With the U.S. economy rebounding quicker than expected, many business leaders are now grappling with how to keep up with demand. As CFOs and their teams look for ways to deliver on present growth opportunities, a lot can be learned from the organizations that thrived through the worst.

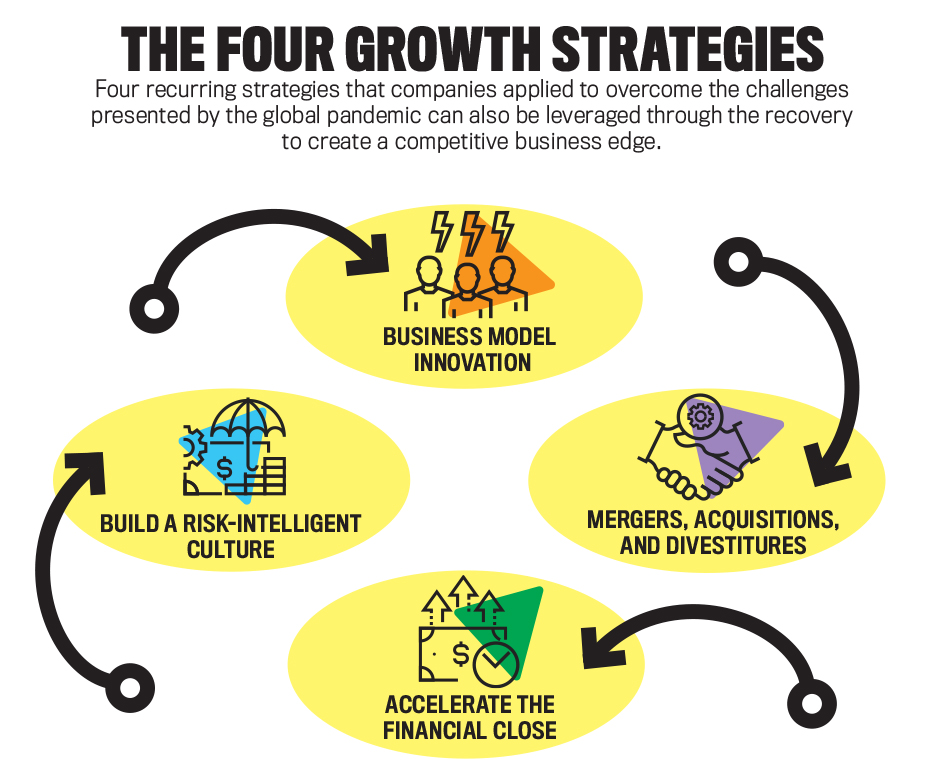

Earlier this year, Oracle pinpointed four recurring strategies that the most ambitious and innovative companies have taken advantage of over the last year to gain a competitive edge and achieve rapid growth: business model innovation; mergers, acquisitions, and divestitures; accelerating the financial close; and building a risk-intelligent culture (see “The Four Growth Strategies”).

As much of the developed world reopens, many organizations are optimistic and looking to invest for a new era of growth. These same four strategies that have proven successful over the past 16 months will continue to be the foundation for companies looking to advance in this new business environment.

BUSINESS MODEL INNOVATION

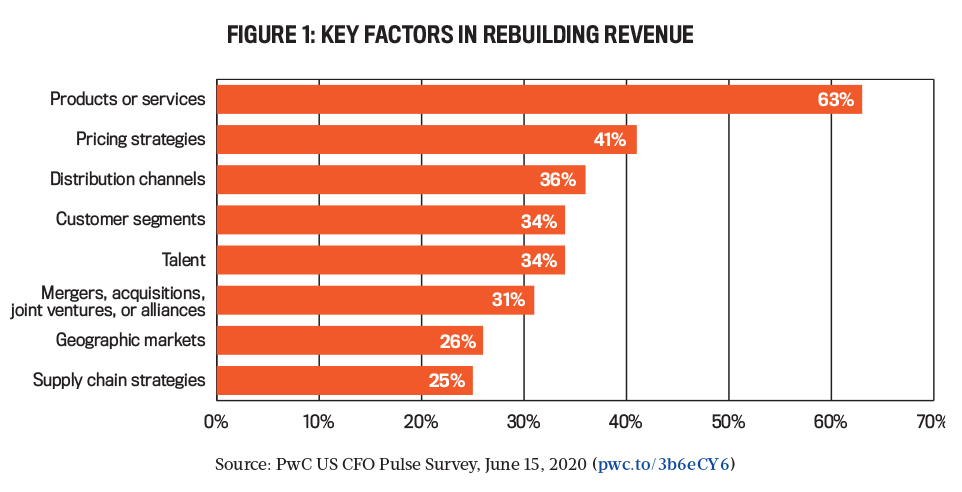

The COVID-19 pandemic changed consumer habits and expectations overnight. To meet these new and constantly evolving expectations, companies had to stay relevant by rethinking existing business models. For instance, when students were suddenly required to stay at home due to local health ordinances, universities had to shift to online learning while still giving students a valuable educational experience. These shifts are continuing to occur across every industry. In fact, a recent poll conducted by PwC found that changes to product and service offerings are considered the most critical component to rebuilding and improving an organization’s revenue streams in the current environment (see Figure 1).

The companies embracing business model innovation are redefining industries by transitioning from transactional business models to service-based business models that ensure a steady and recurring revenue stream. For example, fitness companies that once sold physical pieces of equipment now sell monthly subscriptions to online classes that users can stream on demand from the comfort of their homes.

The case is clear for why business model innovation is a must for many industries coming out of the pandemic and how it can support the shift in consumer habits. But how can your organization get started on taking advantage of this growth opportunity? Begin with these five steps:

- Assess what your customers want. What your customers wanted in early 2020 may not be the same as what they want now. Research your customer base and listen to their feedback using surveys, customer community groups, or virtual events. For instance, a retail company might learn that, while it’s planning on opening another storefront, many of its customers prefer to never shop in-store again. Armed with this information, the company can decide how to best pivot its brick-and-mortar and e-commerce strategies to meet those customer preferences.

- Analyze various business models. Many CFOs are hesitant to shift business models because of the negative impact on short-term revenue. To calm this fear, finance teams should use scenario modeling and financial planning tools to analyze the potential cost of the immediate shift vs. the revenue potential over time. By modeling different scenarios, offerings, and market conditions, company leadership can see what investments make the most financial sense and have the highest potential for continuous revenue growth.

- Collaborate across the entire organization. Even the best innovation attempts can be sabotaged by information silos. To be successful in your business model shift, it’s important that stakeholders across all departments, from HR and finance to engineering and sales, are involved in the innovation process. This collaboration encourages critical components to be debated while developing the product and/or service: What is the best way to bundle services? What should we charge? Should we staff up internally or through contractors? Clear and strong alignment across the organization on these details will ensure every offering is set up for success.

- Design for customer success. With subscription-based business models especially, customer satisfaction is a key indicator for recurring revenue. That’s why companies should create a self-service platform for customers to easily manage their subscriptions or buy a new service when it’s convenient for them. When using a simple and intuitive user interface, customers will have a positive experience with the brand and be more likely to continue renewing services, creating reliable recurring revenue for the organization.

- Measure outcomes and stay agile. Changing a business model requires a reimagination in the way key performance indicators are measured and tracked. For example, moving to a subscription-based model means you’ll be recognizing revenue and billing customers differently (e.g., monthly or quarterly vs. a onetime fee).

To ensure business leaders know what’s working and what isn’t and can quickly adjust any underperforming offerings, finance teams need to collaborate with the rest of the organization to keep them informed using real-time data set against their initial forecasted plans to adapt investments as needed.

MERGERS, ACQUISITIONS, AND DIVESTITURES

According to Reuters, the first half of 2021 alone saw a record $2.4 trillion globally in mergers and acquisitions (M&A) activity. Why? In addition to low interest rates, the most agile companies capitalized on the changes forced by the pandemic to rethink their long-term growth and performance strategies. Some companies considered M&A an opportunity to build on the company’s core business. By growing its footprint in its existing industry or spreading into adjacent markets, a company could expand its customer base and diversify products and services. Others saw the pandemic as an opportunity to drop the dead weight of underperforming assets to lower operating costs, increase profits, and improve organizational coherence.

While taking advantage of M&A and divestitures can be a hugely beneficial method to achieve organizational growth, it’s also one of the most challenging tasks of a CFO’s career. From consolidating multiple companies’ financials onto a single ledger to deciding which company’s enterprise resource planning (ERP) system to stick with (or sometimes an even tougher task—deciding to start from scratch and implement an entirely new ERP system), here are the best practices for getting started:

- Know what you’re getting into. To mitigate risk, start your M&A journey by modeling likely scenarios and then develop financial plans and cash flow analyses for each of those possibilities. But don’t stop at financial planning. Make sure to model scenarios across every department. For instance, you’ll want to evaluate your current and future workforce needs by linking financial with workforce plans to assess how M&A projects will impact corporate resources as well.

- Establish business process owners. Change management is a critical component to success when it comes to M&A and divestitures. To ensure that everyone is working toward the same goal, assign owners for each business process across IT, finance, operations, and more. Holding every team equally accountable for M&A or divestiture success will foster collaboration, alignment, and buy-in across the organization.

- Create a plan for financial reporting. For finance professionals, one of the most challenging parts of a merger or acquisition is marrying two separate companies’ financial data into one. Ask yourself: Will you move Company A onto Company B’s ERP system? If both systems are on the respective premises, which cloud-based ERP platform should you use? Should you onboard end-to-end processes all at once or gradually?

By mapping out a plan early on that’s aligned with your high-level strategic goals, the finance team will remain organized with its eye on the prize, rather than becoming overwhelmed by processes and having to make decisions under duress once it’s knee-deep in the process.

ACCELERATE THE FINANCIAL CLOSE

Now more than ever, companies and their finance teams need to move fast to identify and capitalize on areas of potential growth. But moving quicky is difficult when an organization is spending weeks reconciling accounts, closing the books, and reporting earnings to stakeholders. With some organizations spending up to a month to close their financial quarter, finance teams can potentially spend a third of their time looking back instead of looking forward.

By leveraging AI and machine learning to automate financial close processes such as account reconciliation and reporting, organizations can root out many of the manual processes that hinder a company’s ability to achieve a fast financial close. And by removing the manual effort required, finance teams can reduce human error and spend less time crunching numbers and more time doing what they’re passionate about: identifying new opportunities for revenue and growth. So, how can companies embrace automation to accelerate the financial close? There are a few critical steps for getting started:

- Think through the “extended” process. It isn’t possible to improve financial close processes without first factoring in the hundreds of steps and employees that make up the process. Be sure to think past the final step of closing the books, and instead consider the “extended” financial close, which includes account reconciliation, tax provision, subledger close, and submitting filings to regulatory bodies. By thinking about the full, extended task, CFOs will be able to develop a more strategic plan that achieves the organization’s holistic goals.

- Focus on specific areas of improvement. After the extended financial close process is documented and understood, you can then focus on pinpointing the areas that need to be improved most urgently. In identifying these areas, look for tasks that are tedious, repetitive, or prone to frequent error that could benefit from automation. For many organizations, these processes are extremely manual and reliant on spreadsheets, such as account reconciliation, currency exchange, or payables and receivables.

- Leverage intelligent process automation. Once you’ve identified the processes that could benefit from automation, begin implementing the right tools. Intelligent process automation (IPA) is the next evolution of robotic process automation (RPA), adding in AI capabilities to analyze data, identify new patterns, and make recommendations that improve efficiencies. With IPA, finance teams can automate the repetitive areas that are sucking up their team’s valuable time and instead allow them to focus on higher-level tasks that make a noticeable impact in their organization’s bottom line.

- Create a real-time view of the close. With something as important as the financial close, the status of tasks shouldn’t be left to guesswork. Being able to track and share the status of close processes with stakeholders anywhere, anytime is crucial to collaboration and success and shouldn’t be tracked through spreadsheets living on a computer desktop.

That’s why many finance teams are moving to cloud-based solutions with shared dashboards that provide a real-time view of project statuses across any geography or division. And because closing the books is a recurring activity, full visibility of what worked and what didn’t in past iterations provides an opportunity for finance teams to learn and identify opportunities for improvement.

Leveraging AI and machine learning to accelerate the financial close shouldn’t be an intimidating adjustment for finance teams. In fact, it’s an exciting opportunity for everyone involved. By passing off the most repetitive, manual accounting tasks that are prone to human error, finance professionals can instead focus on more strategic work—allowing them to elevate their career paths and have a voice in board-level strategies, rather than crunching numbers in a corner office. For business leaders, it’s critical to paint the picture of what these new, improved roles could look like to ward off any concerns around job security and gain full buy-in from your finance team early on.

BUILD A RISK-INTELLIGENT CULTURE

Unfortunately, innovative technologies and new business strategies can be risky. In fact, a 2019 SANS Institute Cloud Security Survey that examined the business security competency among hundreds of companies across the globe found that nearly one in five companies had a breach occur in 2018. This leaves CFOs with the important responsibility of defining and combatting risks associated with the big moves they’re making to get their organizations back to growth. For example, during an acquisition, the number of access points to an organization’s sensitive data are increased as the company onboards new employees and transitions information from one system to the other.

Having a well-integrated risk management strategy to monitor the compliance and security of these processes can ensure that any new opportunities for business growth don’t jeopardize the company’s reputation or bottom line. But when it comes to something as critical as risk management, it’s important to follow best practices:

- Secure a quick win. With risk management, time is of the essence, so don’t wait to kick off your journey to risk intelligence. Instead, identify the most critical areas of exposure in your enterprise and shift existing resources to those activities. By starting with a smaller, well-defined project, you’ll see quick results for a relatively low investment, which will increase confidence in the strategy, identify critical players in the decision-making process, and create a playbook for rolling out a larger risk management blueprint.

- Centralize risk management activities. When everyone in the organization has insight into risk metrics and performance, from security monitoring to compliance, it heightens risk awareness and allows for stronger risk-based decisions and oversight. To get started, it’s important to prime your organization by eliminating manual, spreadsheet-based processes in favor of the native risk automation capabilities that are embedded in business applications. And by leveraging a suite of business applications that are fully integrated on a common data model, organizations can mitigate risk by having a full view of the company’s decisions, including how one department’s actions could put another’s at risk.

- Automate critical controls across the organization. When it comes to risk management, removing as much manual error as possible can be the difference between overcoming or falling prey to nefarious actors. Assess the activities and controls within your organization’s risk strategy to determine what can benefit from the continuous monitoring of automation, and then leverage the AI capabilities within your business applications to do so. It’s important to work with stakeholders in every department to better identify and understand the risks that pose the biggest threats across the entirety of the company.

There are many ways for CFOs and their finance teams to restart their organization’s growth engine and take advantage of the rebounding economy, and this playbook will continue to evolve as our new normal is established. But no matter what strategy an organization takes, those that will be successful have one thing in common: a strong technological foundation that enables them to be flexible and pivot quickly.

Cloud-based business applications that embed the latest emerging technologies, such as AI, analytics, and blockchain, are no longer the exception—they’re the rule. Advanced technologies combined with a willingness to make big moves will determine an organization’s ability to outpace change and avoid being left behind.

October 2021