relationship with the auditor.

- Provide quick responses to auditor requests. Avoid long delays in delivering requested materials and documents. That can make the naturally suspicious auditor even more suspicious.

- Provide clear and concise answers to the auditor’s inquiries.

- Be open about any contentious accounting issues where the company chose between a number of alternatives. Bring any unusual or questionable accounting treatment to the auditor’s attention in the early stages of an audit. Then you can discuss the issues and resolve them.

- Don’t feel threatened in dealing with the auditor, and demonstrate that financial officers were also very thorough in determining what accounting treatments to use.

- Remember that the auditor has a job to do, just like the company’s financial staff.

Source: George E. Nogler, “Working with Auditors: Tips and Traps,” Strategic Finance, July 2015.

November 2021