This article is part of the “Creating Greater Long-Term Sustainable Value” series launched by the October 2018 Strategic Finance article (see Mark L. Frigo, with Dominic Barton, “Creating Greater Long-Term Sustainable Value”).

CFOs are responsible for decisions about allocating resources to business units, which is where long-term value creation gets the thumbs-up or thumbs-down. During the last several years, the Center for Strategy, Execution and Valuation in the Kellstadt Graduate School of Business at DePaul University has experimented with the applications of strategic life-cycle analysis, which integrates the life-cycle framework with the Return Driven Strategy framework to analyze the long-term value-creating performance of companies.

In his latest book, Value Creation Principles: The Pragmatic Theory of the Firm Begins with Purpose and Ends with Sustainable Capitalism (Wiley, June 2020), Bartley Madden presents the competitive life-cycle framework to help CFOs, executive teams, and boards make better investment decisions using an underlying logic for management’s priorities, which are driven by the company’s or business unit’s life-cycle position.

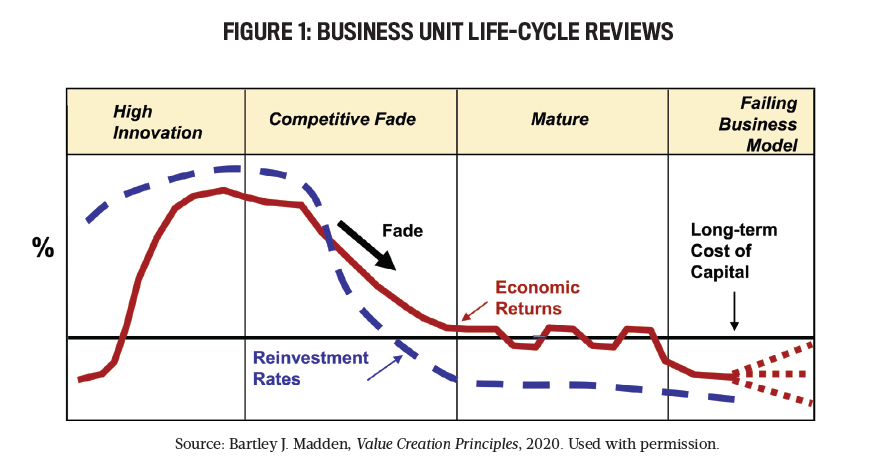

Frigo: You’ve described investment strategies that CFOs and management teams can use in each of the four phases (high innovation, competitive fade, mature, and failing business models) of the competitive life-cycle framework (see Figure 1). How would you describe those strategies?

Madden: Life-cycle track records show a time series of economic returns (returns on invested capital) and reinvestment rates plus a benchmark long-term cost of capital. Over the long term, economic returns “fade” toward the cost of capital. The fade rate is a quantitative reflection of a company’s relative competitive advantage. The key strategic issues vary depending upon a company’s or business unit’s current position in its life cycle.

In the high-innovation stage, a start-up ideally transitions to earning high economic returns coupled to high reinvestment rates. Along the way, management faces multiple critical issues. Early on, the focus should be to quickly confirm or disconfirm the core assumptions underlying the business model. With continued success, the focus shifts to ways that the business can scale, possibly by either disrupting an existing industry or creating a new market that provides genuine value to customers.

The competitive fade stage reflects the fact that high economic returns, especially if accompanied by high reinvestment rates, are a magnet for competitors. Competitors try to duplicate or improve upon the original innovating company’s business model. Over the long term, the company’s economic returns can fade toward the cost of capital and its reinvestment rates can regress (fade) toward an average economy-type growth rate. Management’s critical task in this phase is to build or acquire capabilities to expand in order to stay a step ahead of competitors (“favorable fade”).

At the mature stage, with the organization earning cost-of-capital returns, the challenge facing management is how best to improve the efficiency of existing assets and sustain its core competencies while also investing in new opportunities, some of which may have the potential to make obsolete or displace the company’s existing products or services.

The hallmark of the failing business model stage is “business-as-usual complacency.” The primary task is to restructure early and purge an excessively bureaucratic culture, thereby avoiding bankruptcy. A smaller, more focused company attuned to value creation, and especially eliminating nonvalue-adding activities, has a decidedly better chance to at least earn cost-of-capital returns.

Frigo: What advice would you give to CFOs on how to use the life-cycle framework to guide capital investment decisions?

Madden: The New Economy (discussed further below) is defined by fast-paced change driven by intangible assets that are typically treated as SG&A or R&D expenses under U.S. Generally Accepted Accounting Principles (GAAP), which creates significant barriers in analyzing how investment decisions can create future value (see “Regaining Relevance in Financial Reporting,” Strategic Finance, January 2019). For example, management committed to Lean manufacturing and service businesses will view the organization in terms of horizontal value streams that cut across accounting silos, which are normally controlled by conventional accounting-based efficiency measures and are ill-suited to Lean’s focus on overall system efficiency.

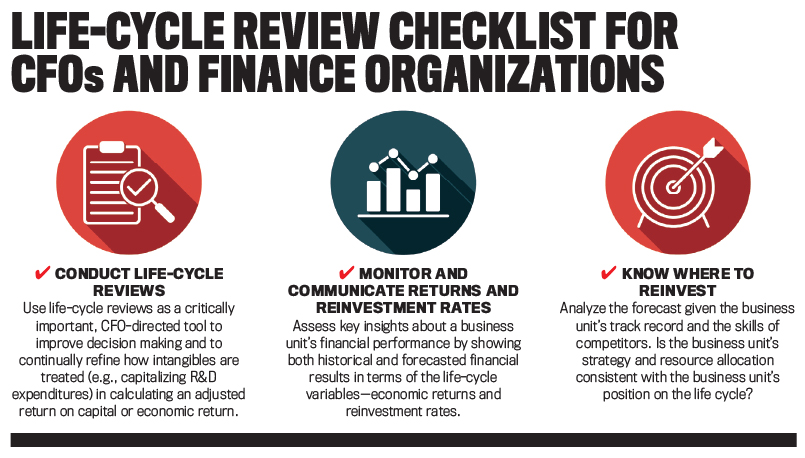

Any accounting-based control system, however useful at higher levels in the organization for ROI measurement, confronts a “crossover” problem at lower levels in the organization where process (not accounting) variables are the logical measurement tools to facilitate productivity gains. So, there is a need to have an in-house learning culture for the finance organization in order to make steady progress in dealing with company-specific performance measurement issues related to intangible assets. To meet that need, CFOs can conduct business unit life-cycle reviews that represent a useful learning tool as part of the finance organization’s executive education strategy. This can immediately improve decision making. (See “Life-Cycle Review Checklist for CFOs and Finance Organizations.”)

Frigo: If a company has implemented an economic value-added (EVA) financial system, does that circumvent or reduce the need for life-cycle reviews?

Madden: Life-cycle reviews are complementary with EVA by providing a means to experiment with the treatment of intangibles and to pinpoint critical financial performance measurement issues. For example, consider the frequent use of some version of a capital asset pricing model (CAPM)/beta equity cost of capital with EVA, which entails an estimate of beta and an estimate of the equity risk premium. Due to the inherent wide variation in these estimates, this can result in cost-of-capital swings that change EVA from positive to negative, or vice versa, due to using different but still plausible estimates.

If only a single EVA number is the focus, users can be unaware of the cost-of-capital impact on EVA. This situation can be avoided with life-cycle track records that display the component parts to value creation—economic returns, reinvestment rates, and a benchmark cost of capital. Furthermore, is a year-to-year EVA increase due to investing more in above-cost-of-capital projects or investing less in below-cost-of-capital projects? The former requires significant skill and is consistent with favorable fade in the future, whereas the latter is less sustainable as to long-term value creation.

The more management teams work with life-cycle track records and investor expectations, the more apparent the increased importance of fade in the New Economy becomes. The key to exceptional gains and losses for shareholders is the fade rates for economic returns and reinvestment rates—all the more reason to have a visual readout of these variables.

Another thing to consider in strategic life-cycle analysis is that brands are important intangibles that can help companies resist the competitive fade. Brands are difficult to capitalize and amortize, but value from a brand is reflected in favorable fade of future economic returns (see Chapter 5 of Value Creation Principles as well as “The Financial Value of Brand” in the October 2019 issue of Strategic Finance).

Frigo: The life-cycle framework can be a powerful tool to assist CFOs and finance organizations help companies create greater long-term sustainable value. It provides a disciplined logic for making capital investment decisions, especially as pertaining to intangible assets in the New Economy. Continuing our discussion, you describe in your book the long-term life-cycle histories of many organizations and analyze the strategies that created significant value or, in some cases, dissipated value. Can you highlight a few examples that would resonate with CFOs?

Madden: Today, there’s a tendency to classify organizations into two broad categories: New Economy winners such as Amazon and Facebook that have exploited the use of information and networks vs. Old Economy companies that are often lagging in innovation with low-growth, large-scale manufacturing businesses or physical retail stores (Costco is an exception and has resisted the fade in economic returns by innovating its offerings and creating hard-to-duplicate value for its customers). A better approach is to employ the life-cycle review mind-set and compare management’s actual strategy and resource allocation to what should be their top priority given the company’s current life-cycle position. With this approach, all organizations are seen to have opportunities for unique value creation and delivering rewarding returns to their shareholders over the long term. Let’s look at two companies that illustrate this idea of widespread value creation opportunities.

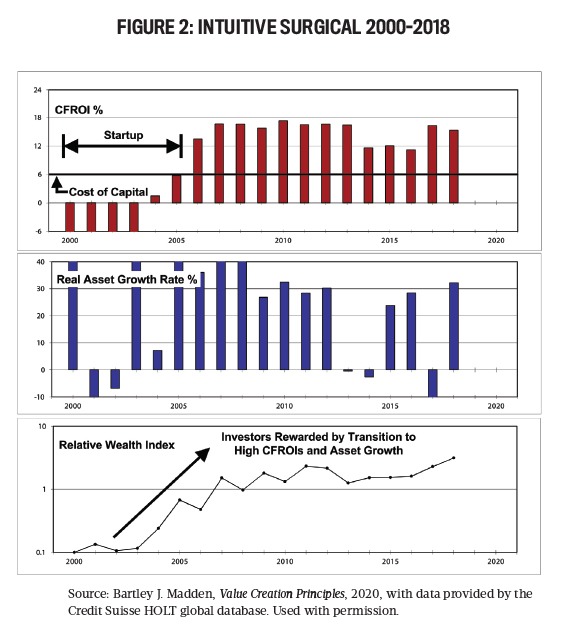

The first example is Intuitive Surgical. In 2018, one million robotic surgery operations were performed using approximately 5,000 da Vinci robotic surgical systems pioneered by Intuitive Surgical. Figure 2 displays the life-cycle track record for Intuitive Surgical.

The life-cycle chart consists of three panels. The top panel displays a company’s economic returns as CFROIs (cash-flow return on investments), which are inflation-adjusted (real) returns and which include myriad adjustments to minimize accounting distortions. A horizontal dark line is drawn at 6% as a benchmark real cost of capital. When analyzing a long-term (say 20 to 50 years) time series of CFROIs, the inflation adjustments are critically important in order to more accurately measure levels and trends. The middle panel displays annual real asset growth rates (which include capitalized R&D). The bottom panel displays a relative wealth index, which is a stock’s total shareholder return relative to the total return of the S&P 500 Index. Outperformance is seen as a rising trend; market-matching performance is recorded as a flat trend; and underperformance of the S&P 500 shows as a declining trend.

The top and middle panels of Figure 2 show that after Intuitive Surgical proved the commercial viability of its technology as a start-up, the company transitioned to earning high CFROIs and high reinvestment rates due to the patient benefits of this less-invasive surgical approach. This transition wasn’t anticipated by the very early investors, and, as the higher level of performance was delivered, the stock significantly outperformed the market (bottom panel).

Over the last decade, management executed on the primary task given its position in the competitive fade stage of the life cycle. It built or acquired capabilities in order to stay ahead of competitors and achieve a favorable fade, i.e., avoided a fast regress of CFROIs toward the cost of capital. Intuitive Surgical developed advanced expertise in systems, instruments, staples, energy, and vision that enables the organization to create the future of robotic surgery.

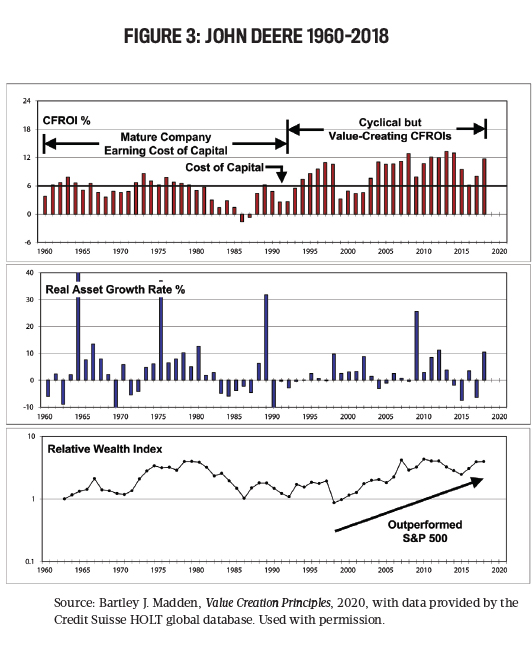

The second example, John Deere, is a stellar model of a so-called Old Economy manufacturer of farm equipment that successfully transitioned from a mature-stage company to a value creator. The top panel of Figure 3 illustrates that from 1960 to the early 1990s, Deere was in the mature life-cycle stage with CFROIs approximately equal to the long-term cost of capital. Management recognized that its top priority was to change its way of doing business and to embrace a culture focused on delivering value-creating (above-cost-of-capital) economic returns.

Management implemented a shareholder value-added (SVA) financial system to improve resource allocation decisions. Importantly, to better compete in the digital world of the New Economy, John Deere evolved from a product-centric business to incorporate a platform-centric capability. This platform exploits the Internet of Things (IoT) environment using sensors on its products and probes in the soil. AI, data sharing, and software tools enable its customers to increase yield and decrease costs in all phases of farming. Returning to the top panel of Figure 3, the last 25 years shows cyclical and mostly value-creating CFROIs in excess of the cost of capital. Shareholders were rewarded, as shown in the bottom panel.

Frigo: These two examples (and others in the book) provide a compelling case for CFOs and finance organizations to develop skills and capabilities for conducting life-cycle reviews. In doing so, they can develop a strategic value-creating finance organization for the New Economy. Besides the life-cycle framework benefits, what other key ideas could you share that would be most useful for CFOs?

Madden: The pragmatic theory of the firm is about a holistic system of connected activities all supporting the organization’s purpose. When a company’s purpose is clearly articulated, then maximizing shareholder value is best positioned as the result of a company successfully achieving its purpose. A different perspective on risk is the concept of “firm risk,” which is defined as impediments to achieving a company’s purpose. A company’s knowledge-building proficiency, relative to competitors, is the primary determinant of its long-term performance. A knowledge-building culture is not only about delivering performance. It can facilitate management conversations with investors who want a deeper understanding of what’s driving the company’s long-term financial performance. Such investors typically are highly desirable long-term owners of the company’s shares.

Frigo: While you make the case that a company’s knowledge-building proficiency is the primary determinant of its long-term performance, some might disagree and argue, for example, that unique capabilities are the most important key to long-term performance.

Madden: How was the decision made to build or acquire those unique capabilities? How does the organization continually improve those capabilities? We return full circle to nurturing and sustaining a culture of knowledge-building proficiency as the bedrock driver of long-term performance. Management of, and accounting for, knowledge-building expenditures is a significant challenge to effective handling of company-specific intangible assets in the New Economy. CFOs who successfully deal with this challenge will contribute to their organization’s competitive advantage. (See “Knowledge-Building Culture: A Key Indicator for Success or Failure” at end of article.)

Frigo: CFOs have a great opportunity to further develop strategic finance organizations using life-cycle reviews and to help their companies create long-term sustainable value by adapting life-cycle reviews as part of their finance organization mission. This is especially important in today’s turbulent New Economy, where superior and sustainable ROI is increasingly driven by intangible assets. CFOs and finance organizations can experiment with handling intangibles in ways that can easily be accommodated with life-cycle reviews. The resulting performance measurement insights can be used immediately to improve resource-allocation decisions to achieve long-term sustainable value creation. CFOs can also use strategic life-cycle analysis logic to develop the internal brand of the finance organization as a strategic and value-creating part of the company. CFOs can also use the life-cycle reviews as a way to communicate the strategy of the company to boards of directors and to investors during earnings calls and investor presentations.

Knowledge-Building Culture: A Key Indicator for Success or Failure*

Management and the board should continually invest for the future even if such investments are incompatible with, or at times even compete with, the firm’s existing assets.… [I]nnovation involves an organizational structure consistent with knowledge building and insightful feedback. This is not a new concept but merely a commonsense conclusion consistent with the long-term track records of highly successful firms.

…[O]n the road to bankruptcy, Eastman Kodak produced a significant inventory of patents emblematic of their R&D proficiency. However, alongside this technical skill for innovation, management created a bureaucratic culture that assumed business-as-usual would produce success in the future. For example, management repeatedly forecasted that its cameras and film would maintain a wide leadership over digital photography. Management with a worldview rooted in never-questioned assumptions will surely fail to get useful feedback about a changing environment and will lose the opportunity to adapt early to a new world.

*An excerpt from pp. 71-72 of Value Creation Principles.

October 2020